|

|

|

|

|||||

|

|

|

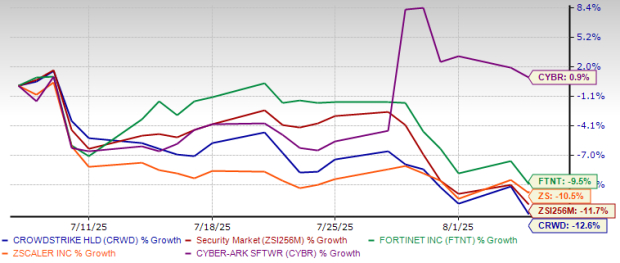

CrowdStrike Holdings CRWD stock has been in a downward trajectory over the past month. Shares of the company have plunged 12.6% over the past month, underperforming the Zacks Security industry’s decline of 11.7%.

CrowdStrike has also underperformed industry peers, including CyberArk Software CYBR, Fortinet FTNT and Zscaler ZS. Shares of CyberArk have inched up 0.9%, while Fortinet and Zscaler have declined 9.5% and 10.5%, respectively.

This underperformance raises the question: Should investors cut their losses and exit, or is it worth holding CRWD stock?

CRWD’s lofty valuation make it vulnerable to further correction.

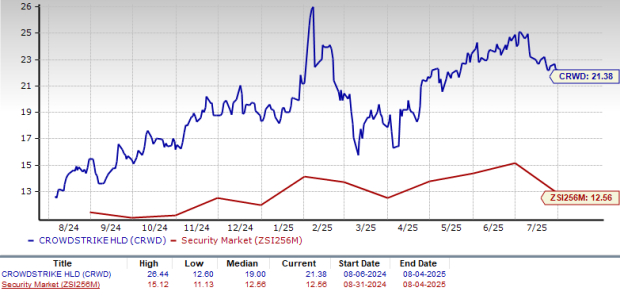

CrowdStrike is currently trading at a high price-to-sales (P/S) multiple, far above the Zacks Security industry. CrowdStrike’s forward 12-month P/S ratio sits at 21.38X, significantly higher than the Zacks Security industry’s forward 12-month P/S ratio of 12.56X.

The stock’s premium valuation when compared with its industry peers, including CyberArk, Fortinet and Zscaler, warrants further caution. At present, CyberArk, Fortinet and Zscaler have P/S multiples of 13.75X, 18.10X and 13.74X, respectively.

CrowdStrike stock has also remained highly volatile due to several macroeconomic and business-related factors. Additionally, the company’s slowing sales growth and profitability compression do not justify its lofty valuations.

Although CrowdStrike has experienced impressive growth since its IPO, recent quarterly reports have shown a deceleration in its growth rate. The company's revenue growth, while still robust, is not as explosive as in previous years.

CrowdStrike had enjoyed more than 35% year-over-year top-line growth till fiscal 2024. However, the growth rate decelerated in fiscal 2025 to 29%. The current Zacks Consensus Estimate for fiscal 2026 and 2027 suggests that the top-line growth will further decelerate to around 21%.

To survive in the highly competitive cybersecurity market, each player is continuously investing to broaden their capabilities. Investment in research & development (R&D) is a top priority for CrowdStrike. Over the last six fiscals, CrowdStrike’s R&D expenses increased 12-fold to improve the design, architecture, operation and quality of its cloud platform.

Over the past few years, CrowdStrike has invested heavily to enhance its sales and marketing (S&M) capabilities, particularly by increasing the sales force. As a result, CrowdStrike’s S&M expenses increased nearly ninefold to $1.52 billion in fiscal 2025 from $173 million in fiscal 2019.

In the first quarter of fiscal 2026, S&M and R&D expenses soared 25.5% and 34.7%, respectively, year over year. Though the firm foresees these investments to generate benefits over the long run, higher expenses are weighing on the company’s bottom-line results.

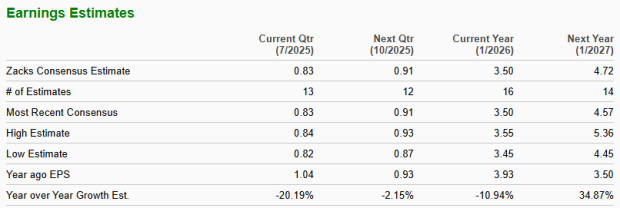

First-quarter non-GAAP earnings declined 7.6% year over year to 73 cents per share. Increasing costs are likely to continue impacting CrowdStrike’s bottom-line performance in the near term, as reflected in the Zacks Consensus Estimate.

CrowdStrike’s decelerating sales growth, shrinking profits and premium valuation warrant a cautious approach to the stock, which makes this Zacks Rank #4 (Sell) stock less attractive in the near term.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite