|

|

|

|

|||||

|

|

|

Comfort Systems USA, Inc. FIX reported solid first-quarter 2025 results, yet opted to keep its full-year revenue and margin guidance unchanged, thereby prompting some investors to question whether the outlook may be overly cautious. Earnings per share surged 75% year over year to $4.75, and revenues rose 19.1% to $1.83 billion, beating expectations across the board. Margins also hit historic highs, with operating income up 54% year over year.

Despite this momentum, management reaffirmed its high-single-digit same-store revenue growth forecast for 2025, citing tough year-over-year comps in the back half. However, end-market dynamics, including booming tech and industrial demand (now 62% of total volume), a rising healthcare footprint and resilient institutional business, suggest continued strength. Modular construction, a growing contributor, also underpins margin sustainability.

While tariff and cost inflation risks remain, Comfort Systems’ scale, geographic positioning and project selection discipline provide significant insulation. Executives emphasized their ability to pass through costs and secure favorable pricing, aided by long-term supplier relationships and proactive contract management.

As of March 31, 2025, the company’s backlog increased 16.5% year over year to $6.89 billion, with sequential growth of 14.9%. The increase was mainly driven by the recent acquisition of Century Contractors (closed in January 2025), alongside same-store backlog growth. Same-store year-over-year backlog growth was mainly attributable to increased project bookings in the technology sector across Texas and North Carolina operations and Texas electrical operation, in the manufacturing sector at its Kentucky electrical operation and the healthcare and technology sectors at one of its Texas operations.

Comfort Systems may be playing it safe with its 2025 view, which isn't surprising given its history of conservative guidance. While this approach might seem overly cautious, it could also reflect strong discipline during uncertain economic times. For long-term investors, the company’s large backlog, healthy finances and track record of handling challenges suggest there’s still good reason to stay confident, even if the outlook seems a little muted.

Shares of this Texas-based heating, ventilation, air conditioning and electrical contracting service provider have soared 51.4% in the past three months, outperforming the Zacks Building Products - Air Conditioner and Heating industry, the broader Construction sector and the S&P 500 Index. The detailed share price performance is shown in the chart below.

Other renowned firms that share the market space with FIX across large-scale contracting in building systems and facilities services include Quanta Services, Inc. PWR and Jacobs Solutions Inc. J. Although the market trends are favoring these companies, they are falling behind in realizing benefits from the robust fundamentals compared with Comfort Systems. In the past three months, shares of Quanta Services and Jacobs Solutions have gained 40.5% and 15%, respectively.

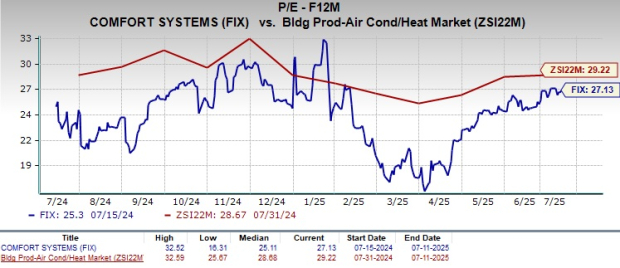

Comfort Systems' stock is currently trading at a discount compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 27.13, as evidenced by the chart below. The discounted valuation of the stock, compared with its peers, advocates for an attractive entry point for investors. That said, in the long term, the valuation could move toward a premium, given the favorable market fundamentals backing the company’s revenue visibility.

Notably, Quanta Services and Jacobs Solutions are currently trading at a forward 12-month P/E ratio of 34.66 and 20.14, respectively.

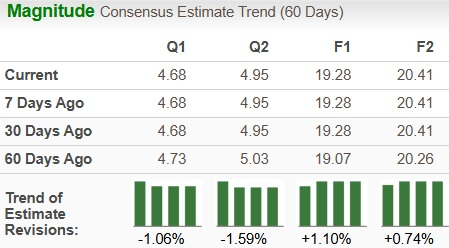

FIX’s earnings estimates for 2025 and 2026 have trended upward over the past 60 days to $19.28 and $20.41 per share, respectively. The estimated figures for 2025 and 2026 imply year-over-year growth of 32.1% and 5.8%, respectively.

The robust market fundamentals and FIX’s strategic initiatives to curb the adverse impacts of macro uncertainties are likely to have induced bullish sentiments among analysts.

FIX stock currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-18 |

Walmart To Report Results, Fresh Off New Highs, A New CEO And $1 Trillion Market Cap

PWR

Investor's Business Daily

|

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite