|

|

|

|

|||||

|

|

|

Altria Group, Inc. MO has demonstrated remarkable resilience in a challenging operating environment, and a major driver of this strength is its robust pricing strategy. Despite ongoing volume pressures in the cigarette category and the impact of strict regulations, the company has effectively leveraged its pricing power to support revenue and profit growth.

In the first quarter of 2025, Altria’s pricing actions played a key role in boosting revenues across both its Smokeable Products and Oral Tobacco segments. This pricing-led growth strategy continues to offset volume declines, underscoring the inelastic nature of cigarette demand. Consumers, particularly in tobacco, often remain loyal despite price hikes due to the addictive nature of the product, allowing Altria to sustain its margins.

The company’s ability to strategically raise prices without significantly losing consumers has been critical in maintaining profitability. This strength is further reflected in Altria’s 2025 earnings outlook. Management expects adjusted earnings per share (EPS) to range between $5.30 and $5.45, signaling year-over-year growth of 2% to 5% from the 2024 base of $5.19. As Altria continues to focus on premium pricing and cost discipline, it remains well-positioned to navigate industry challenges while delivering shareholder value.

Philip Morris International Inc. PM continues to demonstrate that pricing power is a central engine behind its robust profitability. In the first quarter of 2025, PM reported organic net revenue growth of 10.2% and organic operating income growth of 16%, with gross margin expansion of 340 basis points (bps) on an organic basis. Notably, pricing contributed 6 points to Philip Morris’ net revenue growth, driven by an 8% increase in combustible pricing and around 3% in smoke-free products excluding devices.

Turning Point Brands, Inc. TPB emphasizes brand strength and market positioning over aggressive pricing. Stoker’s portfolio of Turning Point Brands showed volume resilience due to consumer trade-down trends, while its modern oral business relies more on strategic brand building than aggressive pricing. Turning Point Brands continues to invest heavily in distribution and marketing, with margin performance influenced by mix shifts and input cost pressures, including tariffs.

Shares of Altria have gained 24.4% in the past year compared with the industry’s growth of 55.6%.

From a valuation standpoint, MO trades at a forward price-to-earnings ratio of 10.72X, below the industry’s average of 15.09X.

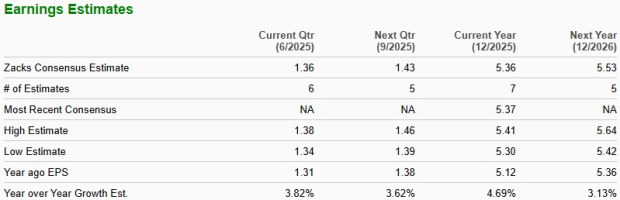

The Zacks Consensus Estimate for MO’s 2025 earnings implies year-over-year growth of 4.7%, whereas its 2026 earnings estimate suggests a year-over-year uptick of 3.1%. The estimates for 2025 and 2026 have remained unchanged in the past 30 days.

MO stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite