|

|

|

|

|||||

|

|

|

Curtiss-Wright currently trades at $474.48 and has been a dream stock for shareholders. It’s returned 416% since July 2020, blowing past the S&P 500’s 94.7% gain. The company has also beaten the index over the past six months as its stock price is up 23.5% thanks to its solid quarterly results.

Following the strength, is CW a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Formed from a merger of 12 companies, Curtiss-Wright (NYSE:CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

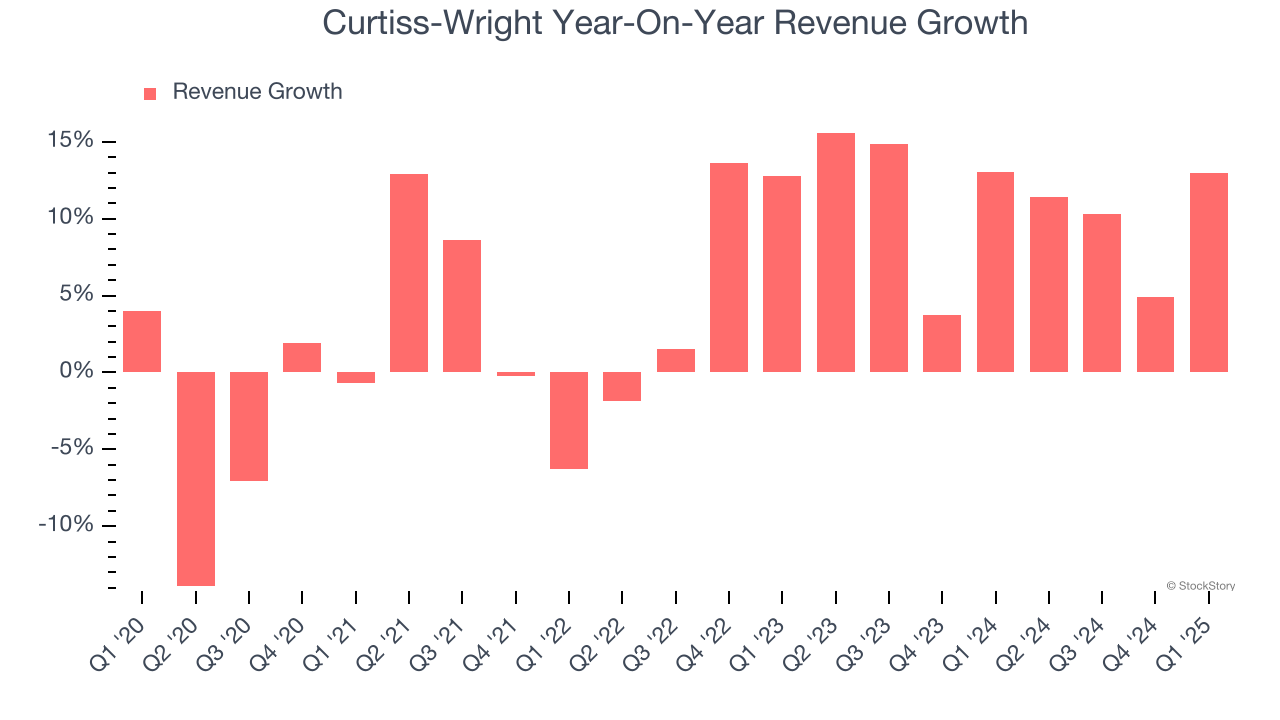

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Curtiss-Wright’s annualized revenue growth of 10.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

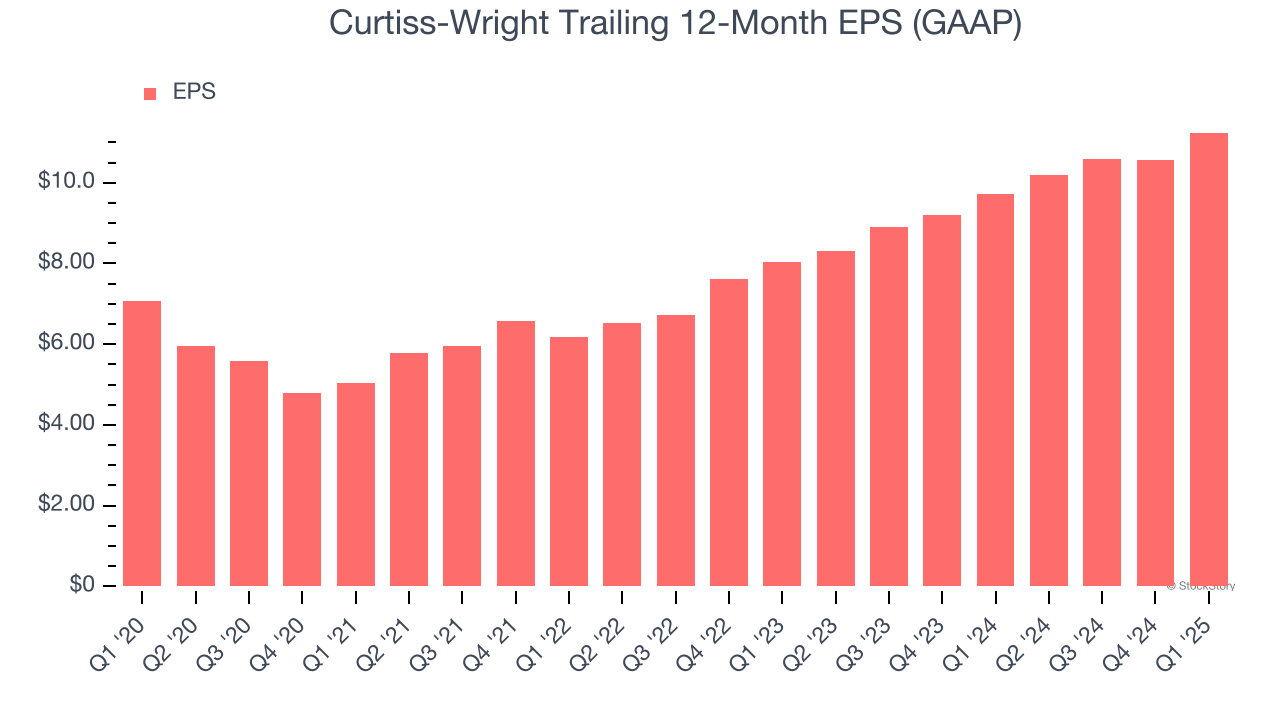

Curtiss-Wright’s EPS grew at a decent 9.7% compounded annual growth rate over the last five years, higher than its 5.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Curtiss-Wright’s revenue to rise by 7.4%, a deceleration versus its 5.1% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Curtiss-Wright has huge potential even though it has some open questions, and with its shares beating the market recently, the stock trades at 37.8× forward P/E (or $474.48 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-02 | |

| Mar-02 | |

| Feb-24 | |

| Feb-22 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-12 | |

| Feb-12 |

Howmet Aerospace Pops. Earnings, Upgrade Fuel Bullish Defense Surge.

CW +5.80%

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite