|

|

|

|

|||||

|

|

|

Howmet Aerospace Inc. HWM is scheduled to release second-quarter 2025 results on July 31, before market open. The Zacks Consensus Estimate for earnings is currently pegged at 87 cents per share on revenues of $1.99 billion.

The company’s second-quarter earnings estimates have increased a penny over the past 60 days. The bottom-line projection indicates an increase of 29.9% from the year-ago number. The Zacks Consensus Estimate for quarterly revenues indicates year-over-year growth of 5.8%.

Howmet has an impressive earnings surprise history. The company’s earnings outpaced the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 8.8%. In the last reported quarter, it delivered an earnings surprise of 11.7%.

Howmet Aerospace Inc. price-eps-surprise | Howmet Aerospace Inc. Quote

Our proven model predicts an earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

HWM has an Earnings ESP of +0.60% and a Zacks Rank of 3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Howmet has been witnessing solid momentum in the commercial aerospace market. The strength in air travel has been driving demand for wide-body aircraft, thereby supporting continued OEM spending. Pickup in air travel is generally positive for the company because the increased usage of aircraft spurs spending on parts and products that it provides.

Growing popularity for new, more fuel-efficient aircraft with reduced carbon emissions and increased spare demand for engines are likely to have proven favorable for HWM in the second quarter. The Zacks Consensus Estimate for revenues from the commercial aerospace market is pegged at $1.05 billion, indicating a 6.9% rise from the second-quarter 2024 number.

Howmet has also been benefiting from the persistent strength in the defense business, cushioned by steady government support. HWM has been experiencing robust orders for engine spares for the F-35 program and other legacy fighters. This is likely to have augmented its top-line performance in the quarter. The consensus estimate for revenues from the defense aerospace market is pegged at $343 million, indicating an 18.3% increase from the year-ago quarter’s number.

However, lower demand in the commercial transportation markets served by the Forged Wheels segment due to lower OEM builds is likely to have dragged its performance in the second quarter. Production issues at The Boeing Company BA due to quality control challenges are also expected to have affected narrow-body and wide-body production rates, which is likely to have affected its sales. The consensus estimate for revenues from the commercial transportation market is pegged at $305 million, indicating an 11.8% decrease on a year-over-year basis.

HWM is dependent on a global supply chain, and in recent years, it has experienced supply-chain disruptions in the aerospace sector that resulted in delays and increased costs. Despite moderation, the persistence of supply-chain issues in the aerospace sector is likely to have affected its operations and performance.

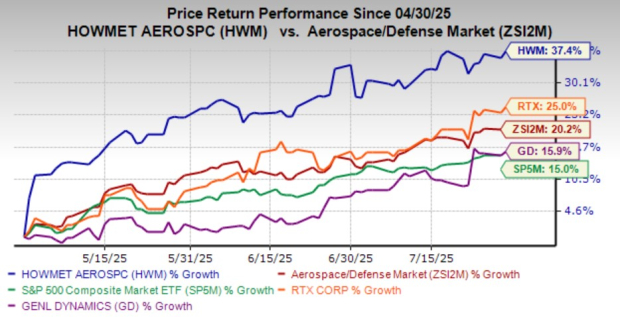

HWM shares have surged 37.4% in the past three months compared with the Zacks Aerospace - Defense industry’s 20.2% growth. The company’s shares have also fared comparatively better than the S&P 500’s increase of 15%. With respect to its major peers, RTX Corporation RTX and General Dynamics Corporation GD have gained 25% and 15.9%, respectively, in the same period.

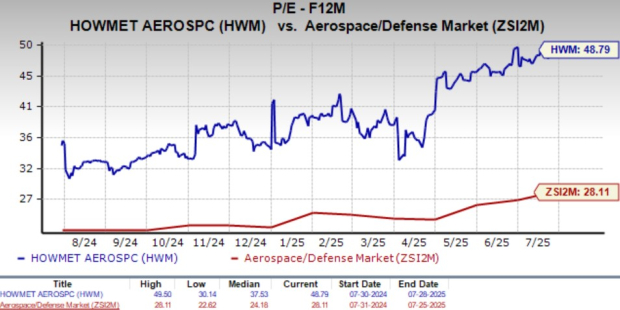

HWM is trading at a forward 12-month price-to-earnings (P/E) ratio of 48.79X, higher than the industry average of 28.11X. This elevated valuation could make the stock vulnerable to further pullbacks if market sentiment sours. In comparison with HWM’s valuation, its peers, RTX Corp. and General Dynamics, are trading cheaper. Notably, RTX Corp. and General Dynamics are currently trading at 24.48X and 19.29X, respectively.

Howmet's robust and diversified portfolio, along with its strength in the commercial and defense aerospace markets, seems promising for its long-term growth. The U.S. government’s enhanced budgetary provisions set the stage for HWM, focused on aerospace and defense businesses, to win more contracts, which is likely to have boosted its top line.

However, weakness in the commercial transportation market, along with supply-chain issues, has been concerning for its near-term performance. Also, the company’s expensive valuation warrants a cautious approach for existing investors.

Despite having strong fundamentals, Howmet has been witnessing some near-term challenges. Investors should monitor the developments pertaining to the stock closely for a more appropriate entry point, as an erroneous and hasty decision could affect portfolio gains. Therefore, it might be prudent to wait for HWM’s earnings report before making an investment decision.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours |

Boeing Wins Big As Farnborough Airshow Takes Off. Airbus, RTX Land Deals.

BA

Investor's Business Daily

|

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 10 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite