|

|

|

|

|||||

|

|

|

Avantor, Inc. AVTR reported second-quarter 2025 adjusted earnings per share (EPS) of 24 cents, down 4% from the year-ago quarter. The bottom line also missed the Zacks Consensus Estimate by 4%.

GAAP EPS for the quarter was 9 cents, down 35.7% year over year.

Revenues grossed $1.68 billion in the reported quarter, down 1.1% year over year. However, the metric surpassed the Zacks Consensus Estimate by 0.4%.

Avantor's foreign currency translation had a positive impact of 2% and M&A had a negative impact of 3%, resulting in flat sales on an organic basis.

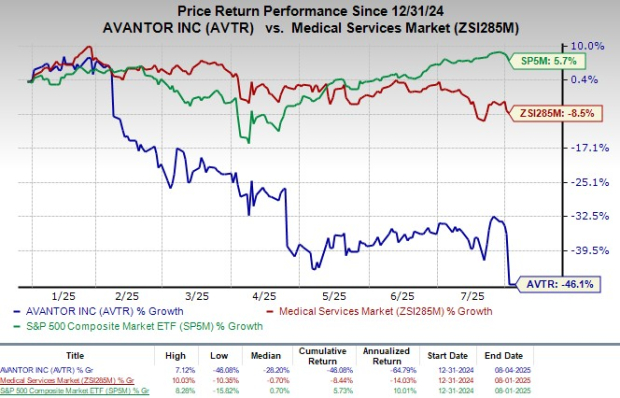

Shares of this company plunged 15.5% till Friday’s trading. The company’s shares have lost 46.1% in the year-to-date period compared with the industry’s decline of 8.5%. The broader S&P 500 Index has increased 5.7% in the same time frame.

The Laboratory Solutions segment’s net sales were $1.12 billion, reflecting a reported decrease of 2.9% year over year. Organic sales decreased 1% year over year in the reported quarter. This figure compares to our segmental projection of $1.05 billion.

Per management, the segment faced ongoing competitive intensity, particularly among large biopharma accounts, driven by macroeconomic and policy-related pressures. To protect and grow market share, Avantor executed strategic pricing actions and extended major contracts, including a five-year extension with BIO Business Solutions, its largest customer group, securing access to over 10,000 companies. The self-manufactured lab chemicals business continued its growth streak, while performance was regionally mixed, with Europe outperforming the Americas and Asia. However, margin pressure persisted due to price concessions, unfavorable mix, and under absorption of fixed costs, resulting in an 11.9% adjusted operating margin.

Bioscience Production’s net sales were $561.3 million, reflecting a reported increase of 2.6%, whereas organic sales increased 1.5% year over year. This figure compares to our segmental projection of $557 million.

Per management, Bioprocessing (representing about two-thirds of the segment) was flat year over year, missing expectations due to two key headwinds: extended planned maintenance at a manufacturing facility, which caused a rise in backorders, and unexpected disruptions from a few large customers—including regulatory and safety setbacks at a gene therapy platform, reduced outlook from an mRNA customer, and a negative Phase III result from a mAbs partner.

CEC declined mid-single digits year over year but grew sequentially; single-use systems and process ingredients posted sequential growth but remained flat to low single digits year over year. Outside bioprocessing, the NuSil medical-grade silicones platform delivered low-double-digit growth, outpacing procedure volumes, though a customer inventory rebalance is expected to temper second-half growth. Segment operating income was $140 million with a 24.9% margin, down year over year due to under absorption and manufacturing-related costs. Looking ahead, Avantor expects the bioprocessing headwinds to persist through year-end and is focused on improving supply chain execution, ramping commercial intensity, and expanding its product portfolio.

Avantor, Inc. price-consensus-eps-surprise-chart | Avantor, Inc. Quote

In the quarter under review, Avantor’s gross profit declined 4.7% year over year to $554.1 million. The gross margin contracted 120 basis points (bps) to 32.9%. We had projected 34.3% of gross margin for the second quarter.

Selling, general and administrative expenses increased 4.8% to $425.3 million year over year.

Adjusted operating profit totaled $252.2 million, down 9% from the prior-year quarter’s level. The adjusted operating margin in the quarter contracted 130 bps to 15%.

Avantor exited the second quarter of 2025 with cash and cash equivalents of $449.4 million compared with $315.7 million at the first-quarter end. Total debt at the end of the second quarter of 2025 was $4.24 billion compared with $4.11 billion at the first-quarter end.

Cumulative net cash provided by operating activities at the end of the second quarter of 2025 was $263.7 million compared with $422.7 million a year ago.

Avantor has updated its outlook for 2025.

The company now projects its organic revenues to witness growth of negative 1% to flat compared with the prior guidance of negative 1% to positive 1% for the full year.

Management now expects negative low-single-digit growth in the Laboratory Solutions segment compared with the prior guidance of negative low-single-digit to flat. Management also expects Bioscience Production to be flat compared with the prior guidance of up mid-single digits. Management also now expects bioprocessing to be flat to up low single digits, down from up mid-single digits.

The company now expects adjusted EPS to lie in the range of 94 cents to 98 cents compared with the prior guidance of $1.02-$1.10. The Zacks Consensus Estimate is pegged at $1.03.

Avantor exited the second quarter of 2025 with mixed results, wherein earnings missed and revenues surpassed their respective estimates.

Avantor’s management highlighted several strategic initiatives and updates aimed at strengthening the company’s competitive position and long-term growth. A major focus during the quarter was the continued rollout of digital tools to improve customer experience and commercial execution. Notably, the company launched Avantor Navigator, its first AI-powered in-house application designed to help customers discover relevant products and services tailored to their research needs.

Additionally, it is deploying a new digital buying platform that offers a more personalized and seamless experience across web and mobile, backed by unified customer intelligence. A revamped pricing optimization tool was also introduced to provide more agile and market-relevant pricing, helping to drive better conversion rates and reduce cart abandonment. These digital upgrades are already showing traction, with several major contract renewals and wins in the second quarter, including extensions with top-15 global pharma customers and a five-year renewal with BIO Business Solutions, Avantor’s single largest customer channel.

Management also addressed progress on the company’s cost transformation program, which remains on track to deliver $400 million in run-rate savings by the end of 2027.

Per management, on the supply chain front, efforts are underway to optimize delivery performance and improve operational efficiency across both manufacturing and planning. This includes targeted initiatives in the Bioscience Production segment, particularly in bioprocessing, where the team is doubling down on field execution and broadening the product portfolio. Avantor also reiterated its commitment to deleveraging, maintaining net leverage at 3.2x adjusted EBITDA, with a goal to move sustainably below 3x.

AVTR currently carries a Zacks Rank #4 (Sell).

Some better-ranked stocks in the broader medical space that have announced quarterly results are Medpace Holdings, Inc. MEDP, West Pharmaceutical Services, Inc. WST and Boston Scientific Corporation BSX.

Medpace Holdings, sporting a Zacks Rank of 1 (Strong Buy), reported second-quarter 2025 EPS of $3.10, beating the Zacks Consensus Estimate by 3.3%. Revenues of $603.3 million outpaced the consensus mark by 11.5%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Medpace Holdings has a long-term estimated growth rate of 11.4%. MEDP’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 13.9%.

West Pharmaceutical reported second-quarter 2025 adjusted EPS of $1.84, beating the Zacks Consensus Estimate by 21.9%. Revenues of $766.5 million surpassed the Zacks Consensus Estimate by 5.4%. It currently flaunts a Zacks Rank #1.

West Pharmaceutical has a long-term estimated growth rate of 8.5%. WST’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Boston Scientific reported second-quarter 2025 adjusted EPS of 75 cents, beating the Zacks Consensus Estimate by 4.2%. Revenues of $5.06 billion surpassed the Zacks Consensus Estimate by 3.5%. It currently carries a Zacks Rank #2 (Buy).

Boston Scientific has a long-term estimated growth rate of 14%. BSX’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 8.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-09 | |

| Apr-09 | |

| Apr-08 | |

| Apr-07 | |

| Apr-07 | |

| Apr-06 | |

| Apr-03 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 |

Boston Scientific Just Took A 10% Header. Why Analysts Are Still Bullish.

BSX -9.02%

Investor's Business Daily

|

| Mar-30 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite