|

|

|

|

|||||

|

|

|

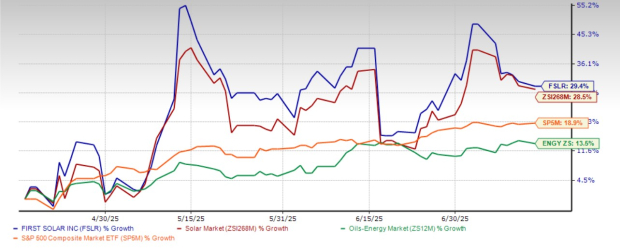

Shares of First Solar Inc. FSLR have gained 29.4% in the past three months, outperforming the Zacks solar industry's growth of 28.5%, as well as, the Zacks Oil-Energy sector’s increase of 13.5% and the S&P 500’s rise of 18.9%.

A similar stellar performance has been delivered by other solar stocks, such as Canadian Solar (CSIQ) and SolarEdge Technologies (SEDG), which have outperformed the industry in the past three months. Shares of CSIQ have gained 86.2%, while shares of SEDG have gained 113.9%.

With FSLR’s robust performance on the bourses, some investors may consider buying the stock right away. However, before taking any decision, it is important to understand the reasons behind this robust performance. Does the company have what it takes to continue this momentum, or are there risks that may affect its future growth? The idea is to help investors make a more insightful decision.

FSLR’s robust performance on the bourses seems to have been influenced by its aggressive expansion plans.

As the largest solar PV manufacturer in the Western Hemisphere, First Solar has been steadily increasing its production capacity to support future sales growth to meet the rapidly expanding global solar demand. In the second quarter of 2025, it started commercial operations at its fourth U.S. manufacturing facility.

This apart, First Solar’s ambitious plan to add around four gigawatts (GW) of new capacity, including a fifth U.S. facility, is expected to start operations in the second half of 2025 and thereby achieve an annual manufacturing capacity of more than 25 GW by the end of 2026, should bode well for its long-term performance.

Also, a recent upgrade in this stock’s target price may have added impetus to investors’ confidence and thereby bolstered FSLR’s share price. In the first week of this month, Royal Bank of Canada raised their price target for FSLR from $188.00 to $200.00, with an outperform rating on the stock currently per a report by MarketBeat).

Looking ahead, FSLR’s growth prospects are backed by its ongoing capacity expansion and strong demand outlook for solar energy, both of which are expected to drive its performance in the coming years.

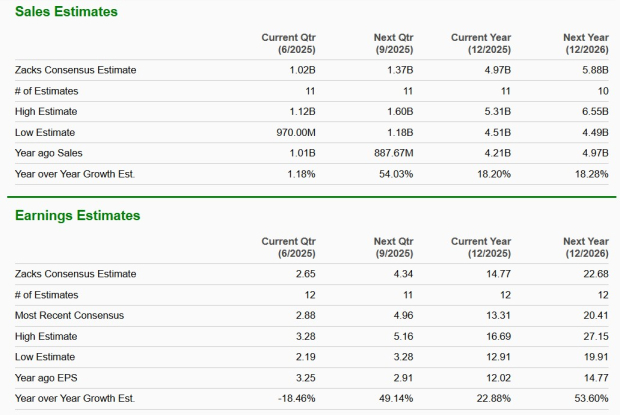

The company aims to sell 15.5-19.3 GW of solar modules (by 2025-end), which should bolster its revenue stream. As of March 31, 2025, First Solar entered into contracts with customers for the future sale of 66.1 GW of solar modules for an aggregate transaction price of $19.8 billion, which it expects to recognize as revenues through 2030. Solid revenue growth should duly aid the company’s bottom line as well.

In line with this, the Zacks Consensus Estimate for FSLR’s long-term (three to five years) earnings growth rate is pegged at 34.5%, better than the industry’s growth rate of 23.1%.

However, First Solar experienced manufacturing issues related to certain Series 7 modules produced in 2023 and 2024. As a result, the company incurred notable warranty charges in recent quarters. Going forward, warranty-related expenses linked to these Series 7 modules are expected to total between $56 million and $100 million, which could negatively impact its operational performance.

Additionally, in April 2025, the U.S. President announced a 10% “baseline” tariff on most trading partners, including Vietnam, India and Malaysia, along with increased tariffs on select countries. Although the higher tariffs have been paused for 90 days, the 10% tariff remains applicable to most nations. Since First Solar manufactures modules in these regions, the tariffs could increase production costs, affect international operations and weigh on overall results. The company has already revised its 2025 guidance downward to reflect the anticipated impact of these tariff changes.

Now let’s take a quick sneak peek at its near-term estimates to see what trend they reflect.

The Zacks Consensus Estimate for FSLR’s 2025 and 2026 revenues indicates a solid improvement of 18.2% and 18.3%, respectively, from the prior-year levels. The estimate for its earnings also indicates a year-over-year improvement.

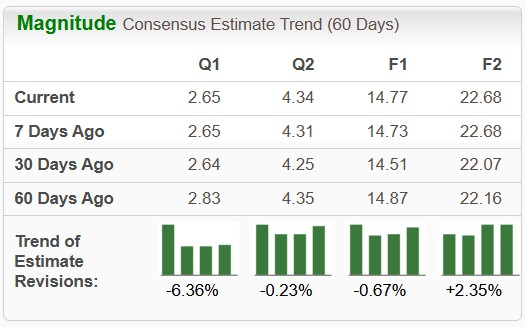

However, the downward revision in its near-term quarterly and annual (except 2026) estimates over the past 60 days indicates investors’ declining confidence in the stock’s earnings generation capabilities.

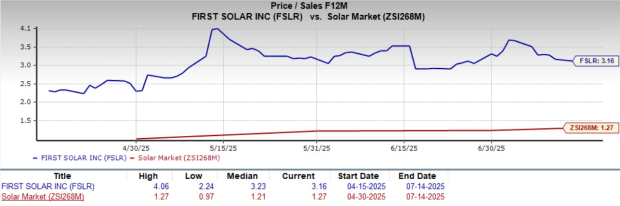

FSLR shares are expensive on a relative basis, with its forward 12-month Price/Sales (P/S F12M) being 3.16X compared with its industry average of 1.27X.

Its industry peers, CSIQ and SEDG, are trading at a discount in comparison with FSLR. CSIQ is trading at a P/S F12M of 0.13X, while SEDG is trading at a P/S F12M of 1.30X.

Investors interested in FSLR should wait for a better entry point, considering its premium valuation, downward revision in near-term earnings estimates and risks associated with tariff imposition.

However, those who already own this Zacks Rank #3 (Hold) stock may continue to do so, taking into account its upbeat sales estimates, solid stock price performance and long-term growth prospects.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite