|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Huntington Ingalls has had an impressive run over the past six months as its shares have beaten the S&P 500 by 20.9%. The stock now trades at $253.23, marking a 24% gain. This performance may have investors wondering how to approach the situation.

Is now the time to buy Huntington Ingalls, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons why HII doesn't excite us and a stock we'd rather own.

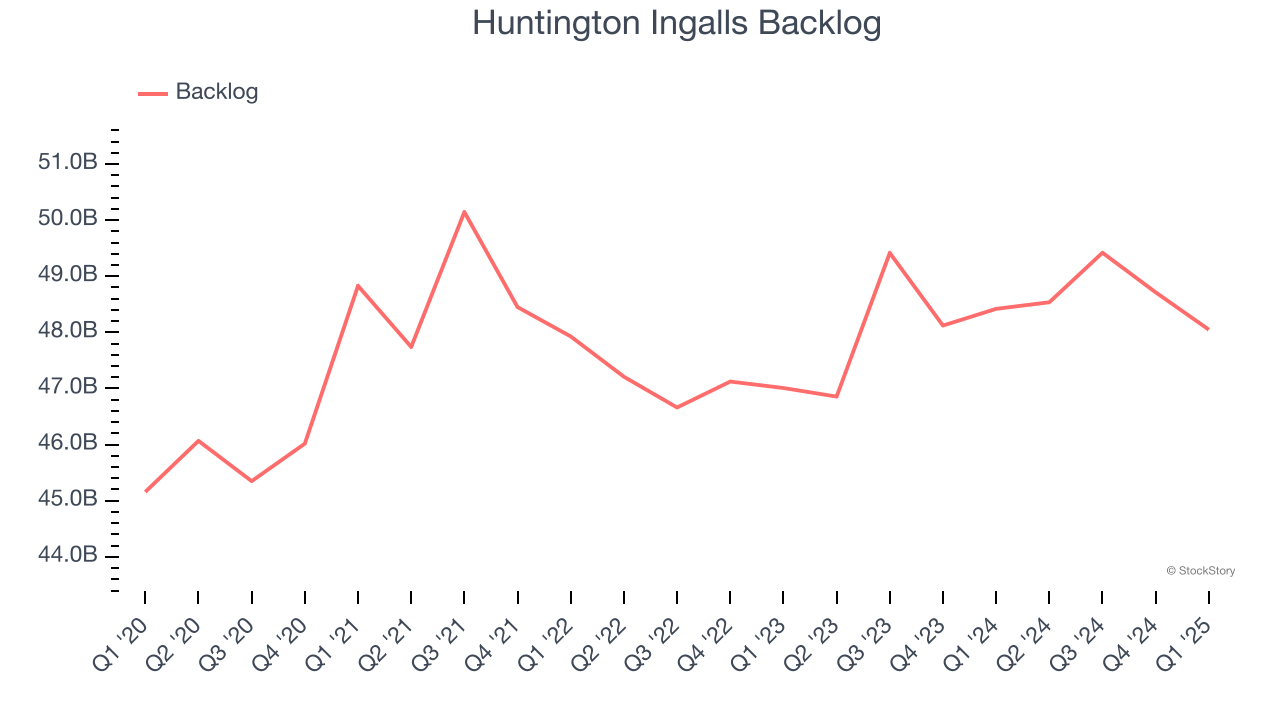

Investors interested in Defense Contractors companies should track backlog in addition to reported revenue. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Huntington Ingalls’s future revenue streams.

Huntington Ingalls’s backlog came in at $48.05 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 1.8%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

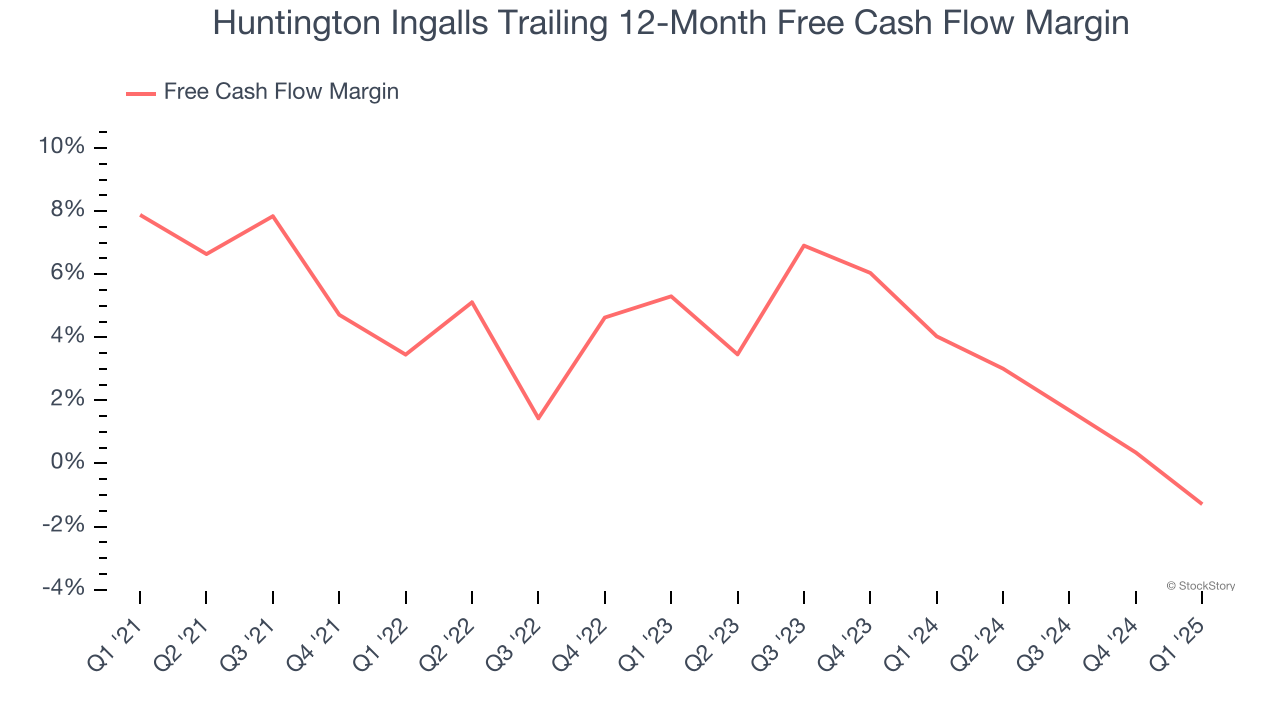

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Huntington Ingalls’s margin dropped by 9.2 percentage points over the last five years. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business. Huntington Ingalls’s free cash flow margin for the trailing 12 months was negative 1.3%.

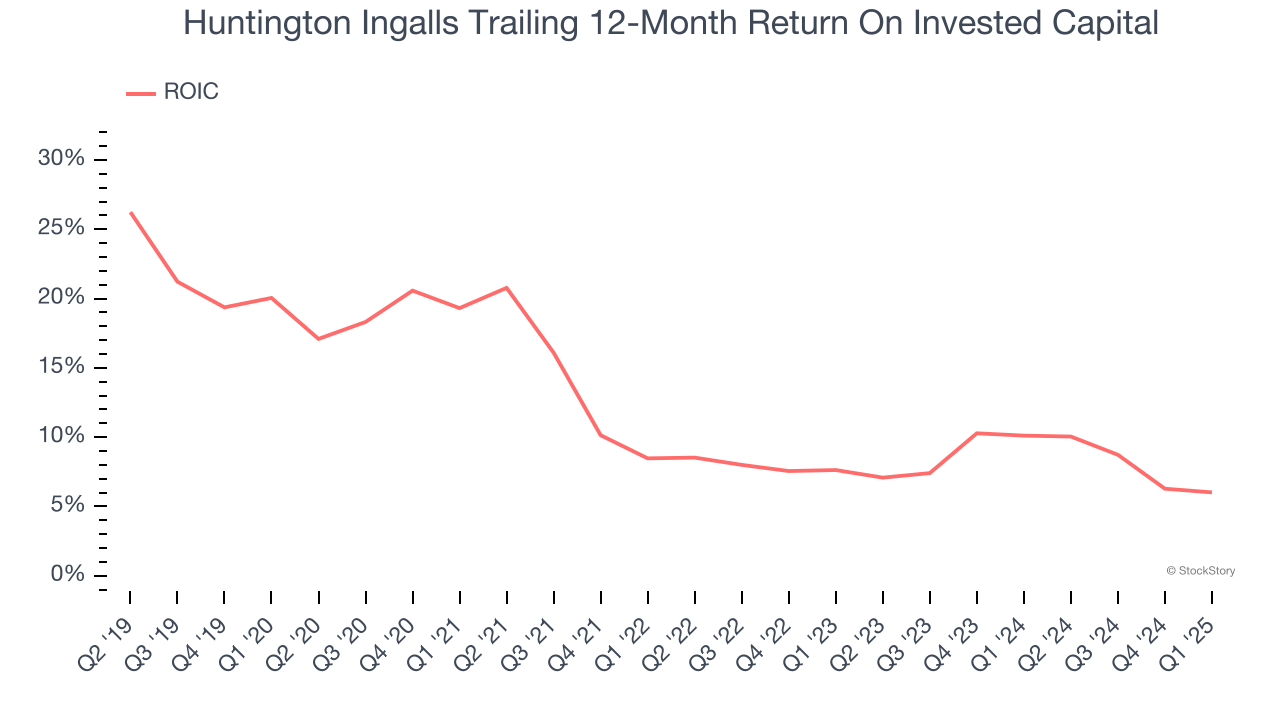

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Huntington Ingalls’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Huntington Ingalls falls short of our quality standards. With its shares outperforming the market lately, the stock trades at 17.9× forward P/E (or $253.23 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d suggest looking at the Amazon and PayPal of Latin America.

Trump’s April 2024 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Feb-19 | |

| Feb-18 | |

| Feb-17 | |

| Feb-16 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 |

Pentagon To Punish Habitually Late Contractors. These Defense Stocks Fall

HII

Investor's Business Daily

|

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-06 | |

| Feb-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite