|

|

|

|

|||||

|

|

|

CyberArk CYBR reported strong subscription growth in the first quarter of fiscal 2025. Subscription annual recurring revenues (ARR) crossed $1.03 billion, up 65% from a year ago. Net new subscription ARR was $51 million compared with $39 million in the same period last year.

Recurring revenues in the first quarter reached $298.2 million, making up 94% of total revenues. Management attributes this performance to be driven by a higher proportion of self-hosted subscription deals.This transition is gradually reshaping CyberArk’s business into one driven by recurring revenues as more customers move to subscription. Moreover, subscription ARR now accounts for nearly 85% of total ARR, up from 77% a year earlier.

A key driver of this growth is CyberArk’s ability to carry out cross-selling synergies among its existing customer base. Existing customers are adopting more solutions from CyberArk’s platform, which is helping grow subscription revenues. For instance, A Fortune 100 financial services firm, which is a long-time CyberArk customer on the human identity side, expanded into certificate lifecycle management and Public Key Infrastructure (PKI) offerings with a competitive multi-six-figure Annual Contract Value (ACV) deal.

Another notable win includes PDS Health, a customer with CyberArk since 2019. The healthcare support organization expanded on the machine identity side by deploying all of Venafi’s Certificate Manager and Zero Touch PKI in a six-figure ACV deal during the first quarter.

These customer wins show how existing customers are adopting more of CyberArk’s platform offerings, boosting subscription revenues and driving larger, stickier contracts. As CyberArk continues to invest in its platform and go-to-market capabilities, the management remains confident that the adoption of multiple solutions will keep supporting its subscription momentum and drive long-term growth in the coming quarters. Our model estimate projects subscription ARR to increase 26% year over year to $1.23 billion in 2025.

Competitors like Zscaler ZS and SentinelOne S are also gaining ground through platform expansion and artificial intelligence (AI) innovation.

Zscaler ended its third quarter of fiscal 2025 with $2.9 billion in ARR, reflecting 23% year-over-year growth. The robust growth was driven by Z-Flex and rapid traction across Zscaler’s three strategic growth pillars, which include Zero Trust Everywhere, Data Security Everywhere and Agentic Operations.

Though comparatively a small competitor, SentinelOne’s ARR is also growing rapidly with reaching $948 million at the end of the first quarter of fiscal 2026. This represents year-over-year growth of 24%, fueled by the rising adoption of SentinelOne’s AI-first Singularity platform and Purple AI.

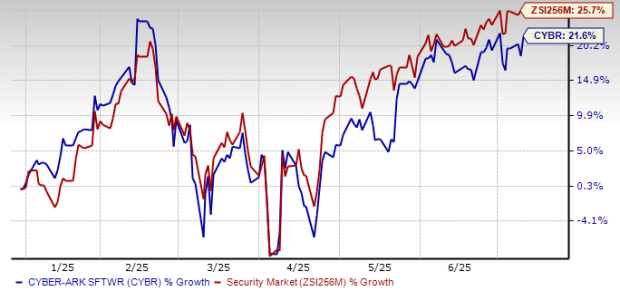

Shares of CyberArk have gained 21.6% year to date compared with the Zacks Security industry’s growth of 25.7%.

From a valuation standpoint, CYBR trades at a forward price-to-sales ratio of 13.47, below the industry’s 15.07.

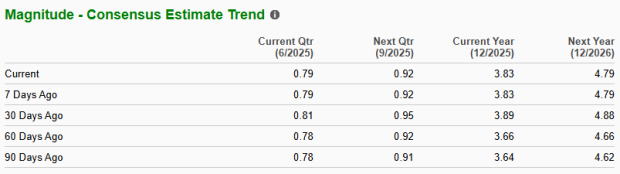

The Zacks Consensus Estimate for CYBR’s 2025 and 2026 earnings implies a year-over-year increase of 26.4% and 25.1%, respectively. The estimates for 2025 and 2026 have been revised downward over the past 30 days.

CyberArk currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Stock Market Today: Dow Slips After CPI Inflation Surprise; DraftKings Plunges On Earnings (Live Coverage)

ZS

Investor's Business Daily

|

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite