|

|

|

|

|||||

|

|

|

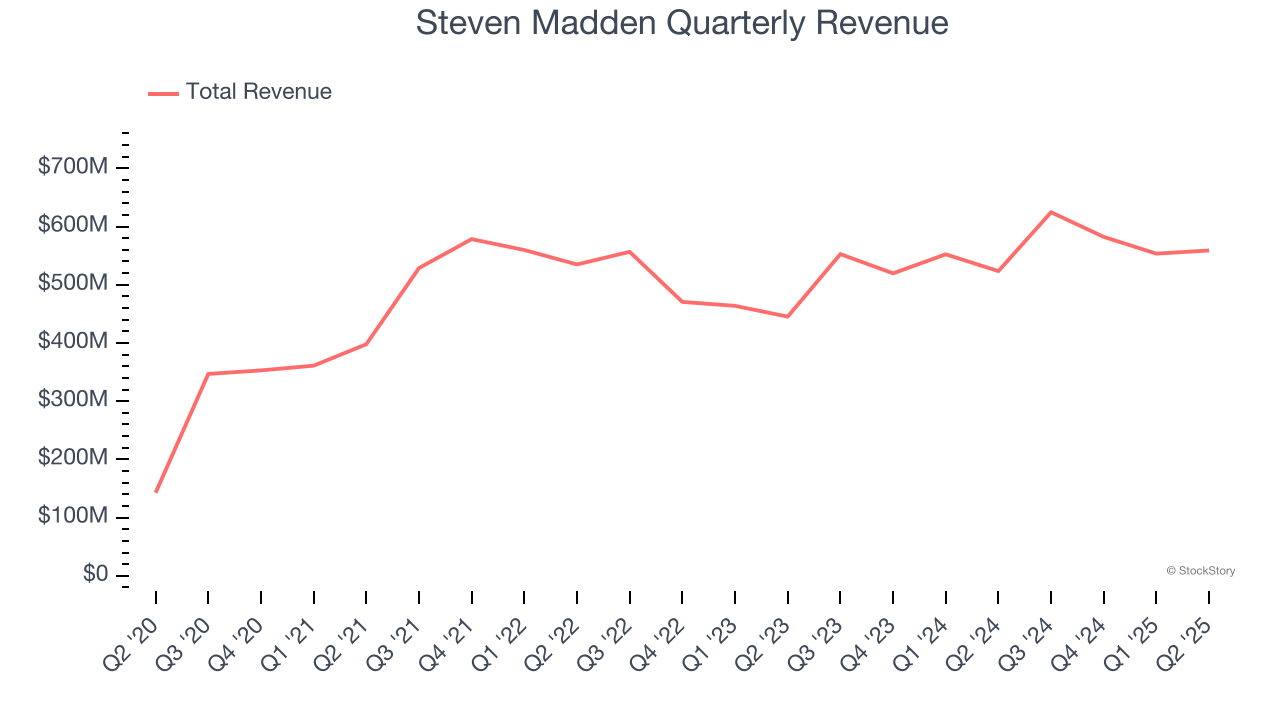

Shoe and apparel company Steven Madden (NASDAQ:SHOO) missed Wall Street’s revenue expectations in Q2 CY2025, but sales rose 6.8% year on year to $559 million. Its non-GAAP profit of $0.20 per share was 17% below analysts’ consensus estimates.

Is now the time to buy Steven Madden? Find out by accessing our full research report, it’s free.

Edward Rosenfeld, Chairman and Chief Executive Officer, commented, “As anticipated, the second quarter was challenging, driven largely by the impact of new tariffs on goods imported into the United States. Our team continues to act with agility to mitigate near-term impacts while remaining focused on positioning the company for long-term growth by executing our strategy to deepen consumer connections through the combination of compelling product and effective marketing. The integration of Kurt Geiger is proceeding smoothly, and we are more confident than ever in its potential to be a significant driver of growth for the company in the years ahead. While tariffs have created near-term pressure and added uncertainty, we believe our key strengths — powerful brands, a robust balance sheet and a proven business model — position us well to navigate the current environment and deliver sustainable growth over time.”

As seen in the infamous Wolf of Wall Street movie, Steven Madden (NASDAQ:SHOO) is a fashion brand famous for its trendy and innovative footwear, appealing to a young and style-conscious audience.

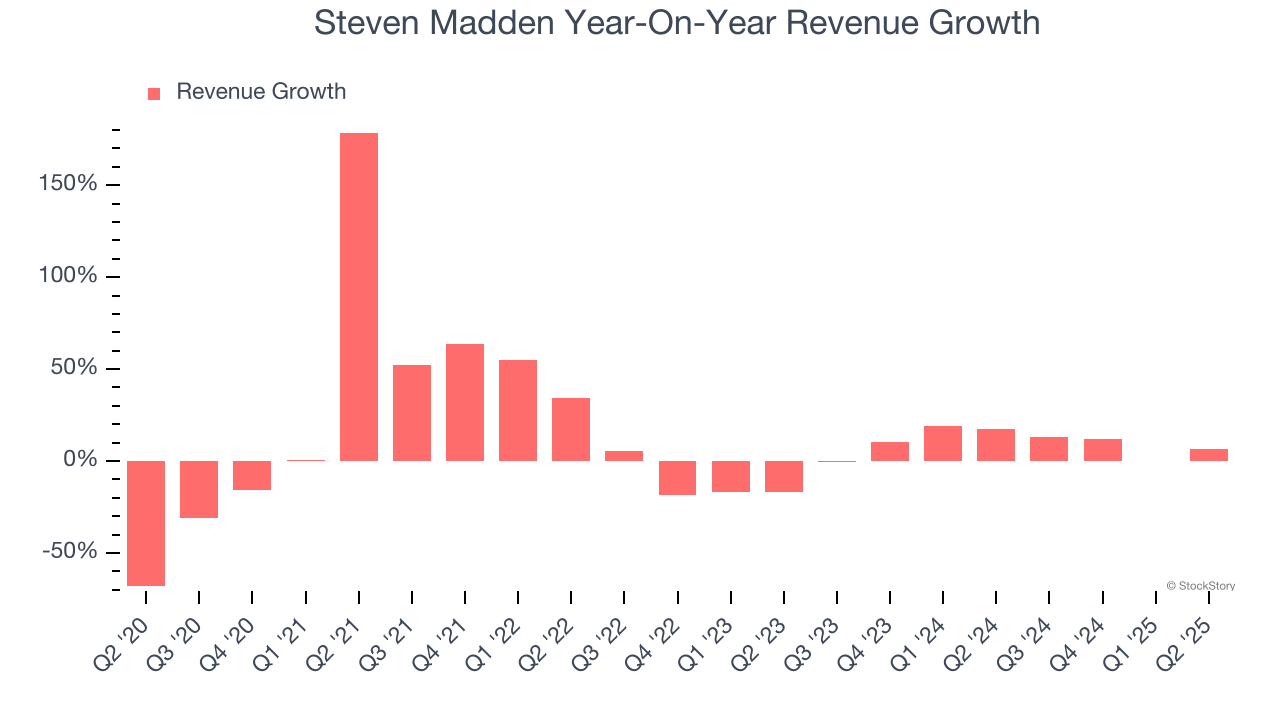

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Steven Madden grew its sales at a 10.3% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Steven Madden’s annualized revenue growth of 9.4% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Wholesale and Retail, which are 64.5% and 35% of revenue. Over the last two years, Steven Madden’s Wholesale revenue (sales to retailers) averaged 10% year-on-year growth while its Retail revenue (direct sales to consumers) averaged 9.8% growth.

This quarter, Steven Madden’s revenue grew by 6.8% year on year to $559 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 14.4% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and indicates its newer products and services will spur better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

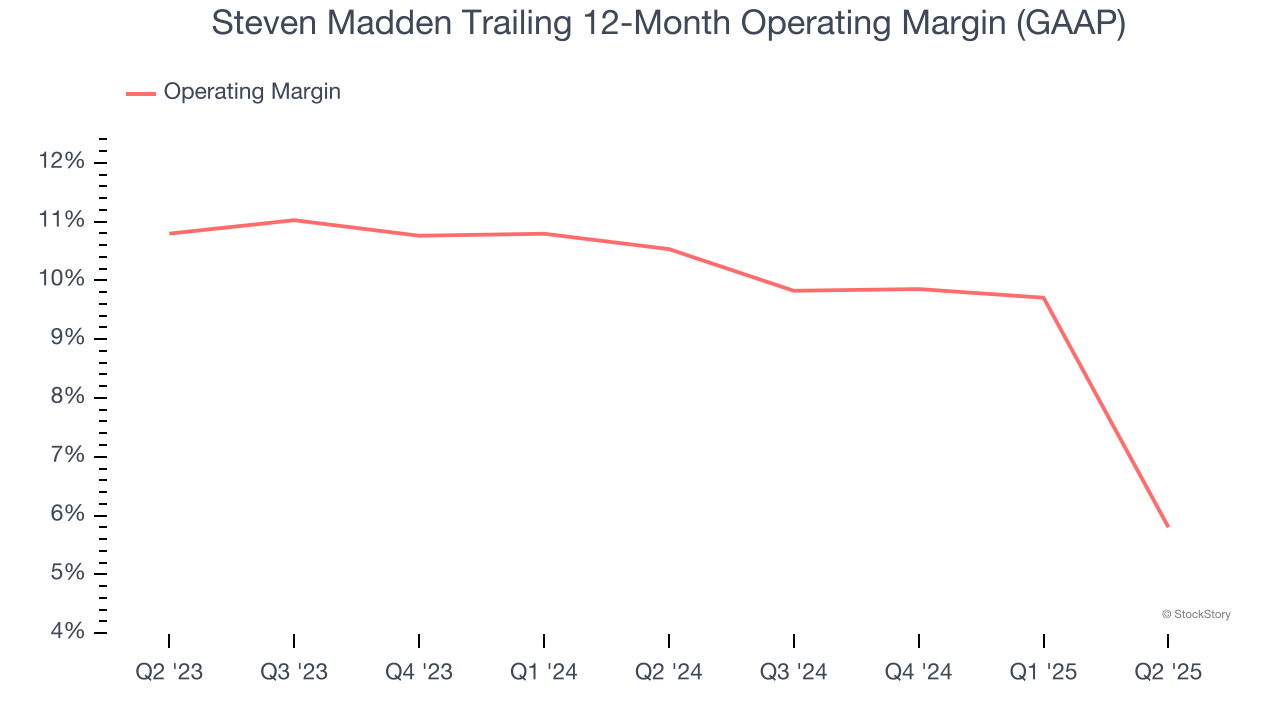

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Steven Madden’s operating margin has been trending down over the last 12 months and averaged 8.1% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Steven Madden generated an operating margin profit margin of negative 7.2%, down 16.2 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

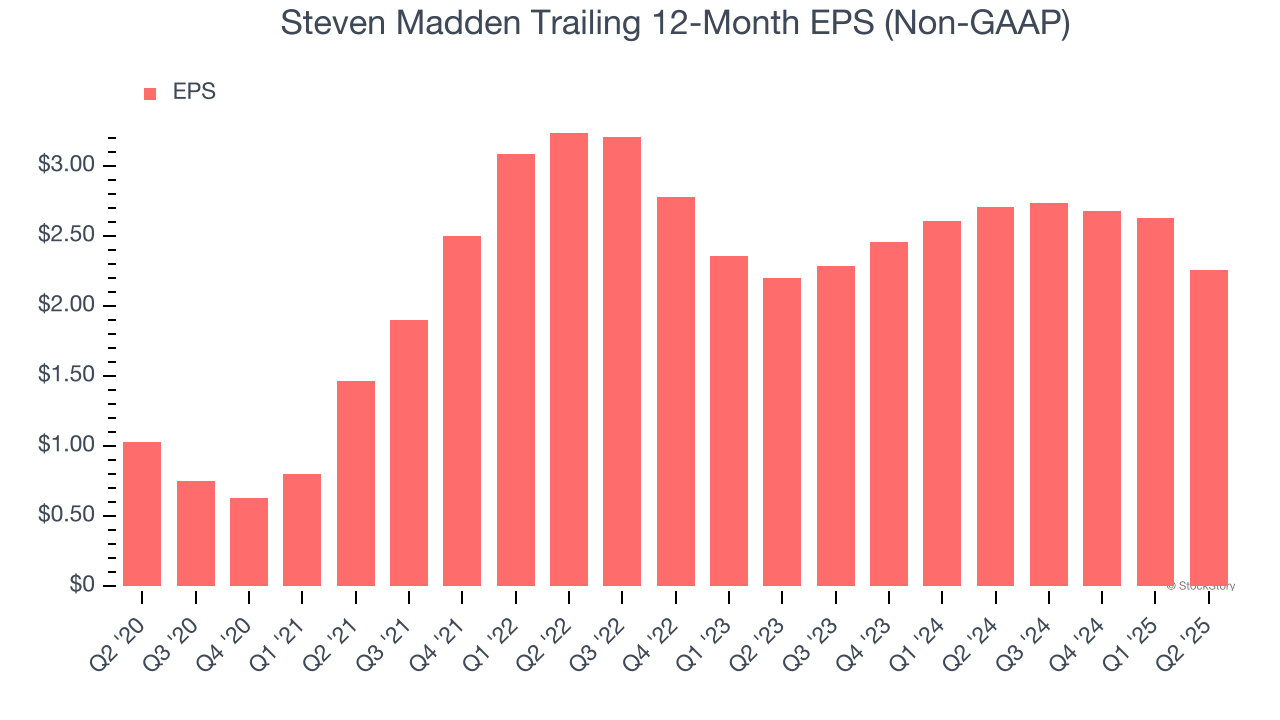

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Steven Madden’s EPS grew at a remarkable 17% compounded annual growth rate over the last five years, higher than its 10.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q2, Steven Madden reported EPS at $0.20, down from $0.57 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Steven Madden’s full-year EPS of $2.26 to shrink by 26.8%.

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 6.2% to $24.68 immediately following the results.

Steven Madden’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-23 | |

| Feb-22 | |

| Feb-17 | |

| Feb-16 | |

| Feb-12 | |

| Feb-12 | |

| Feb-10 | |

| Feb-09 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-02 | |

| Feb-02 | |

| Jan-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite