|

|

|

|

|||||

|

|

|

Zumiez Inc. ZUMZ delivered its fourth consecutive quarter of positive comparable sales growth, reporting a 5.5% increase in the first quarter of fiscal 2025. This performance was driven by higher dollars per transaction, supported by gains in both average unit retail and the number of units per transaction. The results highlight Zumiez’s ability to attract consumers through curated merchandise and strong pricing execution.

Category-wise, women’s products delivered the highest comparable sales increase, followed by men’s, footwear and accessories, while hard goods declined. North America remained the core growth engine, contributing significantly to the quarter’s success. Comparable sales in the region rose 7.4%, its fifth consecutive positive quarter, reinforcing Zumiez’s strong positioning in the largest market.

Total net sales for the quarter rose 3.9% year over year to $184.3 million, with North America sales increasing 4.9% to $149.7 million. Excluding foreign currency impacts, North America’s net sales were up 5.2%. These results reflect both the brand’s resilience in a volatile economic environment and the impact of product innovation, private label expansion and targeted consumer engagement strategies.

Momentum carried into May 2025, with net sales rising 0.7% year over year and comparable sales up 1.4%. North America again led performance, posting a 2.9% and 5.1% rise in net sales and comps, respectively. These figures demonstrate Zumiez’s continued ability to drive top-line growth even amid global economic headwinds.

Zumiez remains confident in its fiscal 2025 trajectory, underpinned by a combination of strong core-market performance and strategic initiatives. For the fiscal second quarter, the company expects total sales between $207 million and $214 million, indicating a potential year-over-year change between a decrease of 2% to an increase of 2%. Comparable sales are projected to range from a year-over-year decrease of 1% to an increase of 3%. Product margin is expected to improve over the prior year.

For the full fiscal year, Zumiez anticipates year-over-year sales growth and modest gains in product margin on top of the 70-basis point improvement achieved in 2024. Margin expansion is expected through operational efficiencies in areas such as occupancy, distribution and logistics.

Capital expenditures for 2025 are projected between $14 million and $16 million, aligned with 2024 levels. Nine new stores are planned for the year — six in North America, two in Europe and one in Australia — while underperforming locations will continue to be rationalized. These efforts, alongside disciplined cost management, are expected to return the company to profitability in 2025.

Zumiez’s growth strategy continues to be anchored in exclusive merchandise, private label expansion and enhanced customer experience. Combined, these initiatives position Zumiez to deliver improved operating margins and long-term shareholder value.

Zumiez is currently trading at a forward 12-month price-to-sales (P/S) multiple of 0.26X, which positions it at a discount compared with the industry’s average of 1.69X. The stock is also trading below its median P/S level of 0.37X observed over the past year. Also, Zumiez is priced lower than the sector’s average of 1.63X. It has a Value Score of B.

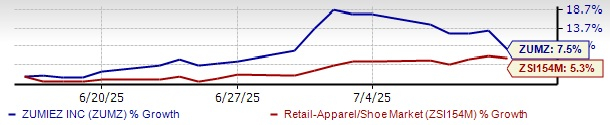

Shares of this Zacks Rank #3 (Hold) company have gained 7.5% in the past month as compared with the industry’s 5.3% growth.

Some better-ranked stocks in the retail space are Canada Goose GOOS, Stitch Fix SFIX and Allbirds Inc. BIRD.

Canada Goose is a global outerwear brand. GOOS is a designer, manufacturer, distributor and retailer of premium outerwear for men, women and children. It flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Canada Goose’s current fiscal year’s earnings and sales indicates growth of 10% and 2.9%, respectively, from the year-ago actuals. Canada Goose delivered a trailing four-quarter average earnings surprise of 57.2%.

Stitch Fix delivers customized shipments of apparel, shoes and accessories for women, men and kids. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Stitch Fix’s current fiscal year’s earnings implies growth of 71.7% from the year-ago actuals. SFIX delivered a trailing four-quarter average earnings surprise of 51.4%.

Allbirds is a lifestyle brand that uses naturally derived materials to make footwear and apparel products. It presently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for BIRD’s current financial-year earnings implies growth of 16.1% from the year-ago actual. Allbirds delivered a trailing four-quarter average earnings surprise of 21.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-20 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite