|

|

|

|

|||||

|

|

|

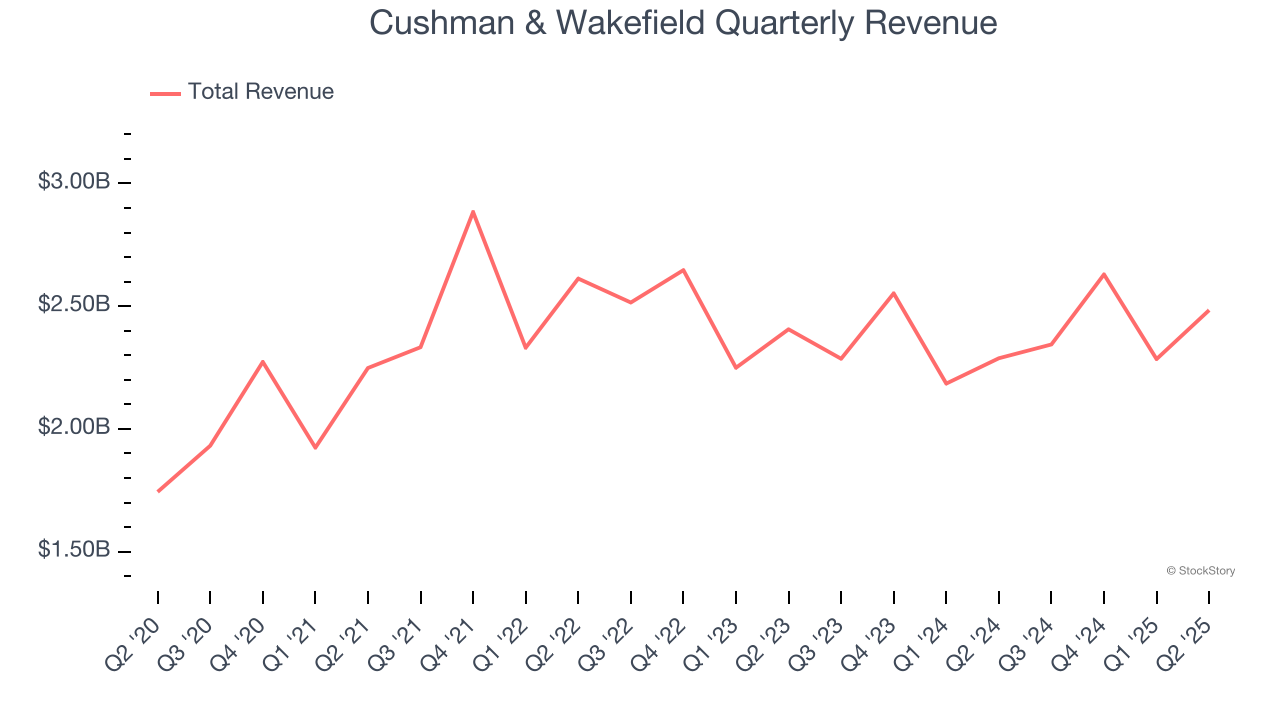

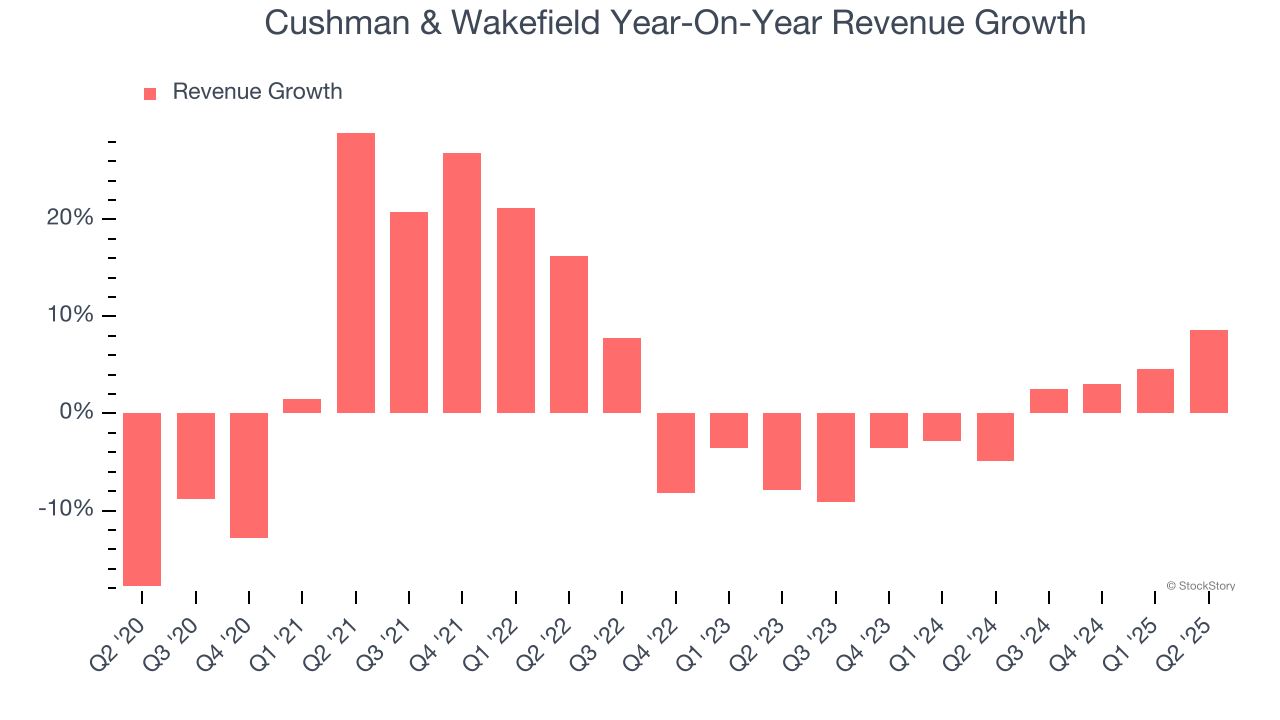

Real estate services firm Cushman & Wakefield (NYSE:CWK) announced better-than-expected revenue in Q2 CY2025, with sales up 8.6% year on year to $2.48 billion. Its non-GAAP profit of $0.30 per share was 36.7% above analysts’ consensus estimates.

Is now the time to buy Cushman & Wakefield? Find out by accessing our full research report, it’s free.

“Our second quarter results highlight the strong and resilient growth engine we have successfully built over the past two years. Capital markets revenue growth of 26% in the quarter underscores our solid market positioning and the early success of our expanded recruiting efforts. Leasing and Services revenue growth continued to exceed expectations as our teams consistently developed and executed compelling market opportunities for our clients. Through the first half of 2025, we achieved 95% adjusted earnings per share growth and are raising our earnings per share outlook for the full year. We also continue to focus on fortifying our balance sheet and this morning have announced an additional $150 million debt paydown,” said Michelle MacKay, Chief Executive Officer of Cushman & Wakefield.

With expertise in the commercial real estate sector, Cushman & Wakefield (NYSE:CWK) is a global Chicago-based real estate firm offering a comprehensive range of services to clients.

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Cushman & Wakefield’s 3.1% annualized revenue growth over the last five years was sluggish. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Cushman & Wakefield’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

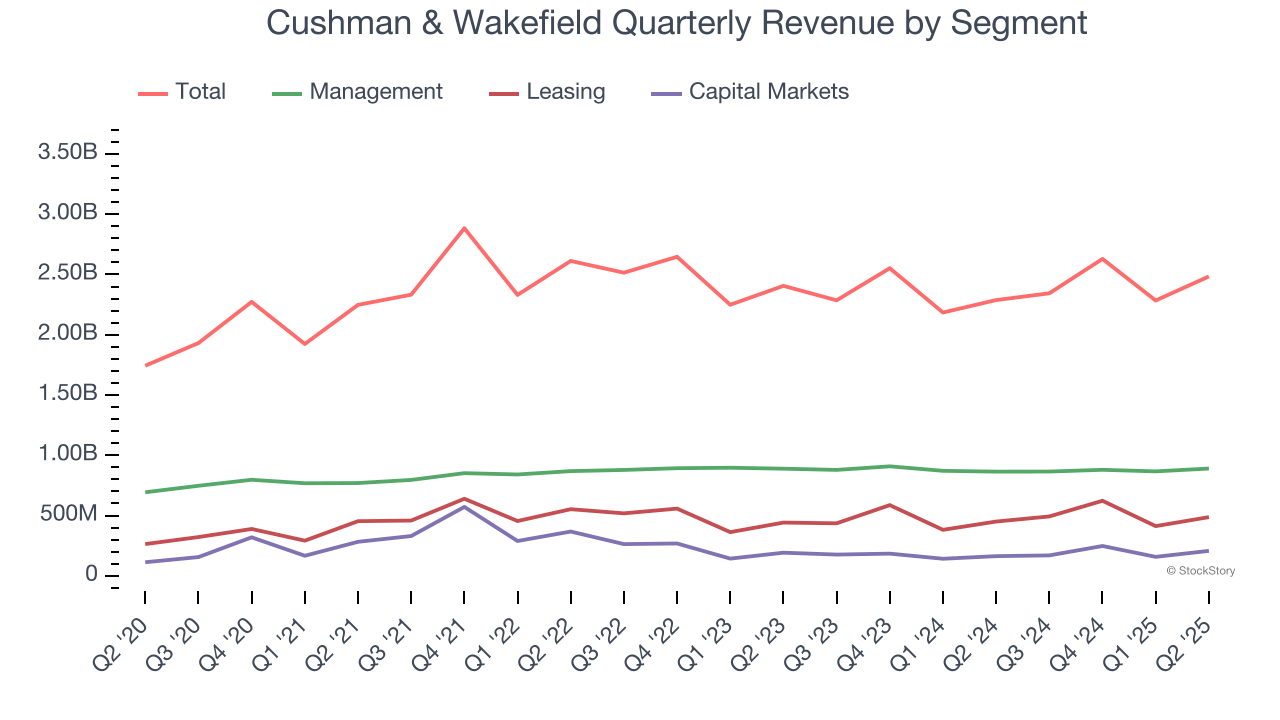

We can better understand the company’s revenue dynamics by analyzing its three most important segments: Management, Leasing, and Capital Markets, which are 35.8%, 19.6%, and 8.3% of revenue. Over the last two years, Cushman & Wakefield’s Management revenue (property management) was flat. However, its Leasing revenue (sourcing tenants) averaged year-on-year growth of 1.4% while its Leasing revenue (sourcing tenants) averaged 1.4% declines.

This quarter, Cushman & Wakefield reported year-on-year revenue growth of 8.6%, and its $2.48 billion of revenue exceeded Wall Street’s estimates by 4.6%.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

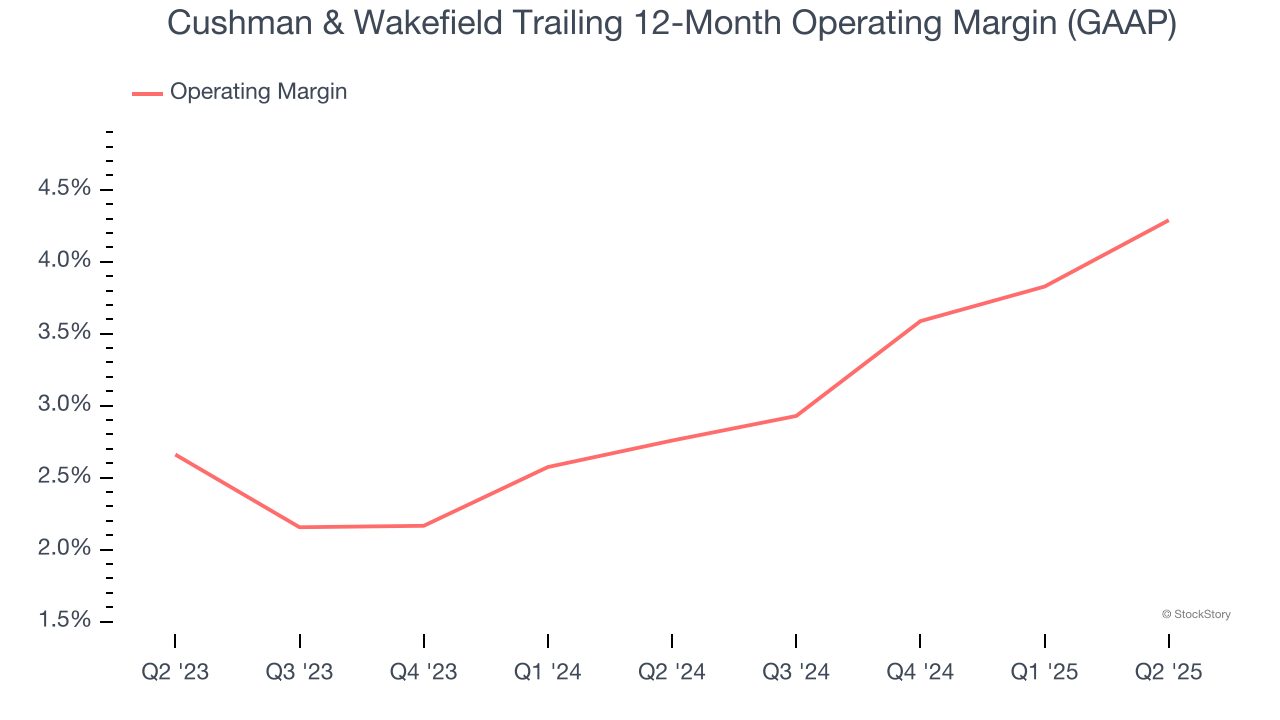

Cushman & Wakefield’s operating margin has been trending up over the last 12 months and averaged 3.5% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

This quarter, Cushman & Wakefield generated an operating margin profit margin of 4.9%, up 1.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

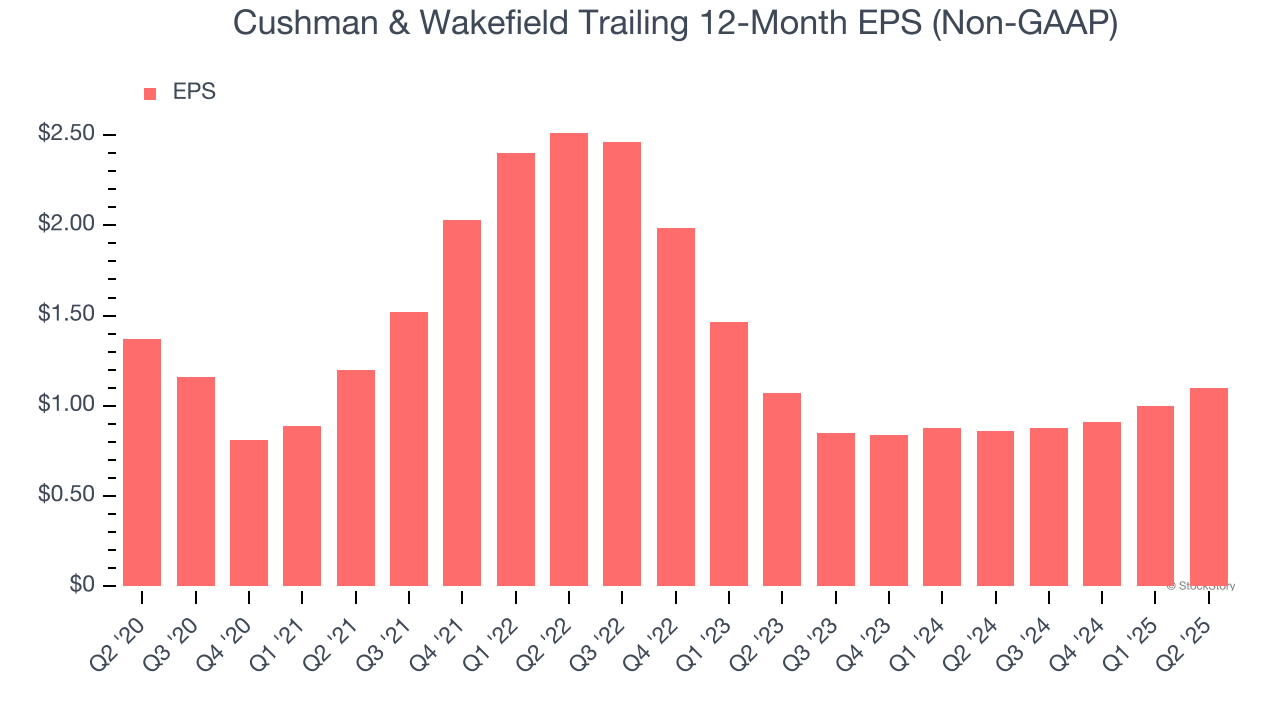

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Cushman & Wakefield, its EPS declined by 4.3% annually over the last five years while its revenue grew by 3.1%. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

In Q2, Cushman & Wakefield reported adjusted EPS at $0.30, up from $0.20 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Cushman & Wakefield’s full-year EPS of $1.10 to grow 8.5%.

We were impressed by how significantly Cushman & Wakefield blew past analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 5% to $12.95 immediately after reporting.

Indeed, Cushman & Wakefield had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-23 | |

| Feb-23 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite