|

|

|

|

|||||

|

|

|

Axon Enterprise, Inc. AXON and Teledyne Technologies Incorporated TDY are two prominent names operating in the aerospace and defense equipment industry. As rivals, both companies are engaged in manufacturing highly engineered public security and digital imaging solutions in the United States and internationally. Both companies have been enjoying significant growth opportunities in the public safety and surveillance industries on account of growing instances of terrorism and criminal activities across the world. Let’s take a closer look at their fundamentals, growth prospects and challenges.

The strongest driver of Axon’s business at the moment is the persistent strength in its Connected Devices segment. Growing popularity for its next-generation TASER 10 products and growth in cartridge revenues, supported by the higher adoption of the TASER products, have been driving the segment’s performance, of late. The segment’s revenues increased 26.1% year over year in the first quarter of 2025.

Axon introduced its next-generation body-worn camera, Axon Body 4, in 2023. Featuring upgraded features like a bi-directional communications facility and point-of-view camera module option, this body camera is generating significant demand, thus boosting the segment’s growth.

The company is also witnessing strong momentum in its Software & Services segment. Solid growth in the aggregate number of users of the Axon network is driving the Software & Services segment’s results. After witnessing a year-over-year increase of 33.4% in 2024, revenues from the segment also increased 39% in the first quarter.

Higher demand for digital evidence management and premium add-on features has also been supporting the segment’s growth. Strong customer satisfaction and engagement have led to a growing base of annual recurring revenues (ARR), which increased 34% year over year to $1.1 billion in the first quarter.

With almost 70% of AXON’s domestic user base still on basic plans, the Software & Services segment holds significant growth potential. New product introductions and add-on features are likely to continue playing an important role in its overall growth as customers are increasingly adopting products like Draft One and the OSP 10 premium bundle.

On the flip side, escalating costs and expenses are a concern for Axon’s margins and profitability. In first-quarter 2025, its cost of sales and SG&A expenses increased 18.2% and 48%, respectively, year over year. Total operating expenses climbed 54.7% year over year to $374.5 million. AXON incurred high costs and expenses related to business integration activities, an increase in headcount, and higher wages and stock-based compensation expenses.

Steady improvement in commercial air travel remains a major growth catalyst for Teledyne, with it being a notable provider of onboard avionics systems and ground-based applications for commercial aircraft. Notably, its first-quarter sales from the Aerospace and Defense Electronics segment improved 30.6% year over year, with commercial sales constituting 20% growth.

Teledyne’s Digital Imaging segment has been witnessing strength driven by higher sales of commercial infrared imaging components and surveillance systems. Increased demand for the company’s high-performance image sensors and digital cameras has been augmenting the segment’s performance. The Digital Imaging segment’s first-quarter sales were $757 million, reflecting an increase of 2.2%.

However, TDY experienced supply-chain challenges, including increased lead times, as well as cost inflation for parts and components, logistics and labor due to availability constraints and high demand in the recent past. This has also delayed the company’s ability to convert backlog to revenues and negatively impacted its profit margin in the past few quarters. To this end, the International Air Transport Association (IATA) announced in its December 2024 report that it expects severe supply-chain issues to continue to impact the aviation industry into 2025.

The escalating costs and operating expenses have also been major headwinds for the company. For instance, its cost of sales in the first quarter totaled $830 million, representing an increase of 7.8% year over year. Its SG&A expenses increased 6.5% in the same period. High costs and expenses, if not controlled, might adversely impact its margins and profitability.

High debt levels have also been a major concern for TDY as they raise financial obligations and might drain its profitability. Teledyne exited first-quarter 2025 with a long-term debt (net of current portion) of $2.96 billion, reflecting an increase of 12% sequentially. Its current liabilities were $1.36 billion, much higher than the cash equivalents of $461.5 million.

In the past six months, Axon shares have risen 25.6%, while Teledyne stock has gained 12.9%.

The Zacks Consensus Estimate for AXON’s 2025 sales and earnings per share (EPS) implies year-over-year growth of 27.2% and 6.7%, respectively. Although the EPS estimates for 2025 have decreased over the past 60 days, the estimate for 2026 has increased.

The Zacks Consensus Estimate for TDY’s 2025 sales implies growth of 6.8% year over year, while the EPS estimate indicates an increase of 8.8%. TDY’s EPS estimates have been trending northward for both 2025 and 2026 over the past 60 days.

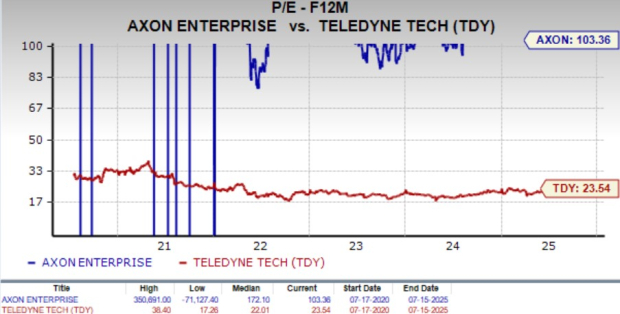

Teledyne is trading at a forward 12-month price-to-earnings ratio of 23.54X, while Axon’s forward earnings multiple sits much higher at 103.36X.

Axon’s diversified product portfolio, growth investments and persistent strength in the Connected Devices and Software & Services segments provide it with a competitive advantage to leverage the long-term demand prospects in the public safety markets. Despite its steeper valuation, AXON holds robust prospects due to strong estimates, stock price appreciation and better forecasts for sales and profit growth.

In contrast, Teledyne’s strength in the Aerospace & Defense as well as Digital Imaging segments has been dented by the supply-chain challenges and rising operating costs and expenses. Also, TDY’s highly leveraged balance sheet warrants a cautious approach for existing investors.

Given these factors, AXON seems a better choice for investors than TDY currently. While AXON carries a Zacks Rank #3 (Hold), TDY currently carries a Zacks Rank #4 (Sell). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 11 hours | |

| Jul-17 | |

| Jul-14 | |

| Jul-12 | |

| Jul-08 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite