|

|

|

|

|||||

|

|

|

Both Qifu Technology QFIN and Sezzle SEZL are eminent players within the credit tech space. QFIN, a Chinese-based fintech company, serves customers utilizing an AI-powered credit platform. Sezzle, on the other hand, is a U.S.-based buy-now-pay-later (BNPL) service provider that offers installment credit to underbanked consumers.

This comparative analysis serves well for investors who are keen on dipping their hands in the credit-tech domain and gain exposure in the fintech space at large. The end goal is to determine which stock provides a better growth opportunity.

QFIN’s core strength lies in its capital-light model, which maximizes growth while minimizing credit risk. The company utilizes the Intelligence Credit Engine (ICE) to connect borrowers with financial institution partners. This dual engine shifts credit risks to partners, thereby lowering the provisions for loan losses, thus improving margins.

The company demonstrated an impressive financial performance during the March-end quarter. Total facilitation and origination loan volume registered a 15.8% year-over-year growth. The dual engine model was responsible for 49.3% of the total originations. The top line showed 12.9% growth while operating income grew a whopping 44.8% year over year, indicating strong operational leverage.

Moving forward, we are optimistic about the company’s AI-Plus credit strategy, launched in early 2025. The main goal of this strategy is to develop an AI agent platform to enhance core credit processes. QFIN has already seen benefits from this initiative, including increased loan volumes, and its delinquency rates after 30 days of collection have remained stable at 0.6%. Additionally, funding costs have decreased 30 basis points due to improved underwriting efficiency and strong asset quality.

As a leading credit-tech platform in China, Qifu Technology benefits from the rising market opportunity. The Chinese digital lending platform market is expected to witness a CAGR of 27.3% from 2024 to 2030, and this bodes well for QFIN’s business, indicating strong demand for its services in the future.

SEZL’s market play is vested in its ability to serve the underbanked population. By carving out this niche within the U.S. fintech market, the company enjoys an immense growth opportunity. Sezzle’s presence is popular in the e-commerce space as it provides immediate financial flexibility during checkout. As a prominent player within the U.S. BNPL sector, the company is at the cusp of riding on the back of an expanding digital payment market that is expected to witness a CAGR of 11.8 % from 2023 to 2028.

The recent financial performance demonstrates the company’s ability to adapt to market forces and effectively serve the underbanked with alternative credit options. In the first quarter of 2025, SEZL’s revenues increased 123.3% compared to the same period last year. This impressive increase was driven by a rise in transaction volume, as shown by a 64.1% year-over-year increase in gross merchandise volume. Operating income surged 260.6% year over year, clearly highlighting its operational leverage and scalability.

Sezzle’s continuous innovation solidifies its position within the credit-tech domain. Initiatives, including Sezzle Balance, Money IQ, and many more, aid customers' experiences, thus paying SEZL with dividends. During the March-end quarter, the company reported an increase in the annual customer purchases frequency to 6.5 times from the year-ago quarter’s 4.5 times. It means that customers use Sezzle’s platform more often for purchases, resulting in higher transactions, which leads to higher revenues.

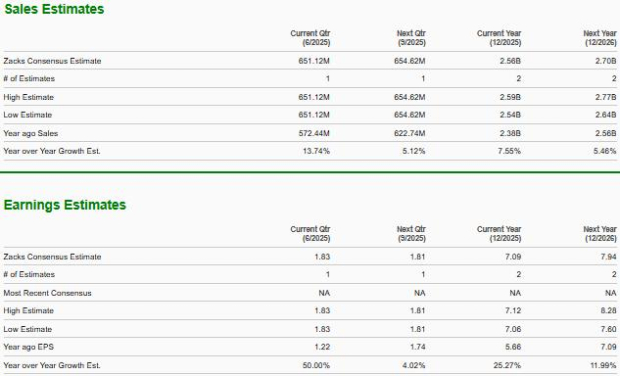

The Zacks Consensus Estimate for QFIN’s 2025 sales is pegged at $2.6 billion, suggesting 7.6% year-over-year growth. The consensus estimate for earnings is pegged at $7.09, indicating a 25.3% rise from the preceding year’s actual. Two earnings estimates for 2025 have moved north in the past 60 days, versus no southward revisions.

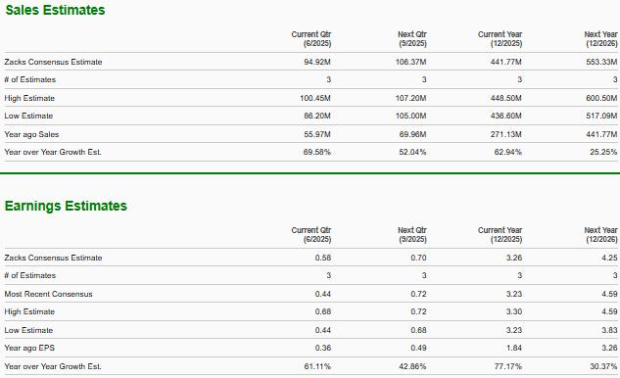

The Zacks Consensus Estimate for SEZL’s 2025 sales is pegged at $441.8 million, implying 62.9% year-over-year growth. The consensus estimate for earnings is pegged at $3.26 per share, indicating 77.2% year-over-year growth. Two earnings estimates for 2025 have moved north in the past 60 days, versus no southward revisions.

Qifu Technology is currently trading at a forward 12-month P/E ratio of 5.97X, which is slightly above the 12-month median of 5.86X. Sezzle is trading at 43.86X, significantly higher than the 12-month median of 19.51X. Although both stocks are trading at a premium compared to their historical valuations, QFIN appears much cheaper than SEZL.

Despite Sezzle’s rapid revenue growth and a top-tier Zacks Rank #1 (Strong Buy), its steep valuation at 43.86x forward earnings raises caution. In contrast, Qifu Technology offers a more balanced profile with strong operating margins, a capital-light AI-driven model, and a far more attractive valuation at just 5.97x forward earnings. While QFIN holds a slightly lower Zacks Rank #2 (Buy), its risk-reward tradeoff appears more favorable given macro uncertainties. For value-conscious investors seeking solid growth at a reasonable price, QFIN looks like the smarter buy in the current fintech landscape.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Dow Jones Futures Rise As Cloudflare Leads Big Software Winners; Jobs Report On Tap

SEZL -33.89%

Investor's Business Daily

|

| Aug-06 | |

| Jul-31 | |

| Jul-24 | |

| Jul-22 | |

| Jul-14 | |

| Jun-30 | |

| Jun-30 | |

| Jun-17 | |

| Jun-03 | |

| Jun-03 | |

| May-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite