|

|

|

|

|||||

|

|

|

What a time it’s been for Herbalife. In the past six months alone, the company’s stock price has increased by a massive 51.5%, reaching $9.71 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Herbalife, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We’re happy investors have made money, but we don't have much confidence in Herbalife. Here are three reasons why we avoid HLF and a stock we'd rather own.

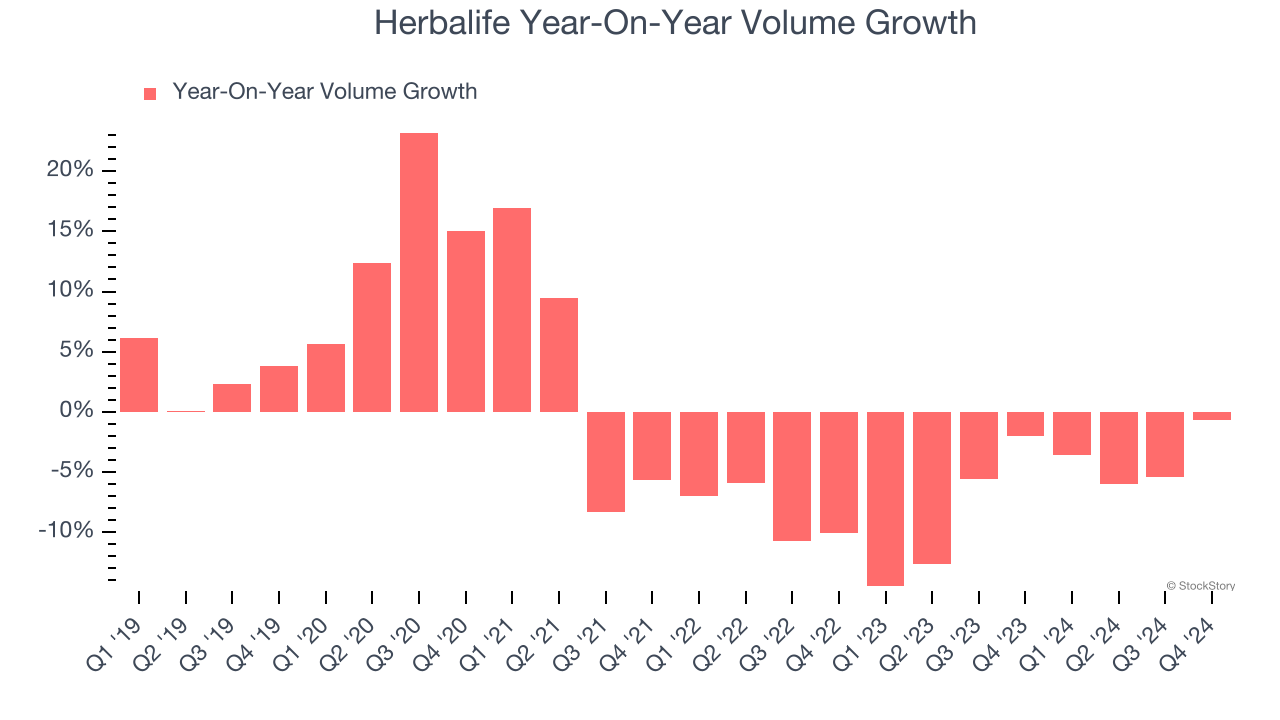

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Herbalife’s average quarterly sales volumes have shrunk by 5.1% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Herbalife’s revenue to stall. While this projection implies its newer products will catalyze better top-line performance, it is still below the sector average.

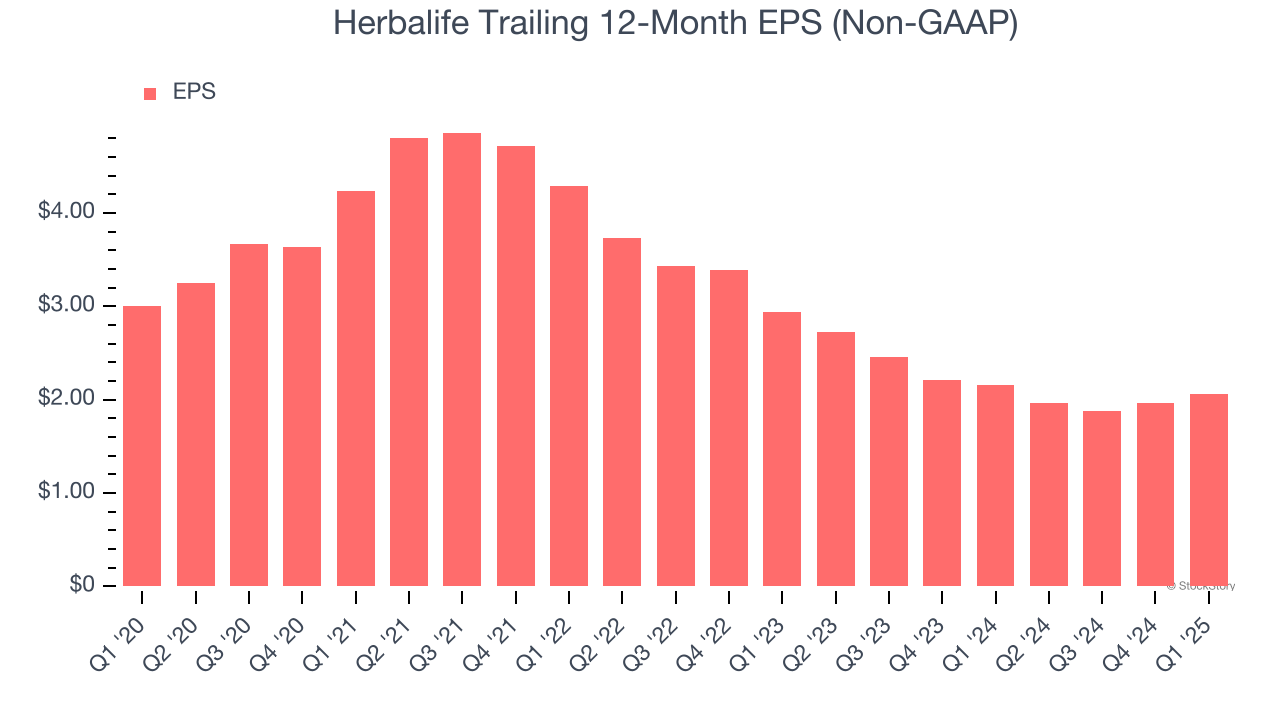

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Herbalife, its EPS declined by 21.7% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Herbalife isn’t a terrible business, but it doesn’t pass our quality test. After the recent surge, the stock trades at 4.7× forward P/E (or $9.71 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-13 | |

| Jul-01 | |

| Jun-03 | |

| Jun-02 | |

| May-15 | |

| May-08 | |

| May-07 | |

| May-06 | |

| Apr-30 | |

| Apr-29 | |

| Apr-15 | |

| Apr-14 | |

| Apr-14 | |

| Apr-10 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite