|

|

|

|

|||||

|

|

|

Tractor Supply Company TSCO has reported second-quarter 2025 results, wherein the top and bottom lines surpassed the Zacks Consensus Estimate. Also, net sales and earnings increased from the year-ago period.

Tractor Supply has posted earnings of 81 cents per share, which beat the Zacks Consensus Estimate of 80 cents. Also, the bottom line increased 2.5% from the figure reported in the prior-year quarter.

Net sales grew 4.5% year over year to $4.44 billion. Also, sales surpassed the Zacks Consensus Estimate of $4.40 billion. The increase in sales can be attributed to store openings and an increase in comparable store sales.

Comparable store sales grew 1.5% year over year, reversing the 0.5% decline registered in the prior year’s second quarter. The improvement reflects a 1% rise in average transaction count and a 0.5% increase in average ticket size.

Growth in comparable sales was fueled by strong performance in year-round categories, particularly consumable, usable and edible (C.U.E.) products, as well as solid demand for spring seasonal items. Apparel, gift and decor, and big-ticket items also contributed positively. However, gains were partially offset by weaker results in select discretionary categories.

Tractor Supply Company price-consensus-eps-surprise-chart | Tractor Supply Company Quote

Gross profit increased 5.4% year over year to $1.64 billion. The gross margin improved 30 basis points year over year to 36.9%, primarily driven by effective product cost management and the continued execution of the company’s everyday low price strategy. Our model predicted gross profit to increase 4.4% and the gross margin to expand 30 bps to 36.9%.

Selling, general and administrative (SG&A) expenses, including depreciation and amortization, rose 6.8% to $1.06 billion from $994.2 million in the second quarter of 2024. As a percentage of net sales, SG&A increased to 23.9% from 23.4%. This rise was largely due to planned investments in growth initiatives and modest fixed cost deleverage, given the pace of comparable store sales growth.

These impacts were partially offset by ongoing productivity improvements, cost controls, and a modest benefit from the company's sale-leaseback program. Our model predicted SG&A expenses to increase 5.1% and as a percentage of sales, this metric was anticipated to expand 30 bps to 21.1%.

Operating income for the quarter grew 2.9% year over year to $577.8 million. Meanwhile, the operating margin fell 20 bps to 13%. We estimated operating income to increase 0.2% and the operating margin to contract 40 bps to 12.8%.

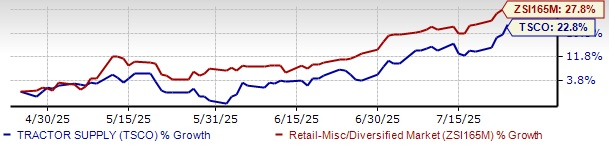

TSCO Stock Past Three-Month Performance

Tractor Supply ended the quarter with cash and cash equivalents of $225.8 million, long-term debt of $1.67 billion, and total stockholders’ equity of $2.49 billion. In the six months ended June 28, 2025, net cash provided by operating activities was $1 billion. In the same period, the company incurred a capital expenditure of $351.6 million.

In the second quarter, Tractor Supply returned $195.9 million to shareholders. This included the repurchase of 1.4 million shares of its common stock for $73.9 million and the payment of $122 million in quarterly cash dividends.

In the second quarter of 2025, the company continued to expand its footprint by opening 24 Tractor Supply stores and two Petsense by Tractor Supply locations. One Petsense by Tractor Supply store was closed during the period.

Tractor Supply is reaffirming its financial guidance for fiscal 2025. The company continues to expect net sales growth of 4-8% and comparable store sales growth of 0-4%. The operating margin rate is projected between 9.5% and 9.9%. Net income is expected between $1.07 billion and $1.17 billion, with earnings per share anticipated to be $2.00-$2.18.

For the year, Tractor Supply expects total share repurchases of $325-$375 million. This Zacks Rank #4 (Sell) company’s shares have gained 22.8% in the past three months compared with the industry’s 27.8% growth.

Some better-ranked stocks are Levi Strauss & Co. LEVI, Stitch Fix SFIX and Urban Outfitters Inc. URBN.

Levi designs and markets jeans, casual wear and related accessories for men, women and children. It flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Levi’s current fiscal-year earnings indicates growth of 4% from the year-ago actuals. LEVI delivered a trailing four-quarter average earnings surprise of 25.9%.

Stitch Fix delivers customized shipments of apparel, shoes and accessories for women, men and kids. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Stitch Fix’s current fiscal-year earnings implies growth of 71.7% from the year-ago actual. SFIX delivered a trailing four-quarter average earnings surprise of 51.4%.

Urban Outfitters is a lifestyle specialty retailer that offers fashion apparel and accessories, footwear, home décor and gift items. It presently has a Zacks Rank of 2.

The Zacks Consensus Estimate for Urban Outfitters’ current fiscal-year earnings and sales indicates growth of 22.2% and 8.5%, respectively, from the year-ago actuals. URBN delivered a trailing four-quarter average earnings surprise of 29%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-15 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite