|

|

|

|

|||||

|

|

|

Kratos Defense & Security Solutions, Inc. (KTOS) is set to release second-quarter 2025 results on Aug. 7, 2025, after market close.

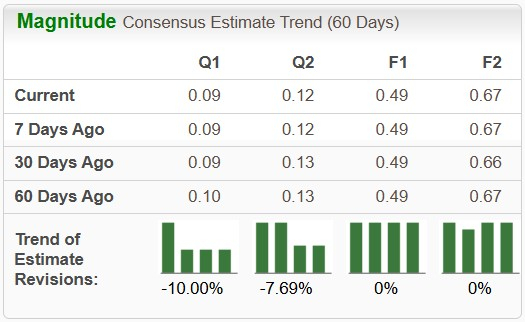

The Zacks Consensus Estimate for KTOS’ second-quarter revenues is pegged at $306.8 million, which indicates a 2.2% rise from the year-ago quarter’s level. The consensus estimate for second-quarter earnings is pegged at nine cents per share, which indicates a decline of 35.7% from the prior-year reported figure. The bottom-line estimate has also moved south over the past 60 days.

KTOS has an impressive earnings surprise history. Its earnings outpaced the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 47.57%.

Our proven model predicts an earnings beat for Kratos Defense this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

KTOS currently has an Earnings ESP of +5.56% and a Zacks Rank of 3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Projections From KTOS’ Business Segments

Persistent supply-chain disruptions and raw material unavailability in the aerospace-defense industry, resulting in delayed production and delivery schedules for drones, are likely to have impacted the revenues of the Unmanned Systems segment in the second quarter.

The Zacks Consensus Estimate for the segment’s quarterly revenues is pegged at $79.1 million, indicating a 7.8% decline from the figure reported a year ago.

Solid revenue growth from the company’s C5ISR, Defense Rocket Support and microwave electronics products businesses, as well as turbine technologies and space, satellite and cyber business, is expected to have bolstered the top line of the Kratos Government Solutions business segment.

The Zacks Consensus Estimate for the Government segment’s second-quarter revenues is pegged at $228.7 million, indicating a 6.7% rise from the year-ago quarter’s reported figure.

With one of Kratos Defense’s segments expected to report solid top-line growth, its overall revenue outlook remains positive. Moreover, positive synergies from the acquisition of certain assets of Norden Millimeter, Inc. in the first quarter are likely to contribute favorably to Kratos Defense’s second-quarter operating results.

Such a solid top-line projection is likely to have aided KTOS’ second-quarter bottom line. However, expected downtime at its high-margin Microwave Products facility in Israel, along with higher material and subcontractor costs on certain multi-year fixed price contracts in the Unmanned Systems business, is expected to have negatively impacted the company’s overall earnings.

Kratos Defense’s shares have exhibited an upward trend, gaining a notable percentage over the past year. Specifically, the stock has gained 193.8%, outperforming the Zacks aerospace-defense Equipment industry’s growth of 58.1%.

Other notable stocks from the same industry have also rallied in the past year and comfortably outpaced the industry’s performance. Shares of Rocket Lab USA Inc. (RKLB) and CurtissWright Corporation (CW) have risen 855.8% and 87.2%, respectively, in the past year.

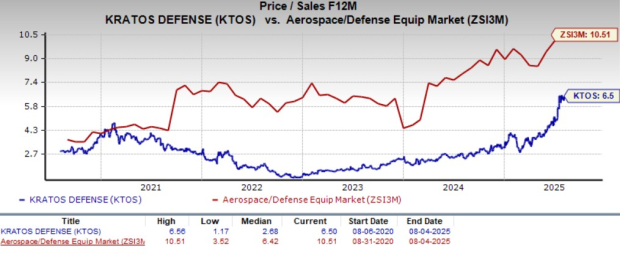

From a valuation perspective, KTOS is trading at a discount when compared with its industry. Currently, it is trading at 6.50X forward 12-month sales multiple, which is lower than its industry’s forward price/sales multiple of 10.51X. However, its five-year median is 2.68X. So, the company’s valuation looks stretched when compared with its five-year range.

While the forward 12-month price/sales multiple for RKLB is 27.65X, the same for CW is 5.32X.

Rising global tensions have led many countries to significantly boost their defense capabilities. This trend has benefited defense companies like Kratos Defense, Rocket Labs and CurtissWright through strong contract wins. As a result, Kratos Defense's second-quarter 2025 results are likely to show solid growth in its order backlog.

However, persistent margin pressures due to rising material and subcontractor costs remain a key concern for investors.

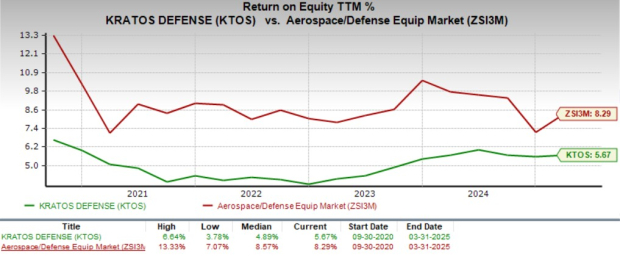

This might have also led the company to have a lower return-on-equity (ROE) compared with its peer group. The figure below implies KTOS is less efficient at creating profits and increasing shareholder value than its peer group. Currently, KTOS’ ROE is pinned at 5.67% compared with the industry’s 8.29%.

Kratos Defense may deliver an earnings beat this quarter, supported by its positive Earnings ESP. The company is poised to benefit from robust defense spending trends and strategic acquisitions. However, considering the near-term challenges such as downtime at its high-margin Microwave Products facility along with lower ROE, investors interested in this stock should wait for a better entry point before this Thursday.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 10 min | |

| 22 min | |

| 25 min | |

| 31 min | |

| 33 min | |

| 35 min | |

| 1 hour |

Rocket Lab Reports Earnings Tonight: What Do Prediction Markets Say About Neutron Launches in 2026?

RKLB

Benzinga Prediction Markets

|

| 2 hours | |

| 2 hours | |

| 5 hours | |

| 5 hours |

SpaceX Rivals Rocket Lab, AST SpaceMobile About To Report Earnings. What To Expect.

RKLB

Investor's Business Daily

|

| 8 hours | |

| 12 hours | |

| Aug-09 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite