|

|

|

|

|||||

|

|

|

Northern Trust Corporation NTRS recently passed the Federal Reserve’s 2025 stress test, retaining a 2.5% Stress Capital Buffer and confirming its solid capital position. Backed by strong organic growth, expense management initiative, and robust shareholder returns, the company remains well-positioned for long-term performance despite near-term expense pressures.

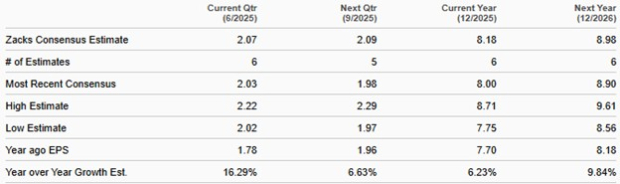

Analysts seem optimistic regarding the company’s earnings growth prospects. The Zacks Consensus Estimate for NTRS’ 2024 and 2025 earnings has been revised upward over the past seven days.

Estimates Revision Trend

Fed Stress Test Validates Capital Strength: Northern Trust passed the Federal Reserve’s 2025 stress test, which indicated that the bank could withstand a severe recession with sufficient capital to absorb hundreds of billions in losses.

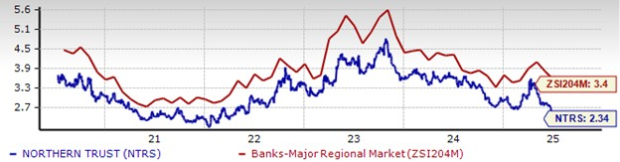

Following the stress test, Northern Trust announced its intention to increase its quarterly dividend by 7% to 80 cents per share, effective in the third quarter of 2025, subject to board approval. Currently, it has a dividend payout ratio of 38%. NTRS has a current dividend yield of 2.34% compared with the industry’s 3.4%.

Dividend Yield

Aside from the dividend, the company also maintains an active share repurchase program. In October 2021, the company approved a $25 million share repurchase program with no expiration date. The bank bought back $287 million worth of shares in the first quarter of 2025 and is targeting a similar level for the upcoming second quarter. As of March 31, 2025, 10.9 million shares remained available under the share repurchase plan.

Northern Trust’s liquidity position also supports its financial flexibility. As of March 31, 2025, its deposits with the Federal Reserve and other central banks totaled $52 billion, significantly higher than the total debt (including long-term and other borrowings) of $12 billion. Given the solid liquidity position, the company remains well-positioned to maintain consistent capital distributions and meet its debt obligations even during volatile economic conditions.

Earnings Strength: Over the past three to five years, the company's earnings per share (EPS) have witnessed an increase of 3.1%. Further, it is expected to display an upward trend in the near term, with a projected three-to-five-year EPS growth rate of 6.2%. Also, NTRS surpassed estimates in each of the trailing four quarters, with an average earnings surprise of 7.4%.

Furthermore, for 2025 and 2026, NTRS’s earnings are projected to increase year over year.

Earnings Estimates

Solid Organic Growth:Organic growth is Northern Trust’s key strength, as reflected by its revenue and loan growth story. Over the past four years (2020–2024), the company’s total revenues grew at a compound annual growth rate (CAGR) of 7.8%, supported by consistent increases in both net interest income (NII) and non-interest income. The growth momentum of revenue, NII, and non-interest income continued at a steady rate in the first quarter of 2025.

Additionally, the loan and lease balance rose at a CAGR of 6.7% during the same period. However, the trend reversed in the first quarter of 2025. Nonetheless, as the client base continues to expand, the company anticipates a rebound in loan activity, particularly as its wealth management services attract more clients.

The launch of Family Office Solutions in April 2025, targeting ultra-high-net-worth clients, provides tailored support, including investment advisory services, consolidated reporting, bill pay, and outsourced chief investment officer capabilities, which is expected to enhance this segment further. Looking ahead, the company expects further improvement in NII, backed by steady loan demand given expected Fed rate cuts by year-end. This will continue to support its top-line growth.

Cost Optimization Efforts Driving Profitability: Northern Trust has taken measures to reinstate its operating leverage over the upcoming quarters. The company focuses on disciplined headcount management, vendor consolidation, rationalization of its real estate footprint, and process automation. These efforts are expected to enhance productivity and enable the company to meet its financial objectives.

The ultimate measure of the company’s past efforts' success was its ability to consistently achieve a return on equity (ROE) between 10% and 15%. In the first quarter of 2025, the company reported its third consecutive quarter of positive operating leverage, delivering an ROE of 13%. This indicates that the company is making steady progress toward achieving sustainable profitability.

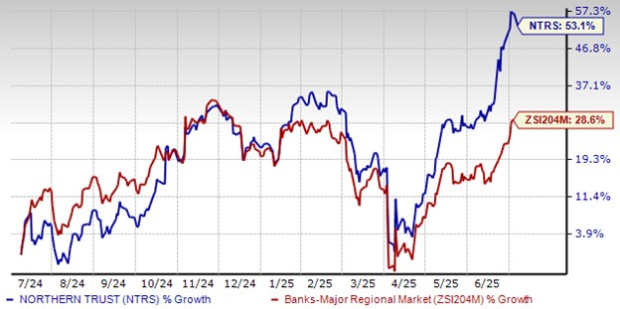

Over the past year, NTRS shares have gained 53.1% compared with the industry’s growth of 28.6%.

Price Performance

Northern Trust currently carries a Zacks Rank #2 (Buy).

Some other top-ranked stocks in the same space are BankUnited BKU and State Street Corporation STT, each carrying a Zacks Rank of 2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

BankUnited’s earnings estimates for 2025 have been unchanged at $3.20 per share over the past seven days. BKU’s share price has increased 25.8% over the past year.

STT’s earnings estimates for 2025 have been revised upward to $9.59 per share over the past seven days. Its share price has increased 47.5% during the same period.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-16 | |

| Mar-16 | |

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite