|

|

|

|

|||||

|

|

|

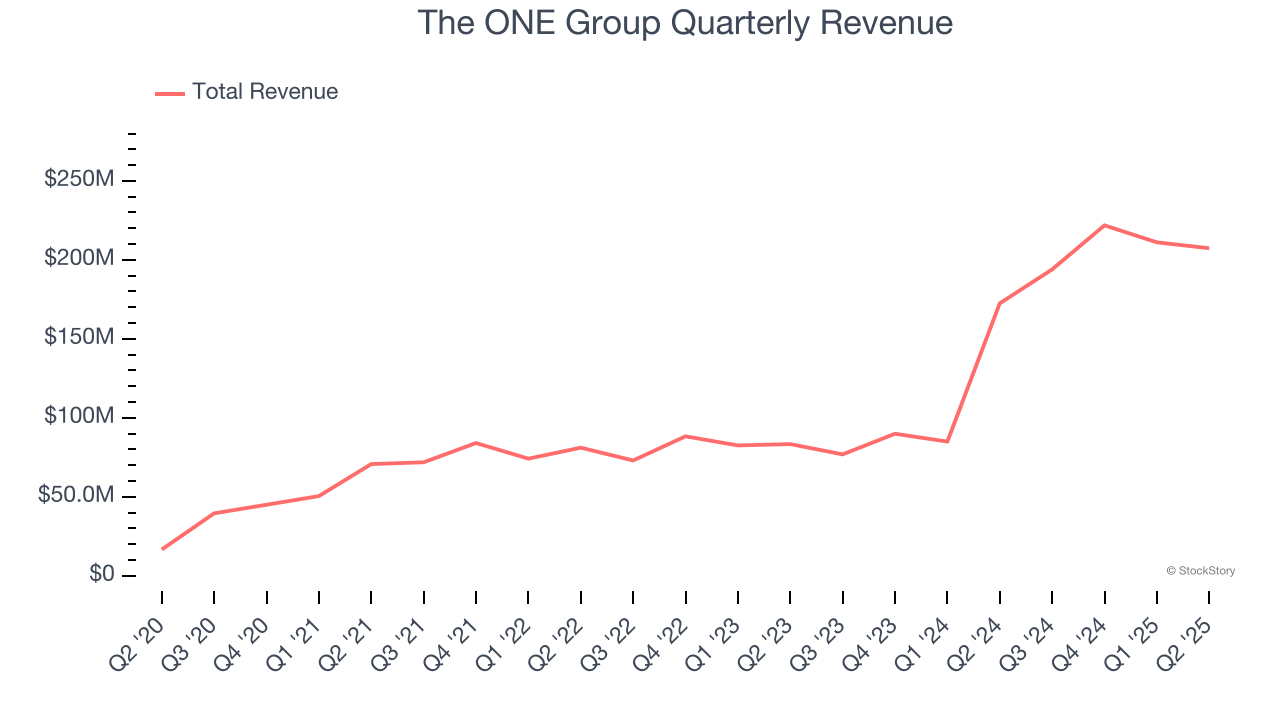

Upscale restaurant company The One Group Hospitality (NASDAQ:STKS) missed Wall Street’s revenue expectations in Q2 CY2025, but sales rose 20.2% year on year to $207.4 million. Next quarter’s revenue guidance of $192.5 million underwhelmed, coming in 5.7% below analysts’ estimates. Its non-GAAP profit of $0.05 per share was significantly above analysts’ consensus estimates.

Is now the time to buy The ONE Group? Find out by accessing our full research report, it’s free.

Doubling as a hospitality services provider for hotels and resorts, The One Group Hospitality (NASDAQ:STKS) is an upscale restaurant company that operates STK Steakhouse and Kona Grill.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $834.4 million in revenue over the past 12 months, The ONE Group is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can grow faster because it has more white space to build new restaurants.

As you can see below, The ONE Group’s sales grew at an incredible 44.4% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new restaurants and expanded its reach.

This quarter, The ONE Group generated an excellent 20.2% year-on-year revenue growth rate, but its $207.4 million of revenue fell short of Wall Street’s high expectations. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months, a deceleration versus the last six years. This projection doesn't excite us and suggests its menu offerings will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

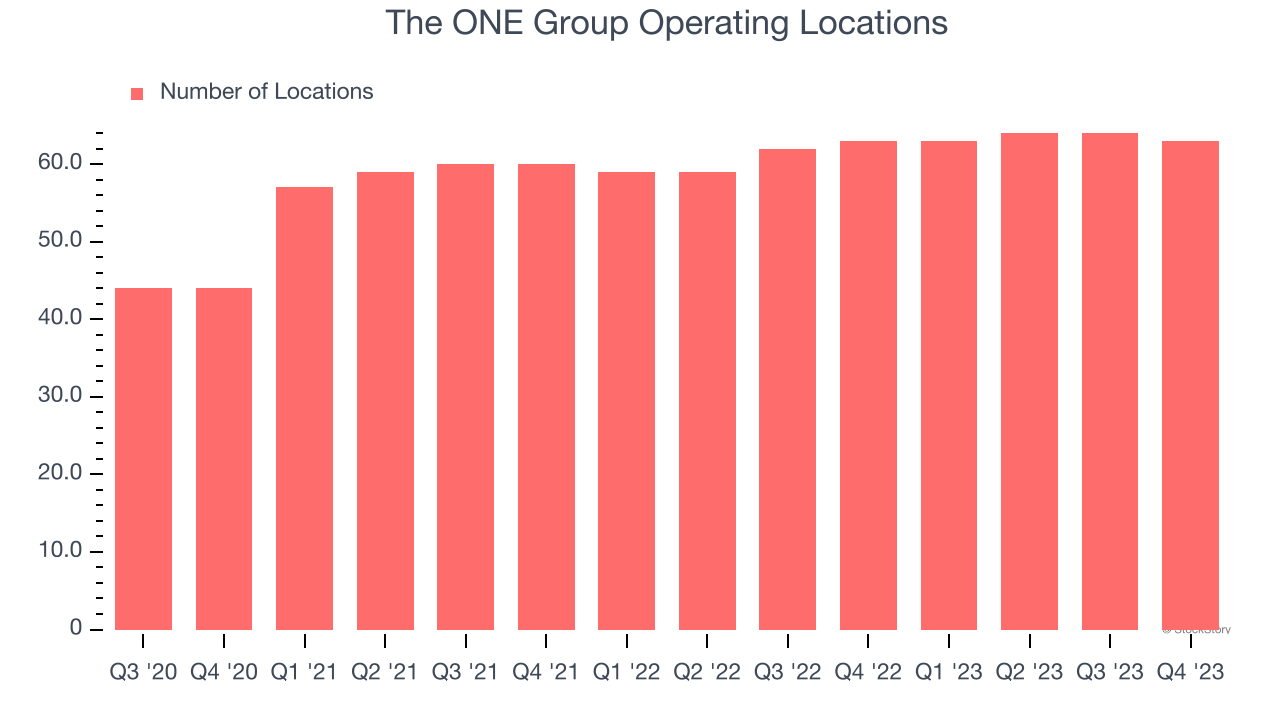

A restaurant chain’s total number of dining locations often determines how much revenue it can generate.

The ONE Group opened new restaurants quickly over the last two years, averaging 1.6% annual growth, faster than the broader restaurant sector.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Note that The ONE Group reports its restaurant count intermittently, so some data points are missing in the chart below.

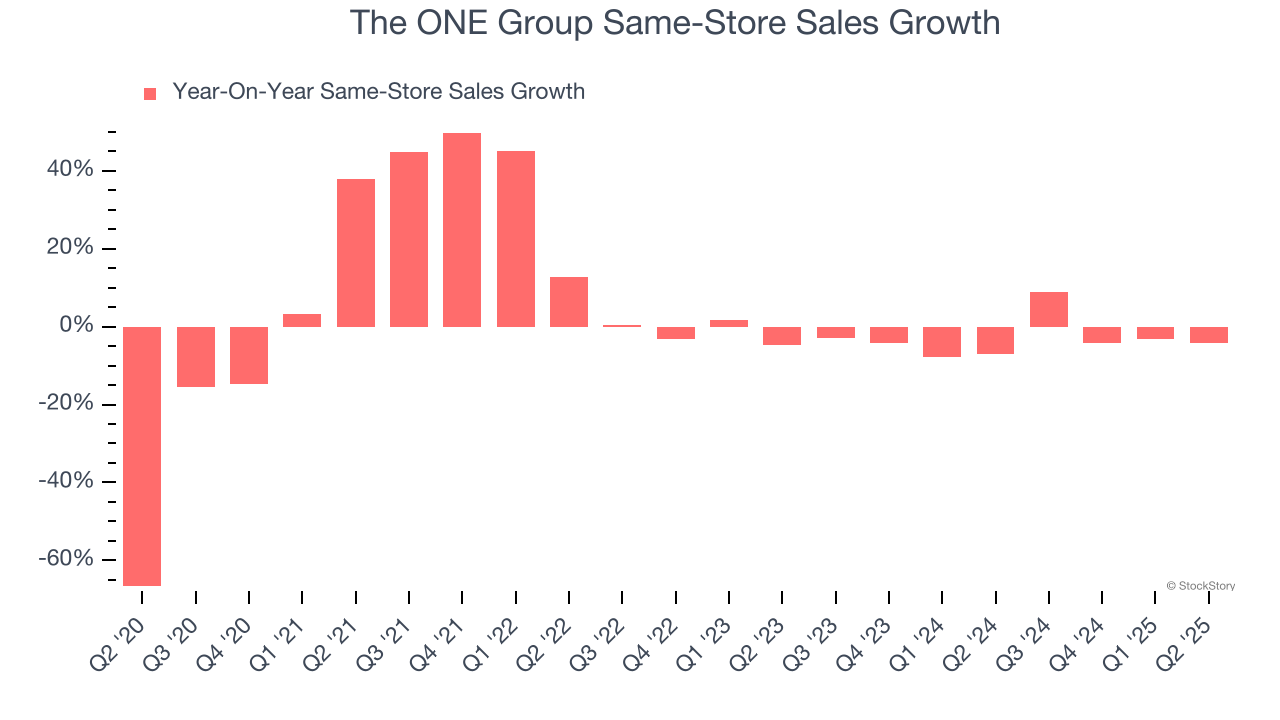

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

The ONE Group’s demand has been shrinking over the last two years as its same-store sales have averaged 3.1% annual declines. This performance is concerning - it shows The ONE Group artificially boosts its revenue by building new restaurants. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its restaurant base.

In the latest quarter, The ONE Group’s same-store sales fell by 4.1% year on year. This performance was more or less in line with its historical levels.

We were impressed by how significantly The ONE Group blew past analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock remained flat at $3.05 immediately after reporting.

Is The ONE Group an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Jun-03 | |

| May-28 | |

| May-11 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-01 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-13 | |

| Mar-13 | |

| Mar-12 | |

| Feb-25 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite