|

|

|

|

|||||

|

|

|

American Woodmark’s stock price has taken a beating over the past six months, shedding 34.4% of its value and falling to $53.13 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy American Woodmark, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we're cautious about American Woodmark. Here are three reasons why AMWD doesn't excite us and a stock we'd rather own.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, American Woodmark struggled to consistently increase demand as its $1.71 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect American Woodmark’s revenue to drop by 2.7%. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

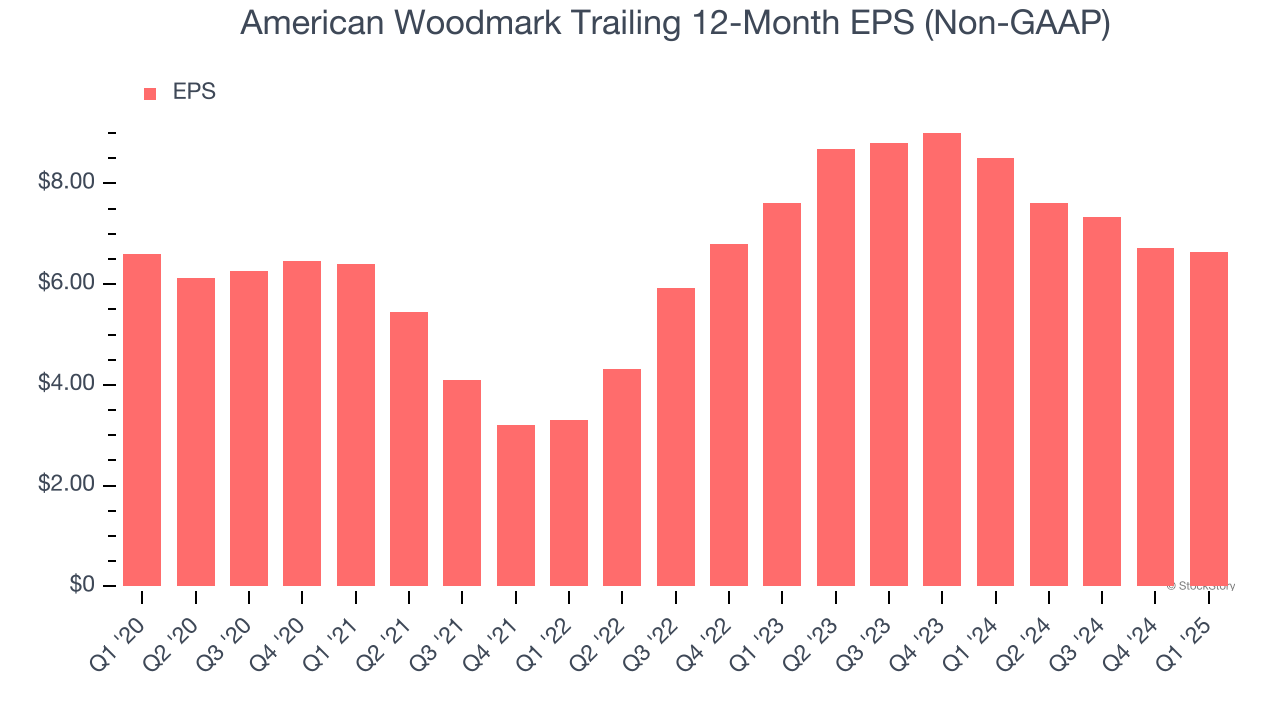

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

American Woodmark’s EPS was flat over the last five years, just like its revenue. This performance was underwhelming across the board.

American Woodmark doesn’t pass our quality test. After the recent drawdown, the stock trades at 8.6× forward P/E (or $53.13 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d recommend looking at one of our top digital advertising picks.

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| May-28 | |

| May-27 | |

| Apr-19 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-11 | |

| Feb-04 | |

| Dec-15 | |

| Nov-25 | |

| Nov-25 | |

| Nov-21 | |

| Nov-12 | |

| Oct-30 | |

| Oct-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite