|

|

|

|

|||||

|

|

|

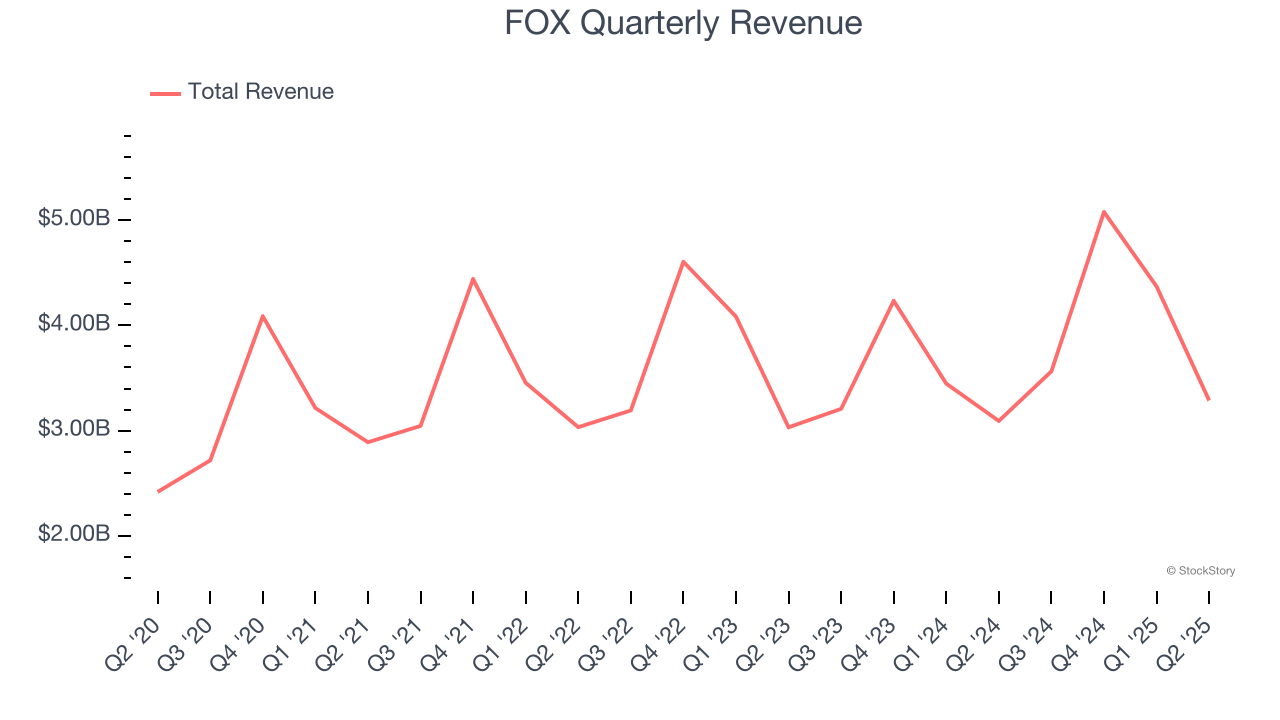

Cable news and media network Fox (NASDAQ:FOXA) announced better-than-expected revenue in Q2 CY2025, with sales up 6.3% year on year to $3.29 billion. Its non-GAAP profit of $1.27 per share was 27.3% above analysts’ consensus estimates.

Is now the time to buy FOX? Find out by accessing our full research report, it’s free.

Founded in 1915, Fox (NASDAQ:FOXA) is a diversified media company, operating prominent cable news, television broadcasting, and digital media platforms.

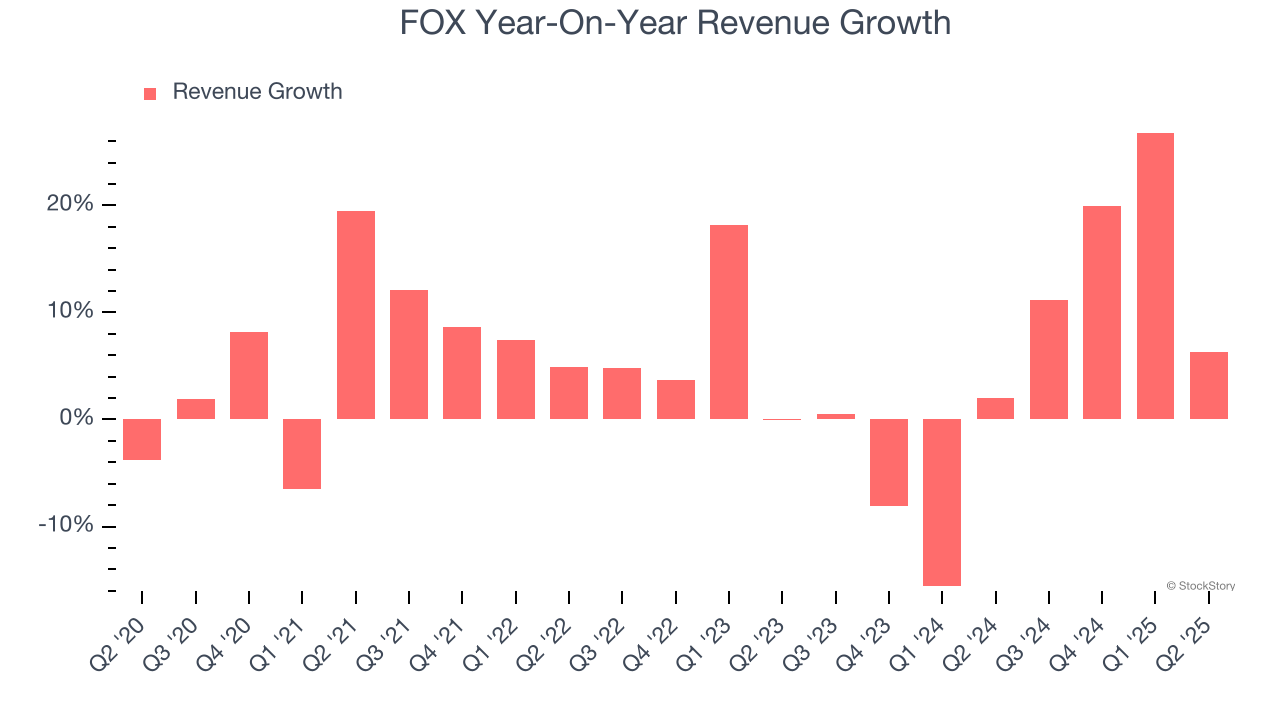

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, FOX’s 5.8% annualized revenue growth over the last five years was sluggish. This was below our standard for the consumer discretionary sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. FOX’s recent performance shows its demand has slowed as its annualized revenue growth of 4.5% over the last two years was below its five-year trend.

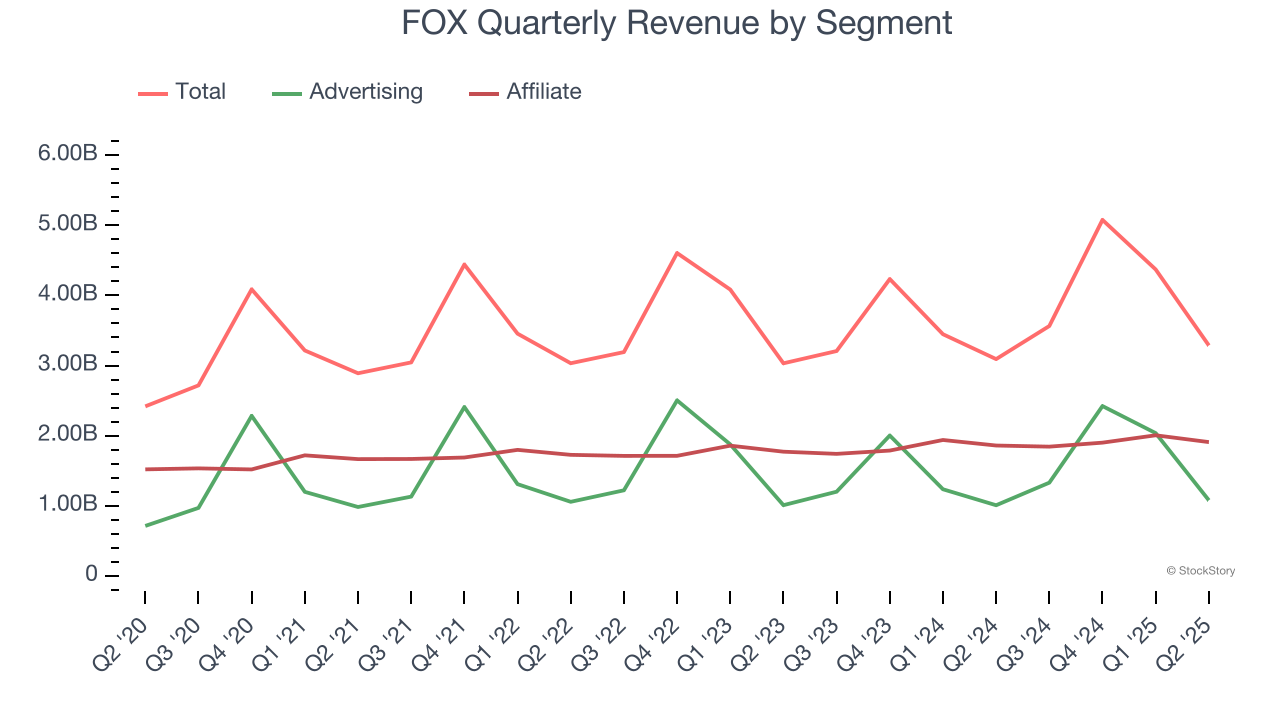

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Advertising and Affiliate, which are 32.8% and 58% of revenue. Over the last two years, FOX’s Advertising revenue (marketing services) averaged 6% year-on-year growth while its Affiliate revenue (licensing and retransmission fees) averaged 4.2% growth.

This quarter, FOX reported year-on-year revenue growth of 6.3%, and its $3.29 billion of revenue exceeded Wall Street’s estimates by 5.5%.

Looking ahead, sell-side analysts expect revenue to decline by 4.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

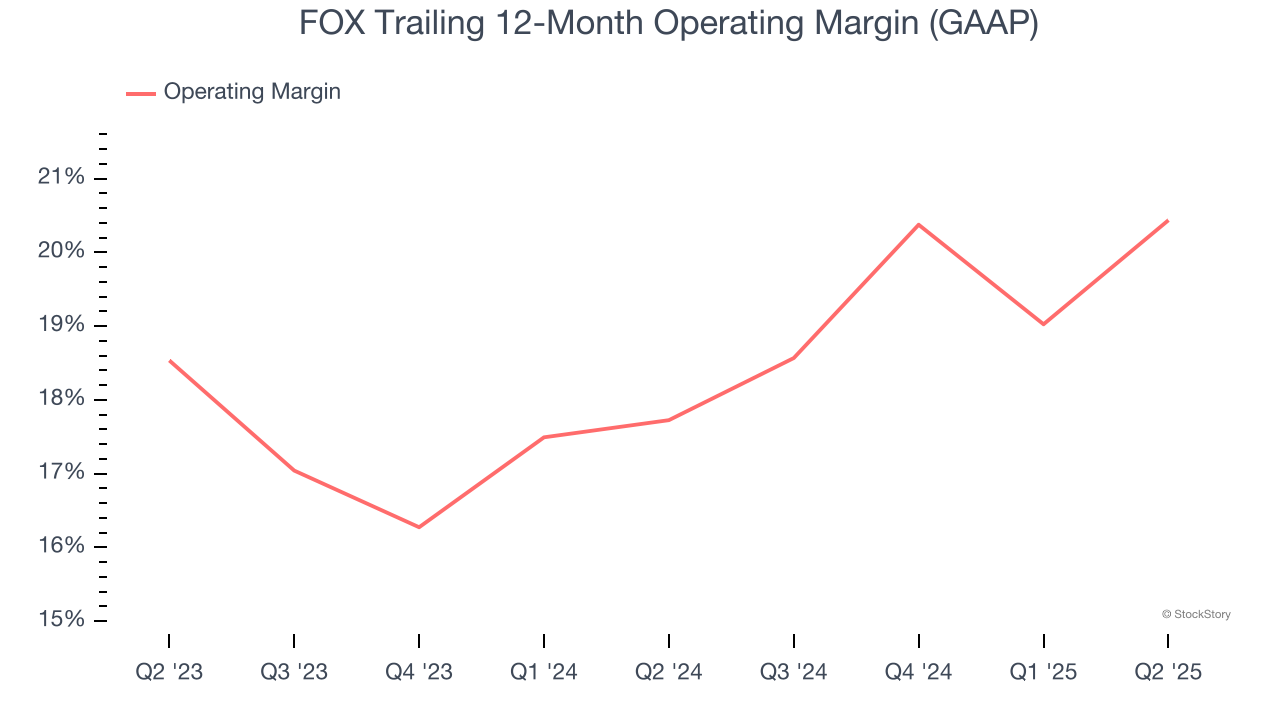

FOX’s operating margin has risen over the last 12 months and averaged 19.2% over the last two years. On top of that, its profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

In Q2, FOX generated an operating margin profit margin of 28.5%, up 6.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

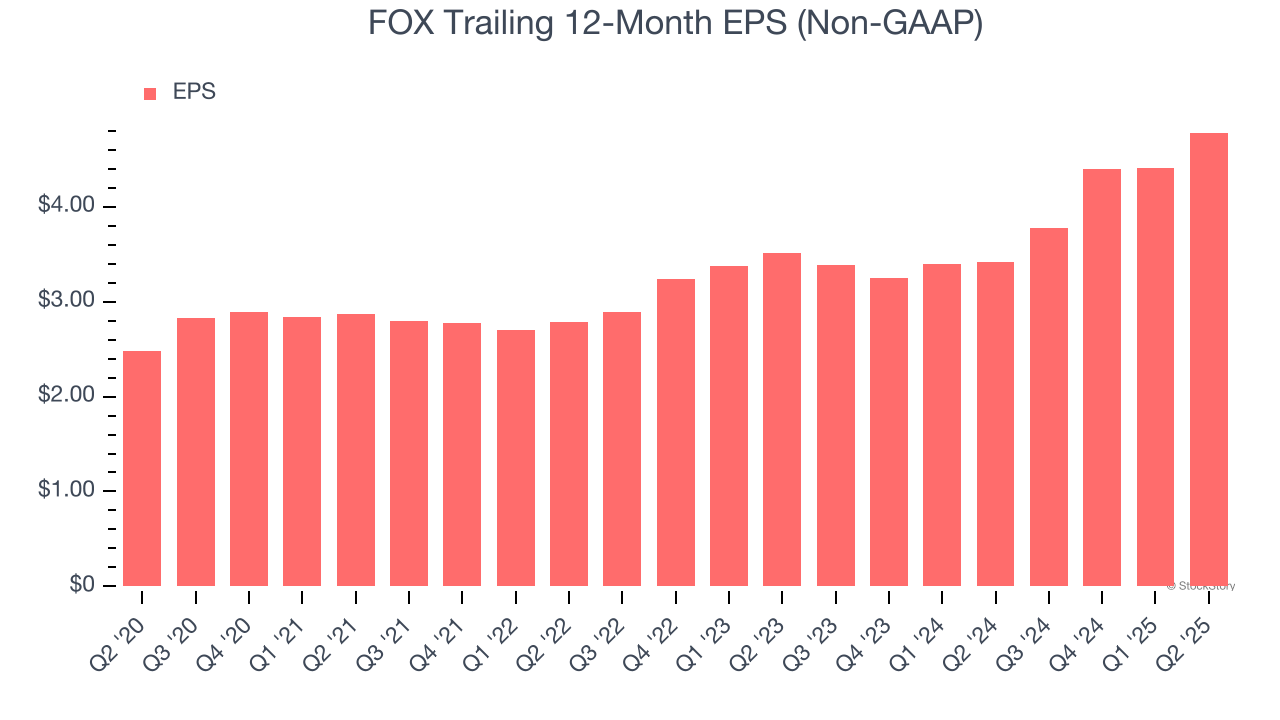

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

FOX’s EPS grew at a solid 14% compounded annual growth rate over the last five years, higher than its 5.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q2, FOX reported adjusted EPS at $1.27, up from $0.90 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects FOX’s full-year EPS of $4.78 to shrink by 10.6%.

We enjoyed seeing FOX beat analysts’ EPS expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 1.8% to $58.06 immediately following the results.

FOX put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Mar-24 | |

| Mar-24 | |

| Mar-19 | |

| Mar-09 | |

| Mar-06 | |

| Mar-02 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-19 | |

| Feb-18 | |

| Feb-13 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite