|

|

|

|

|||||

|

|

|

Altria Group, Inc. MO is slated to report its second-quarter 2025 earnings on July 30, before market open.

The Zacks Consensus Estimate for second-quarter revenues stands at $5.2 billion, indicating a 1.7% decline from the same period last year. On the contrary, the consensus mark for earnings has moved up by a cent in the past 30 days to $1.37 per share, indicating 4.6% growth from the year-ago quarter’s reported figure.

Altria has a trailing four-quarter average earnings surprise of 1.3%. In the last reported quarter, the company’s bottom line surpassed the Zacks Consensus Estimate by a margin of 5.1%.

As investors prepare for Altria’s second-quarter announcement, the question looms regarding earnings beat or miss. Our proven model predicts an earnings beat for MO this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is exactly the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Altria has an Earnings ESP of +1.03% and a Zacks Rank #3 at present. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Altria Group, Inc. price-consensus-eps-surprise-chart | Altria Group, Inc. Quote

Altria is expected to have been hurt by regulatory and market pressures, most notably the ITC’s exclusion order on NJOY ACE, which led to a full halt in shipments after the first quarter. This development removed Altria’s only FDA-authorized e-vapor product from the market, significantly impacting its smoke-free portfolio. Meanwhile, the company is likely to have continued to face volume pressure in its cigarette business, driven by ongoing consumer downtrading, macroeconomic strain, and competition from illicit flavored disposable vapes, which now dominate the e-vapor landscape.

However, Altria’s performance is likely to have been supported by strong pricing power and disciplined cost controls. The company’s ability to implement targeted price increases and manage its Marlboro brand through store-level analytics is likely to have helped preserve profitability even as volumes softened. Margin expansion, which was evident in the first quarter, is expected to have carried through into the second quarter, helping offset revenue headwinds from the regulatory disruption and volume softness. In addition, Altria will likely have benefited from cost savings under its Optimize & Accelerate initiative, aimed at streamlining operations and driving efficiency across the organization.

While the removal of NJOY ACE represents a setback for its smoke-free strategy, Altria’s continued focus on cost discipline and operational execution is likely to have helped maintain earnings stability in the second quarter.

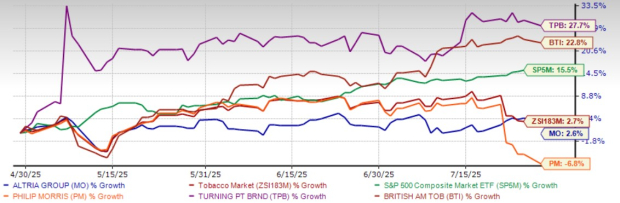

Over the past three months, Altria’s stock has advanced 2.6%, closely matching the Zacks Tobacco industry’s growth of 2.7%, though trailing the broader S&P 500, which rose 15.5% during the same period. While not the top performer, Altria outpaced Philip Morris International Inc. PM but underperformed Turning Point Brands, Inc. TPB and British American Tobacco p.l.c. BTI. Philip Morris declined 6.8%, while British American Tobacco rose 22.8%. Shares of Turning Point Brands led the group with a standout 27.7% gain over the three months.

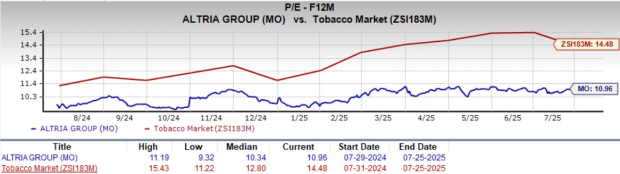

From a valuation perspective, Altria shares are trading at a discount relative to the industry average. With a forward 12-month price-to-earnings ratio of 10.96, below the industry’s average of 14.48, the stock offers compelling value for investors seeking exposure to the sector.

This valuation gap becomes even more pronounced when compared to key competitors. Philip Morris International trades at a P/E ratio of 20.11, while Turning Point Brands stands at 21.54, both significantly higher than Altria’s multiple. In contrast, British American Tobacco trades at a lower P/E of 10.94, placing it closer to Altria in terms of valuation.

With regulatory headwinds clouding its smoke-free strategy and volume challenges persisting in the core cigarette business, Altria heads into its second-quarter earnings with a mixed backdrop. However, signs of resilient pricing power, disciplined cost control, and an appealing valuation may offer a cushion against near-term volatility. Given the stock’s relative stability, earnings beat potential, and value-driven appeal, cautious optimism seems warranted. Investors may consider holding their positions or selectively adding on weakness, while closely watching management’s commentary on product pipeline updates and long-term strategic execution.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite