|

|

|

|

|||||

|

|

|

Rocket Lab USA, Inc. (RKLB) is slated to report second-quarter 2025 results on Aug. 7, 2025, after market close.

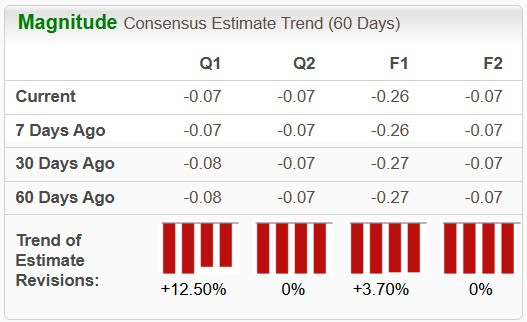

The Zacks Consensus Estimate for revenues is pegged at $135.1 million, indicating an improvement of 27.1% from the year-ago quarter’s reported figure. The consensus mark for the bottom line is pegged at a loss of seven cents per share, implying an improvement from the prior-year quarter’s reported loss of eight cents. The bottom-line estimate has also improved in the past 60 days.

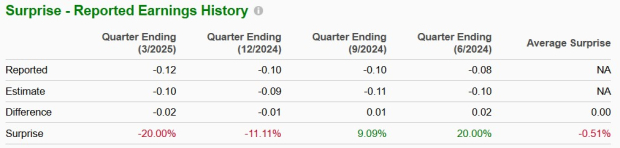

RKLB’s earnings beat the Zacks Consensus Estimate in two of the trailing four quarters and missed in two, the average negative surprise being 0.51%.

Our proven model predicts an earnings beat for RKLB this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Rocket Lab has an Earnings ESP of +18.18% and a Zacks Rank of 3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

RKLB’s Launch Services Unit to Post Solid Sales

Higher revenues generated from growth in the number of launch missions, as well as solid revenue contributions from strong bookings witnessed in the prior quarters, are likely to have bolstered the top line of the Launch Services business segment. HASTE missions performed during the quarter, which come at a higher average selling price compared with standard electron missions, are also likely to have aided this unit’s revenues in the second quarter.

The Zacks Consensus Estimate for the segment’s quarterly revenues is pegged at $39.5 million, indicating a solid 34.5% increase from the top line reported a year ago.

RKLB’s Space Systems Unit Also Holds Potential

Solid growth in spacecraft and satellite manufacturing, along with a strong contribution from RKLB’s control systems and separation systems businesses, is likely to have boosted revenue growth for its Space Systems business segment.

The Zacks Consensus Estimate for the segment’s second-quarter revenues is pegged at $95.4 million, indicating 24.1% growth from the year-ago quarter’s reported figure.

Solid revenue contribution from both of its segments is likely to have bolstered Rocket Lab’s overall revenues in the second quarter.

Such a strong revenue projection is also expected to have boosted RKLB’s second-quarter earnings growth. However, increased operating costs due to higher spending on the Neutron program, a growing workforce, rising research and development expenses and greater IT-related costs, including enhanced cybersecurity requirements for RKLB’s U.S. Government programs, are likely to have weighed on its operating margin. This, in turn, is anticipated to have negatively affected its overall earnings.

RKLB’s shares have exhibited an upward trend, gaining a notable percentage over the past year. Specifically, the stock soared 844.6% in the time frame, outperforming the Zacks aerospace-defense equipment industry’s growth of 55.3%. It has also outpaced the broader Zacks Aerospace sector’s return of 27.2% as well as the S&P 500’s gain of 19.7%.

A similar stellar performance has been delivered by other industry players, such as Kratos Defense & Security Solutions, Inc. (KTOS) and CurtissWright Corporation (CW), whose shares have surged 192.3% and 84.9%, respectively, over the past year.

In terms of valuation, RKLB’s forward 12-month price-to-sales (P/S) is 24.03X, a premium to its industry’s average of 9.61X. This suggests that investors will be paying a higher price than the company's expected sales growth compared with its industry’s P/S ratio.

However, its industry peers are currently trading at a discount compared with RKLB as well as the industry average. While the forward 12-month price/earnings multiple for KTOS is 6.14, the same for CW is 5.19.

According to a World Economic Forum report from April 2024, the space economy may reach $1.8 trillion by 2035, driven by the increasing adoption of satellite and rocket-enabled technologies. This outlook strengthens the long-run growth prospects of space stocks like RKLB. Notably, RKLB’s Electron launch vehicle ranks as the second most frequently launched orbital rocket by U.S. companies.

However, RKLB is currently facing a few challenges that investors should keep in mind before considering the stock. One key concern is the company’s high operating expenses, driven by continuous investments in developing new products and improving existing ones. These elevated costs tend to offset the advantages of strong revenue growth, leading to quarterly losses.

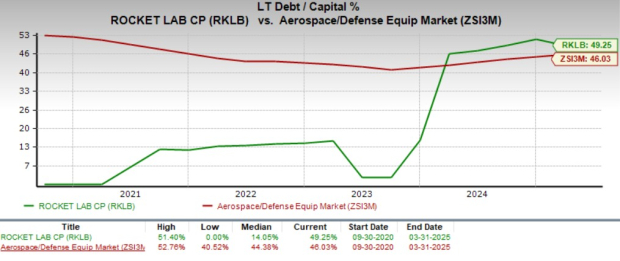

Another point of concern is the company’s high level of debt compared with its industry peers, as evident from RKLB’s higher long-term debt-to-capital ratio compared with the industry. This is primarily due to significant investments in designing, manufacturing and commercializing new technologies. Such a heavy debt load could raise concerns among investors.

RKLB is less likely to disappoint with its second-quarter 2025 results, taking into account its favorable Zacks Rank, solid revenue growth expectations and positive Earnings ESP. However, considering its premium valuation and elevated leverage compared with its industry, investors interested in RKLB should remain on the sidelines before this Thursday.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 min | |

| 21 min | |

| 24 min | |

| 30 min | |

| 32 min | |

| 34 min | |

| 1 hour |

Rocket Lab Reports Earnings Tonight: What Do Prediction Markets Say About Neutron Launches in 2026?

RKLB

Benzinga Prediction Markets

|

| 2 hours | |

| 2 hours | |

| 5 hours | |

| 5 hours |

SpaceX Rivals Rocket Lab, AST SpaceMobile About To Report Earnings. What To Expect.

RKLB

Investor's Business Daily

|

| 8 hours | |

| 12 hours | |

| Aug-09 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite