|

|

|

|

|||||

|

|

|

Pagaya Technologies Ltd. PGY and OneMain Holdings, Inc. OMF are both consumer finance companies focused on catering to the underserved credit market -- subprime and non-prime borrowers. While Pagaya uses artificial intelligence (AI)-powered machine learning to optimize credit underwriting and securitization, OneMain operates as a brick and mortar and digital lender serving non-prime borrowers.

Can PGY’s AI-powered growth momentum subdue OMF’s proven marketplace supremacy? While both face headwinds from shifting consumer spending patterns and market uncertainties, let’s decipher which stock is better placed for long-term growth.

With an adaptable business model and capital-efficient structure, Pagaya initially focused on personal loans. Over time, the company expanded into auto lending and point-of-sale financing, reducing exposure to any single loan type and improving resilience across economic cycles.

To diversify its funding, PGY has built a network of more than 135 institutional partners and utilizes forward flow agreements—pre-arranged deals where investors commit to buying future loans. These agreements offer funding stability, especially during market disruptions.

A key differentiator is Pagaya’s proprietary tech and product suite. Its pre-screen solution allows lenders to present pre-approved offers to existing customers without formal applications, helping partners boost credit access and deepen relationships with minimal marketing spend.

Additionally, Pagaya operates with minimal on-balance-sheet exposure. Loans are typically acquired immediately by asset-backed securities (ABS) vehicles or via forward flow agreements, thanks to capital raised in advance. This approach limits credit and market risk, preserving flexibility during turbulent environments.

This model proved effective from 2021 to 2023 amid rising rates and tighter markets. By relying on forward flow agreements and strategic ABS issuance, Pagaya maintained liquidity and minimized loan write-downs.

Operating through 1,300 locations across 47 states, OneMain typically provides unsecured and secured personal installment loans, often used for debt consolidation, home improvements, medical expenses, and other large personal needs. It also offers optional credit and non-credit insurance products, such as life, disability and involuntary unemployment insurance.

Revenue growth has been a major strength for OneMain. Its loan mix of Front Book and Back Book aims for revenue sustainability while maintaining upside potential in a rapidly changing macroeconomic environment. OMF frequently securitizes portions of its loan book via OneMain Financial Issuance Trust to reduce funding costs and manage balance sheet exposure. Its 2024 acquisition of Foursight Capital LLC expanded its presence into the auto lending business.

As a subprime lender, OMF is more exposed to credit risk and macroeconomic cycles. However, the company employs rigorous underwriting and servicing, supported by centralized data analytics, and has a strong record of managing credit performance, even during downturns.

OMF focuses on sustainable shareholder returns through dividends and buybacks. Since initiating dividends in 2019, it has raised them seven times. A $1 billion buyback program launched in 2022 that extends through December 2026 reflects management’s emphasis on repurchases.

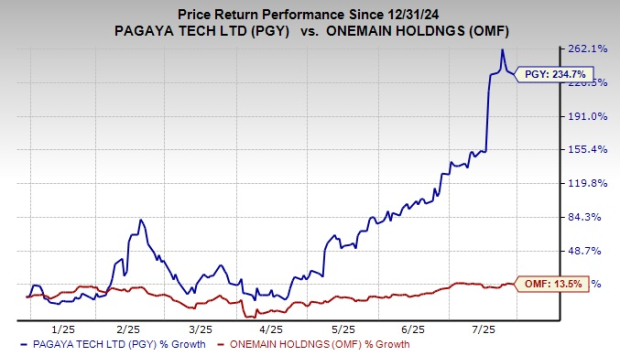

So far this year, shares of Pagaya have performed extremely well, given bullish investor sentiments. The stock has soared 234.7%, while OMF has gained 13.5%. Hence, in terms of investor sentiments, PGY has the edge.

From a valuation perspective, Pagaya is currently trading at a trailing 12-month price-to-book (P/B) of 5.34X, while OMF stock is trading at a trailing 12-month P/B of 2.15X.

So, in terms of valuation, PGY is expensive compared to OneMain.

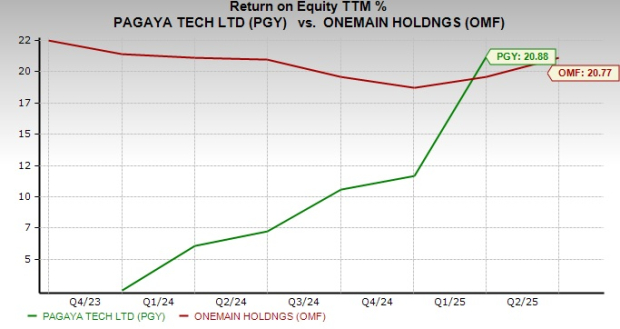

Pagaya’s return on equity (ROE) of 20.88% is marginally above OneMain’s 20.77%. This reflects that PGY is just slightly more efficient in using shareholder funds to generate profits.

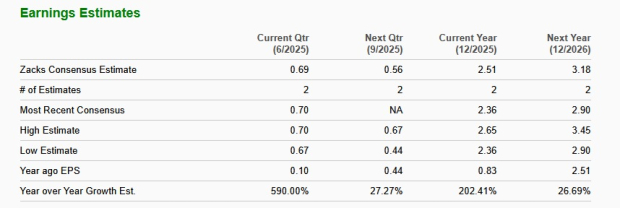

The Zacks Consensus Estimate for PGY’s 2025 and 2026 revenues indicates year-over-year growth of 23.6% and 18.3%, respectively.

The consensus estimate for PGY’s earnings indicates a 202.4% and 26.7% year-over-year jump in 2025 and 2026, respectively.

On the contrary, the Zacks Consensus Estimate for OMF’s 2025 and 2026 revenues implies a year-over-year increase of just 7.4% and 7.5%, respectively.

Also, the consensus estimate for OneMain’s earnings indicates 26.4% growth for 2025 and a 29.4% rise for 2026.

Pagaya is scaling rapidly with its flexible, capital-light model, AI-powered lending solutions and a strong network of funding partners. Its significantly stronger revenue and earnings growth prospects compared to OneMain enhance its appeal as a high-upside investment opportunity.

While OMF boasts a well-established marketplace model and a more attractive valuation, PGY’s compelling growth trajectory makes it better positioned for long-term gains, justifying the premium valuation.

PGY currently sports a Zacks Rank #1 (Strong Buy), whereas OneMain carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 | |

| Jul-09 | |

| Jul-08 | |

| Jun-30 | |

| Jun-15 | |

| Jun-11 | |

| Jun-10 | |

| Jun-08 | |

| May-27 | |

| May-26 | |

| May-21 | |

| May-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite