|

|

|

|

|||||

|

|

|

Sales and earnings peaked during the pandemic, but the business fundamentals remain strong.

The swimming pool distributor is building out its digital footprint to create stickier sales channels.

Pool has a strong recurring revenue stream to weather the ups and downs in new pool construction.

Pool Corporation (NASDAQ: POOL) was a pandemic darling. In the two-year stretch from 2020 to 2021, the stock surged nearly 167%. People were flush with stimulus cash, interest rates were low, and it seemed like everyone wanted to build their own backyard Xanadu.

Since then, it's been much tougher swimming. Shares of Pool Corp. have drifted 14% lower over the past three years, and the stock is down about 10% so far in 2025. Is this a good opportunity to buy an industry leader on the dip?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

Pool Corp. is the world's largest wholesale distributor of swimming pool equipment and supplies, and a leading distributor of irrigation and landscaping products in the United States. Through its nearly 450 locations in North America, Europe, and Australia, Pool Corp. distributes more than 200,000 products to roughly 125,000 wholesale customers, who include pool builders and remodelers, service companies, retailers, and landscaping contractors.

The company's revenue and earnings peaked during the pandemic pool boom. In 2022, net sales hit a high-water mark of $6.2 billion -- nearly double its 2019 sales. Diluted earnings per share (EPS) of $18.70 were an all-time high as well, nearly 200% higher than 2019 EPS.

Up against those lofty comps, the past two-and-a-half years have been a bit sobering. Year-over-year sales declined 10% in 2023 and 4% in 2024, respectively. In the first quarter of 2025, sales dipped 2% on a same-selling-days basis, which adjusts for the number of business days in the quarter.

Tough comps haven't been the only challenge. Higher inflation and higher interest rates have been a double whammy for the pool industry. It's estimated that 61,000 in-ground pools were installed in 2024 -- down from 117,000 in 2021. In February, CEO Peter Arvan said that consumer discretionary spending that requires financing "remains a headwind."

While Pool Corp. isn't swimming in pandemic-era profits anymore, the business isn't sinking. Far from it. In 2024, the company generated $5.3 billion in net sales, with only 14% of sales coming from new pool construction. Nearly 65% of Pool Corp.'s revenue came from maintenance, repair, and replacement products -- things like water-treatment chemicals, pumps, filters, and cleaning equipment.

This is steady, recurring revenue that helps Pool Corp. weather the ups and downs in the housing market and the overall economy. Importantly, we're talking about non-discretionary spending, which means these are unavoidable expenses that are required to keep pools safe, clean, and functional. As the installed base of in-ground pools gets older, Pool Corp. expects steady demand for both essential repairs and aesthetic upgrades -- from replacing worn-out pumps to refreshing tile, lighting, and landscaping.

Pool Corp.'s investments in its digital ecosystem should drive continued growth in repair and maintenance sales. Its Pool360 software tools help pool professionals manage their businesses more efficiently, while improving their customers' experiences. Through the Pool360 platform, builders, remodelers, service providers, and retailers can order directly from Pool Corp.'s e-commerce site, which has buoyed sales of its private-label chemicals.

On the consumer side, Pool Corp. recently launched the Regal and E-Z Clor mobile apps to help homeowners maintain healthy pool chemistry. The apps can analyze water-test results and provide a diagnosis if there's a problem, along with specific product recommendations.

Pool Corp.'s growing suite of digital tools for pool pros and consumers should create stickier sales channels, build customer loyalty, and drive sales of higher-margin in-house products.

Even with in-ground pool installation down nearly 50% since 2021, Pool Corp. has had four consecutive years of annual sales topping $5 billion, thanks to steady contributions from its maintenance and repair sales. In first-quarter 2025, net sales clocked in at $1.1 billion. The company said it expects full-year diluted EPS between $11.10 and $11.60, compared to $11.30 in 2024.

In 2024, Pool Corp. generated $659.2 million in operating cash flow, and maintained a solid 11.6% operating margin. What's just as important is how the company deploys its cash. Pool Corp. passes that test with its strong track record of reinvesting in the business and returning general amounts of capital to shareholders.

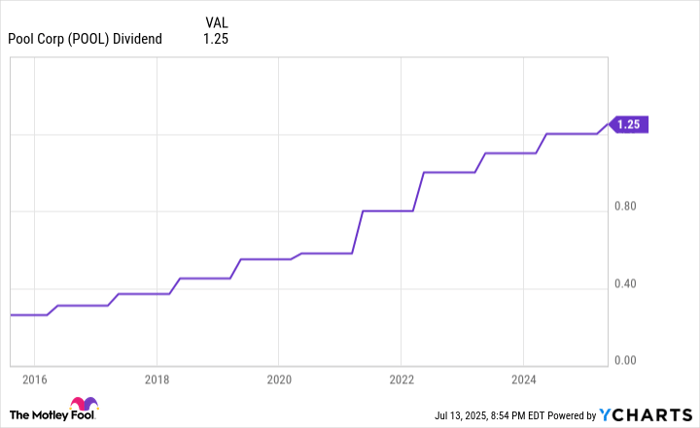

Since its inception as a public company, Pool Corp. has spent 46% of its cash -- $2.7 billion -- on share buybacks, and 21% on dividends. In April, Pool Corp. increased its quarterly dividend by 4% to $1.25 per share. As a shareholder, this is the kind of chart you love to see.

POOL Dividend data by YCharts.

Pool Corp.'s stock trades at a forward price-to-earnings (P/E) ratio of 28, compared to its average P/E of 29.6 over the past decade. With strong cash flow, a growing digital ecosystem, and a shareholder-friendly capital allocation strategy, there's a lot to like here. I'm wary of the pool industry's sensitivity to economic cycles. However, Pool Corp.'s recurring revenue stream is a stabilizing force -- and a strong foundation for growth when market conditions improve.

Before you buy stock in Pool, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pool wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $679,653!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,046,308!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 179% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of July 15, 2025

Josh Cable has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

| Jul-15 | |

| Jul-09 | |

| Jun-16 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-05 | |

| Jun-05 | |

| Jun-05 | |

| May-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite