|

|

|

|

|||||

|

|

|

The Home Depot, Inc. HD, a prominent player in the home improvement retail sector, continues to benefit from its strategic store investments, supply-chain discipline and expanding digital capabilities. Its ability to adapt to shifting consumer behavior and macroeconomic headwinds has helped it maintain a solid position in a competitive market. However, with the stock already pricing in much of this resilience, investors are wondering: Is there still value to unlock, or is it prudent to hold the stock, or consider trimming positions at the current price?

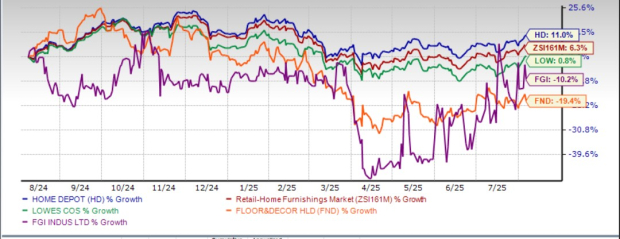

Shares of Home Depot closed at $386.80 yesterday, delivering a gain of 11% over the past year. This performance outpaced the industry’s 6.3% growth. Home Depot has also outperformed peers such as Lowe's Companies, Inc. LOW, Floor & Decor Holdings, Inc. FND and FGI Industries Ltd. FGI. While shares of Lowe’s have risen 0.8% in the past year, Floor & Decor Holdings and FGI Industries have declined 19.4% and 10.2%, respectively.

Home Depot currently trades at a forward 12-month price-to-sales (P/S) multiple of 2.29, which positions it at a premium compared to the industry’s average of 1.61. However, the stock is trading slightly below its median P/S level of 2.30, observed over the past year.

This premium positioning is especially notable when compared to peers like Lowe’s (with a forward 12-month P/S ratio of 1.55), Floor & Decor (1.71) and FGI Industries (0.06).

Home Depot stands out as a compelling long-term investment opportunity for those seeking exposure to a stable company in the home improvement sector. In a landscape filled with economic noise and macroeconomic uncertainty, Home Depot continues to demonstrate resilience through strategic actions and its ability to serve both DIY customers and professional contractors.

One of the most promising aspects of Home Depot’s growth story is its Pro segment. The company has been expanding its professional customer base with acquisitions like SRS Distribution. This move not only brings complementary verticals such as roofing, landscaping and pool supply under its umbrella but also significantly strengthens Home Depot’s trade credit program, an essential tool for winning and retaining large-scale Pro clients. Management believes SRS will be a growth engine, capturing more share from fragmented Pro markets.

Home Depot’s investment in technology and customer-facing innovation continues to deliver results. Its interconnected retail model, a seamless blend of digital and in-store shopping, is proving highly effective. Enhancements in delivery speed, combined with AI-driven support tools like Magic Apron, are elevating the customer experience and encouraging higher engagement. By combining AI advancements with ongoing employee training, Home Depot is repositioning its stores as intelligent service centers.

At a strategic level, the company’s approach to supply chain management reinforces its investment appeal. By reducing overdependence on any single country for sourcing and ensuring more than half of its purchases are made in the United States, Home Depot is safeguarding against geopolitical risks and potential tariff pressures. Add to this the structural tailwinds from an aging U.S. housing stock and high home equity levels, which put Home Depot in a better position to benefit from a wave of deferred remodeling demand once interest rates normalize. Together, these factors provide a strong case for investors to consider Home Depot as a core holding in their portfolios.

While Home Depot remains a strong operator, there are still reasons for caution. The company is facing pressure on its margins as rising costs weigh on profitability, even as sales grow. Demand for big-ticket, discretionary purchases like kitchen and bath remodels remains soft, with many homeowners holding off on major remodels due to high interest rates. Inventory levels have also climbed, raising questions about efficiency if demand further slows.

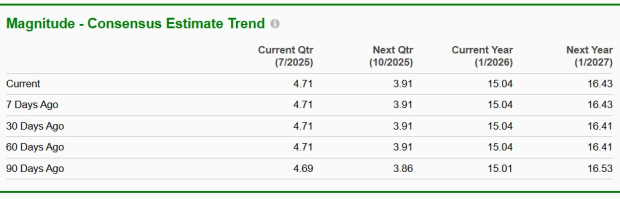

Over the past 30 days, the Zacks Consensus Estimate for Home Depot’s current fiscal year has held steady at $15.04, implying a year-over-year decline of 1.3%. Meanwhile, the estimate for the next fiscal year has risen by a couple of cents to $16.43, suggesting year-over-year growth of 9.2%.

Considering Home Depot’s ongoing investments in Pro expansion, digital innovation and supply-chain resilience, the company remains fundamentally sound. However, near-term challenges such as margin pressure, soft discretionary demand and limited earnings growth suggest that much of the good news may already be reflected in the stock’s current valuation. For existing shareholders, it makes sense to hold and stay invested, given Home Depot’s long-term potential and market leadership. For prospective investors, it may be prudent to wait for a more attractive entry point or clearer signs of an earnings inflection before initiating a new position. Home Depot currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite