|

|

|

|

|||||

|

|

|

Hologic HOLX is set to release third-quarter fiscal 2025 results on July 30, after the closing bell.

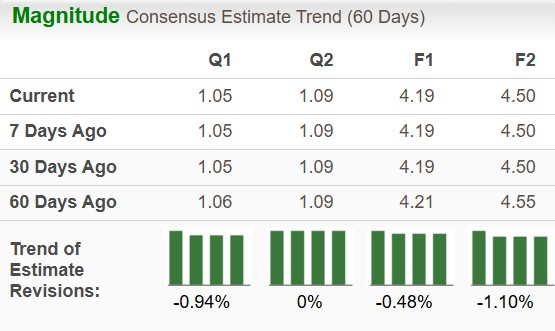

The Zacks Consensus Estimate for third-quarter earnings per share (EPS) suggests a 0.9% decrease year over year to $1.05. The estimate has dropped by 1 cent in the past 60 days. The Zacks Consensus Estimate for third-quarter revenues currently stands at $1.01 billion, suggesting a 0.4% decline year over year.

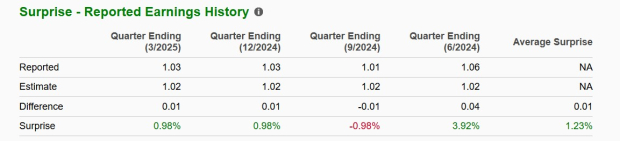

The U.S. medical device maker focusing on women’s health has a mixed record over the trailing four quarters. It topped estimates in three quarters and missed on one occasion. On average, the earnings surprise came in at 1.23%.

Per our proven model, a stock with a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), along with a positive Earnings ESP, has a higher chance of beating estimates, which is not the case here.

Earnings ESP: Hologic has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks Rank #1 stocks here.

Starting with the largest division, Diagnostics’ performance in the fiscal third quarter may have been mixed. Molecular Diagnostics is expected to have favorably impacted revenues, with the BV/CV/TV assay being a key contributor. Hologic has been working to drive awareness and reimbursement of the test to address a large unmet need in the U.S. vaginitis market. The Biotheranostics oncology business is likely to have continued to benefit from the ongoing adoption of the Breast Cancer Index (“BCI”) test. However, the loss of the HIV testing business in Africa following the halt of USAID funding is expected to have weighed on growth.

In cytology and perinatal businesses, Hologic is likely to have witnessed the robust U.S. adoption of the Genius AI product. Meanwhile, international performance is expected to have suffered, particularly due to ongoing headwinds in China. Tariffs, increasing local competition and rising anti-American sentiment, along with more available alternatives, are expected to affect overall segment results. Our model forecasts a 1.1% decline year over year in Diagnostics revenues to $436 million.

We also expect the company’s Breast Health segment to sustain the recent downward trend from lower capital equipment sales. However, recurring service revenues — tied to Hologic’s large installed base — may have helped offset some declines. Endomagnetics is likely to have entered the second half of the year with strong momentum, positively contributing to the Interventional Breast portfolio. Still, tariffs are expected to have posed challenges as a bulk of these products are manufactured outside the United States. According to our model, Breast Health revenues in the fiscal third quarter are likely to decrease 4.7% year over year to $366.8 million.

Similarly, the GYN Surgical segment also may have faced tariff pressure in the fiscal third quarter, given that a majority of these products are made in Costa Rica. Despite that, robust international sales are likely to have supported growth. The Fluent Pro Fluid Management System may have continued gaining traction. Further, ongoing integration of the newly acquired Gynesonics is expected to have positively contributed to Hologic’s revenues in the to-be-reported quarter. Our model forecasts Surgical division revenues to improve 6.4% year over year to $177.3 million.

Further, Hologic’s production ramp-up of the Horizon DXA system in Skeletal Health in the second quarter is likely to have been carried into the to-be-reported quarter as well. Our model estimates 40.2% growth in the Skeletal business, reaching $26.6 million.

In the past year, Hologic shares have declined 18.5%, steeper than the industry’s 15.7% fall and the Zacks Medical sector’s 17.6% drop. The company also underperformed peers Abbott ABT and QIAGEN QGEN, which have risen 19.6% and 12.8%, respectively.

Valuation-wise, Hologic is trading at a forward five-year Price/Sales (P/S) of 3.35X, lower than the industry average of 4.01X. The stock is graded a Value Score of B at present.

Hologic continues to yield robust growth and durability, benefiting from its presence in both Diagnostics and Medtech. Across each of its franchises, the company offers products that are widely recognized and often seen as the standard of care, such as ThinPrep and cervical cancer screening on Panther instrument in Molecular Diagnostics, 3D Genius mammography in Breast Health business and MyoSure for the treatment of fibroids in the Surgical business. Hologic’s international business also drives strong top-line performance, reflecting its ability to capture potential opportunities into reality. Backed by a strong balance sheet and disciplined approach to capital allocation, the company continues to strengthen its foundation with acquisitions like Endomagnetics and Gynesonics.

That said, Hologic remains exposed to macroeconomic volatility. Tariffs tied to its manufacturing activities in Costa Rica and China could increase inventory acquisition costs by $20-$25 million per quarter in fiscal 2025, pressuring margins. The company reduced its China revenue forecast by $20 million amid tougher operating conditions, now projecting only $50 million. Further, currency headwinds forecasted for this year are approximately $10-$15 million. Hologic expects a low-single-digit decline in Breast Health, while Diagnostics growth is expected to be limited by Africa weakness and lower sales in China.

Hologic’s weak top and bottom-line projections for the fiscal third quarter, together with industry and broader macroeconomic challenges weighing on business segments, are likely to continue dragging its stock performance. While the company has several key drivers that promise long-term growth, including valuable inorganic additions, its near-term headwinds warrant a more cautious stance. Hence, at this stage, HOLX stock may not present a favorable entry point. Those already invested may find it wise to exit.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Abbott Bounds Higher After Hiking 2026 Profit View On Second-Quarter Beat

ABT +10.71%

Investor's Business Daily

|

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite