|

|

|

|

|||||

|

|

|

Over the last six months, BankUnited’s shares have sunk to $36.34, producing a disappointing 7.7% loss - a stark contrast to the S&P 500’s 5.2% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in BankUnited, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why we avoid BKU and a stock we'd rather own.

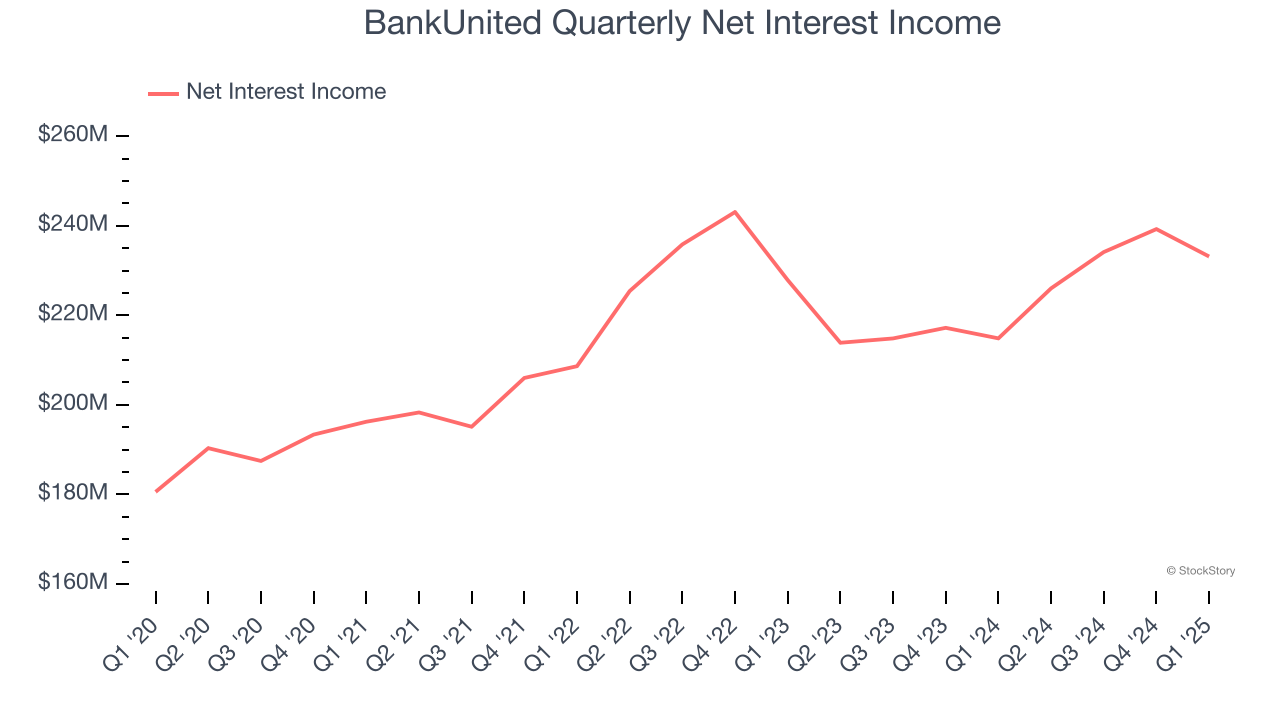

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

BankUnited’s net interest income has grown at a 5% annualized rate over the last four years, worse than the broader bank industry. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

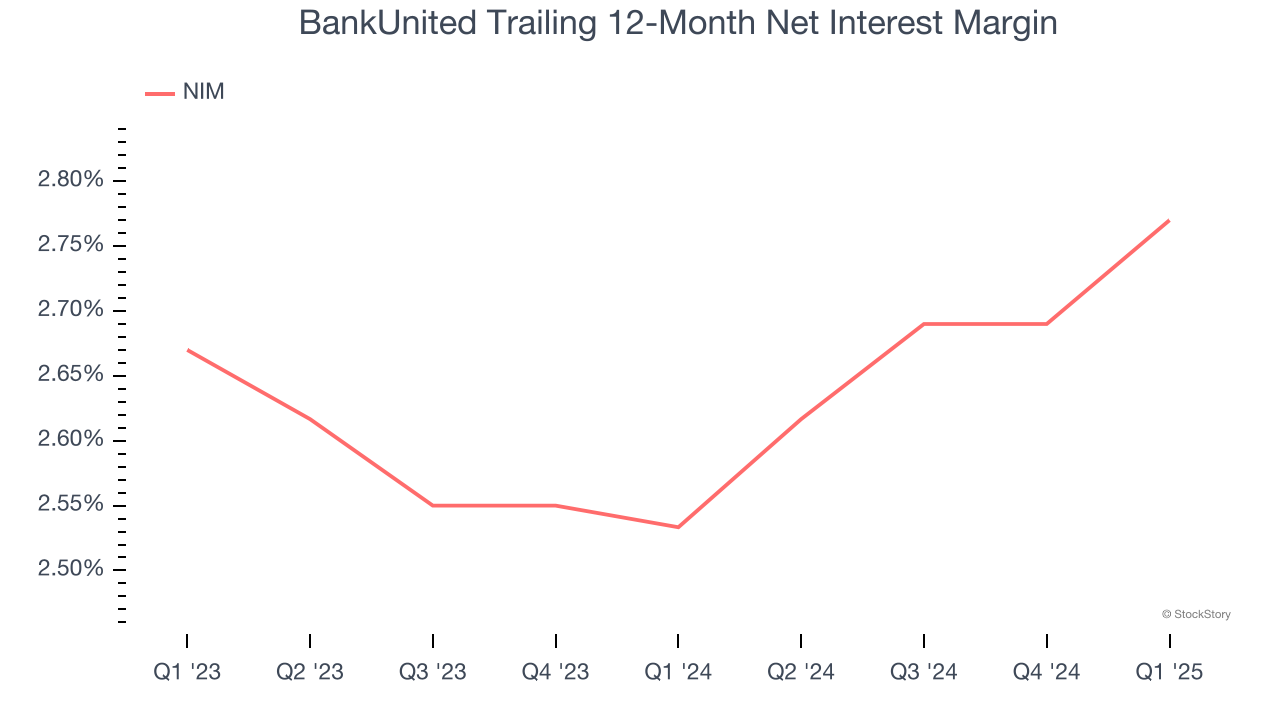

Net interest margin represents how much a bank earns in relation to its outstanding loans. It’s one of the most important metrics to track because it shows how a bank’s loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, we can see that BankUnited’s net interest margin averaged a poor 2.7%, meaning it must compensate for lower profitability through increased loan originations.

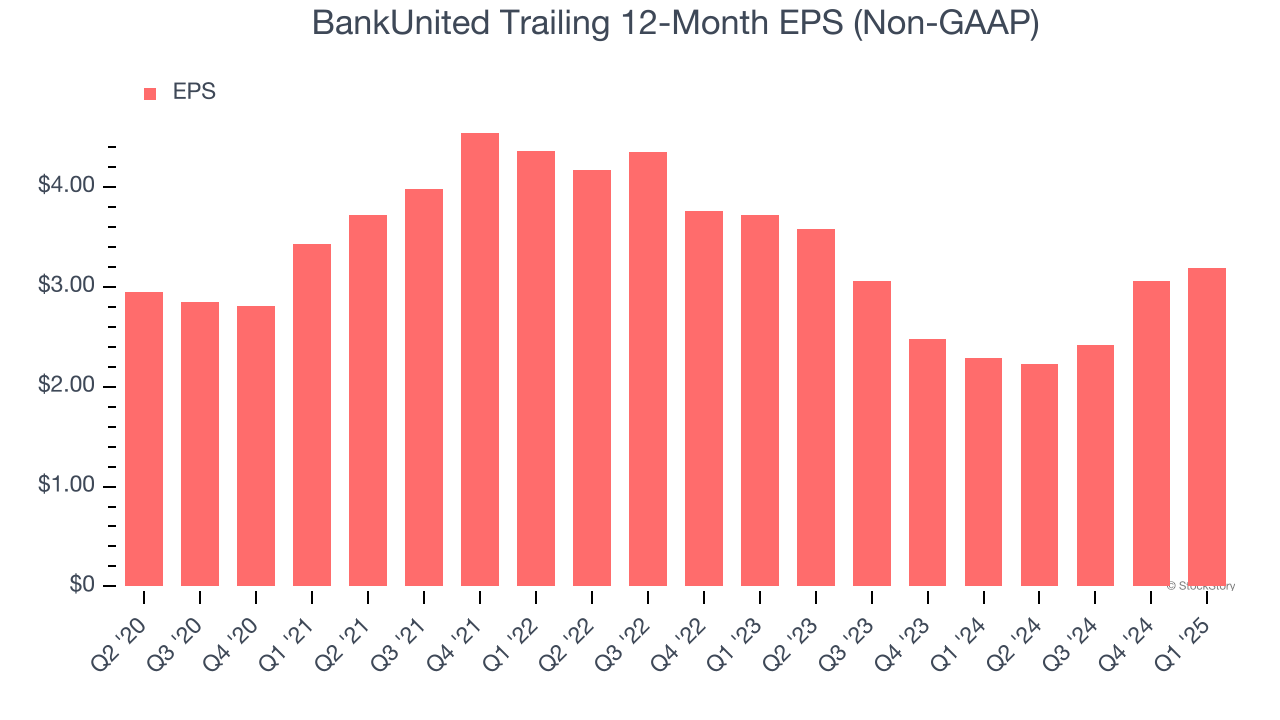

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

BankUnited’s unimpressive 2.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

BankUnited isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 0.9× forward P/B (or $36.34 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Apr-06 | |

| Mar-31 | |

| Mar-31 | |

| Mar-26 | |

| Mar-10 | |

| Mar-10 | |

| Mar-06 | |

| Mar-04 | |

| Mar-02 | |

| Feb-27 | |

| Feb-26 | |

| Feb-23 | |

| Feb-20 | |

| Feb-13 | |

| Feb-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite