|

|

|

|

|||||

|

|

|

Credo Technology Group Holding Ltd CRDO has witnessed a sharp upward trajectory in revenues over the recent quarters, reflecting strong business momentum. Despite tariff headwinds, customer concentration risks and the broader macroeconomic uncertainty, the company reported strong year-over-year revenue growth in each of the fiscal 2025 quarters, driven by rising demand for its high-speed connectivity solutions.

While top-line growth often grabs eyeballs, Credo’s strength lies in its margin profile and operational discipline. Credo is not only driving substantial product momentum but also showcasing the profitability of its business model. In fiscal 2025, operating margin expanded 2,500 basis points, reflecting strong top-line leverage fueled by product growth. Operating expenses grew at a significantly slower pace than revenues, resulting in a substantial increase in profitability that positively impacted the bottom line.

Its revenues nearly tripled from the fiscal first to the fourth quarter, demonstrating its ability to respond to a key market shift. The company focused on innovative, reliable and energy-efficient connectivity, with strong growth in HiWire Active Electrical Cables (AECs), optical and retimer products. CRDO continues to gain traction in the optical market with a major DSP win for an 800G transceiver and has launched ultra-low-power optical DSPs using 5nm tech. It also noted a robust pipeline for PCIe Gen6 AECs and retimers, with customer wins expected to boost revenues in fiscal 2026.

Through smart innovation, strategic alignment with AI and data center trends, and disciplined financial management, the company is delivering a combination of top-line growth and operating excellence. For fiscal 2026, CRDO expects revenues to surpass $800 million, implying year-over-year growth of more than 85%. Non-GAAP operating expenses are projected to increase at less than half the rate of revenue growth compared to fiscal 2025. As a result, it anticipates its non-GAAP net margin to approach 40%, reflecting strong operating leverage and continued financial momentum.

Marvell Technology, Inc. MRVL saw a 63% increase in revenues year over year to $1.9 billion in the first quarter of the fiscal year and anticipates continued strong growth into the second quarter. This momentum is fueled by rising AI demand in the data center market, with revenues driven by the rapid expansion of custom silicon programs and solid shipments of electro-optics products.

In fiscal 2025, MRVL’s data center revenues increased 76% year over year, supported by high demand for electro-optics, custom AI chips and next-generation switches. The company expects this growth to continue into the second quarter, with mid-single-digit gains and robust year-over-year growth. For the second quarter of fiscal 2026, MRVL projects revenues of around $2 billion (+/-5%), suggesting an estimated 57% increase from the previous year.

Fueled by strong demand for its AI semiconductor solutions and VMware, Broadcom AVGO posted 20% year-over-year revenue expansion to $15 billion in the second quarter of fiscal 2025. AI revenues rose 46% year over year to more than $4.4 billion, driven by continued strength in AI networking. Adjusted EBITDA grew 35% year over year to $10 billion, highlighting the strength of its business model.

The company expects AI semiconductor revenues to grow 60% to $5.1 billion in the fiscal third quarter, marking 10 straight quarters of growth as investments from hyperscale partners in AI XPUs and connectivity solutions for AI data centers continue. For the fiscal third quarter, Broadcom expects revenues of $15.8 billion, up 21% year over year. Semiconductor revenues are anticipated to grow 25% to $9.1 billion.

Shares of CRDO gained 41.4% year to date compared with the Electronics-Semiconductors industry’s growth of 13.1%.

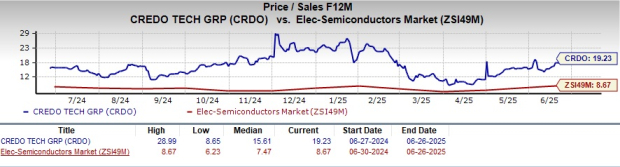

In terms of the forward 12-month price/sales ratio, CRDO is trading at 19.63, higher than the Electronic-Semiconductors sector’s multiple of 8.67.

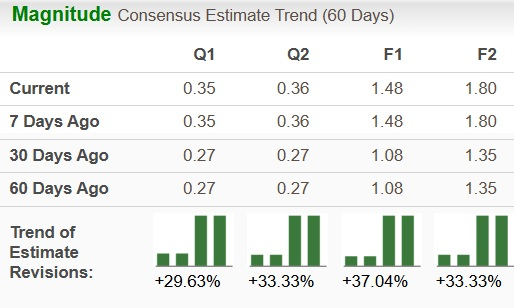

The Zacks Consensus Estimate for CRDO earnings for fiscal 2026 has seen a significant upward revision over the past 60 days.

CRDO currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite