|

|

|

|

|||||

|

|

|

Nebius Group N.V. NBIS, a fast-growing artificial intelligence (AI) infrastructure provider, is forecasting a return to positive adjusted EBITDA in the second half of 2025, driven by accelerating revenues, global expansion and focus on tech innovation. NBIS is gaining from solid growth in its core AI business. As organizations increasingly invest in generative AI, Nebius is benefiting from a full-stack approach, offering everything from high-performance GPU cloud infrastructure to Saturn Cloud’s MLOps platform and AI development tools. The company recently announced the general availability of NVIDIA GB200 Grace Blackwell Superchip capacity for its customers in Europe.

Its expanding global infrastructure footprint, with data centers now across the United States, Europe and the Middle East, bodes well. To gain a larger share of the AI cloud compute market, NBIS is focusing on technical enhancements that increase reliability and reduce downtime to boost customer retention. In the first quarter, Nebius significantly upgraded its AI cloud infrastructure through improvements to its Slurm-based cluster. Nebius expanded integrations with external AI platforms like Metaflow, D Stack and SkyPilot, enabling customers to migrate tools with nominal friction.

To support growth, the company is doubling down on AI infrastructure with an ambitious $2 billion capital expenditure plan for 2025, up from its earlier guidance of $1.5 billion.

Nebius reported a 385% year-over-year revenue surge for the first quarter of 2025, reaching $55.3 million. It expects full-year revenues between $500 million and $700 million, backed by strong AI and cloud infrastructure demand. Over the medium term, the company anticipates EBIT margins to be within the 20% to 30% range, supported by the continued scaling of its AI cloud business.

However, NBIS’ path to profitability will require careful navigation. Despite a positive turn in the second half of 2025, management reaffirms that adjusted EBITDA will be negative for full-year 2025. The company is currently in a high-growth phase, which naturally comes with elevated capital expenditures and operational costs. Moreover, increasing market competition and macroeconomic uncertainties may adversely impact NBIS’ growth trajectory.

Nebius competes with technology giants like CoreWeave, Inc. CRWV and Microsoft Corporation MSFT.

CoreWeave’s first-quarter 2025 results show enormous growth, with revenues jumping 420% year over year to about $981.6 million. A backlog of $25.9 billion (including an $11.9 billion OpenAI deal) and partnerships with IBM and other AI labs underline strong demand. The adjusted operating income rose 550% year over year to $163 million, while adjusted EBITDA surged nearly 6x to $606 million, with margin improving from 55% to 62%. However, CoreWeave has become highly leveraged. It carried about $18.8 billion in total liabilities after the first quarter, of which $8.7 billion was debt. Interest expense swelled to roughly $264 million in the first quarter as a result. The company expects interest expense to remain elevated at $260-$300 million for the current quarter. It anticipates capex to be between $20 billion and $23 billion for 2025 due to accelerated investment in the platform to meet customer demand.

Microsoft Corporation operating income was $32 billion and increased 16% (up 19% in cc) in the third-quarter fiscal 2025. The operating margin expanded 110 basis points to 45.7% on a year-over-year basis. However, operating margins are expected to decrease approximately one point in fiscal 2025 due to elevated capital investments outpacing revenue growth. The company’s operating expenses rose 2.4% year over year, while it spent $21.4 billion on capex and $16.7 billion on cash for PP&E. For the fourth quarter, MSFT anticipates operating expenses to increase in the $18-$18.1 billion range. For fiscal 2026, capex is estimated to grow at a slower rate than in fiscal 2025, with a higher share of short-lived assets.

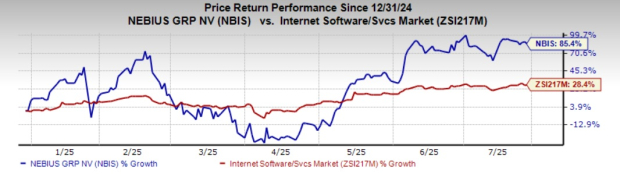

Shares of Nebius have gained 85.4% year to date compared with the Internet – Software and Services industry’s growth of 28.4%.

In terms of price/book, NBIS’ shares are trading at 3.83X, down from the Internet Software Services industry’s ratio of 4.25.

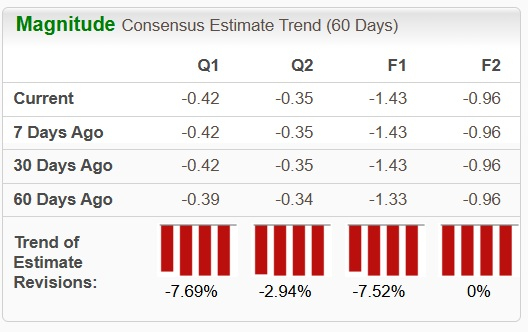

The Zacks Consensus Estimate for NBIS’ earnings for 2025 has been unchanged over the past 30 days.

NBIS currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite