|

|

|

|

|||||

|

|

|

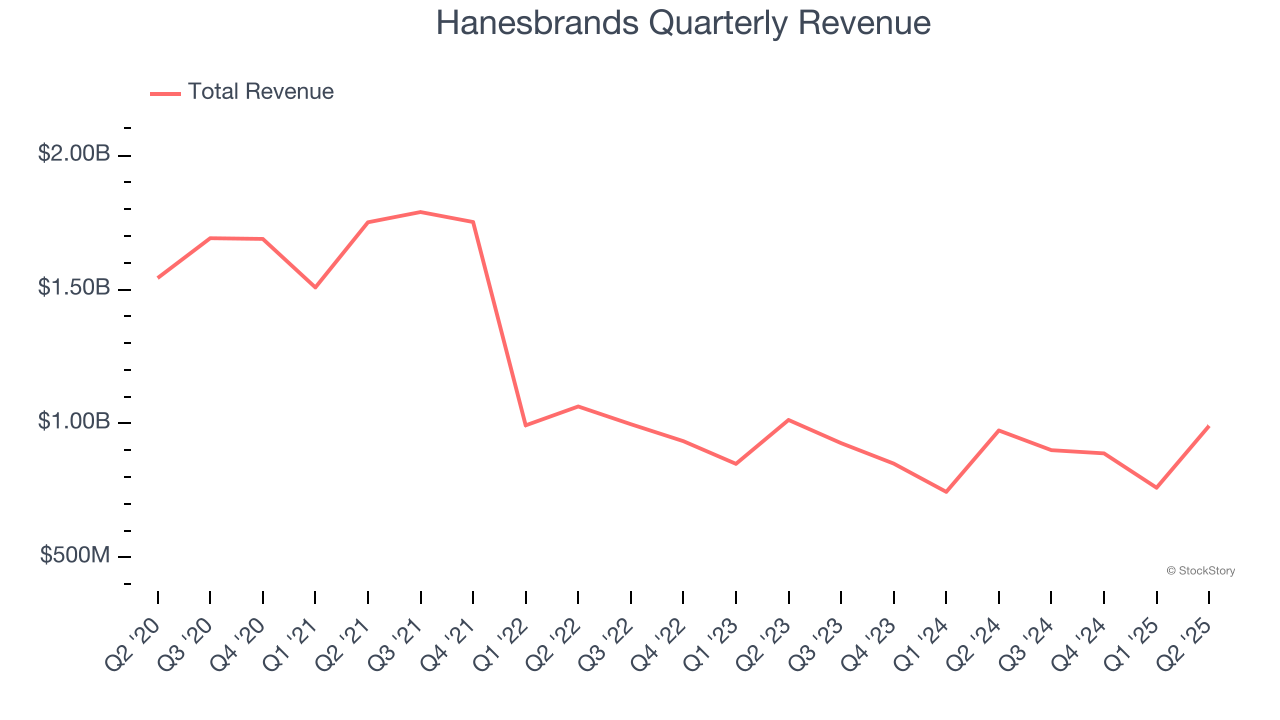

Clothing company Hanesbrands (NYSE:HBI) announced better-than-expected revenue in Q2 CY2025, with sales up 1.8% year on year to $991.3 million. The company expects next quarter’s revenue to be around $900 million, close to analysts’ estimates. Its non-GAAP profit of $0.24 per share was 34.8% above analysts’ consensus estimates.

Is now the time to buy Hanesbrands? Find out by accessing our full research report, it’s free.

“For the third consecutive quarter, we delivered revenue, profit and earnings per share growth that exceeded our expectations as we continue to see the benefits of our growth strategy and prior transformation initiatives,” said Steve Bratspies, CEO.

A classic American staple founded in 1901, Hanesbrands (NYSE: HBI) is a clothing company known for its array of basic apparel including innerwear and activewear.

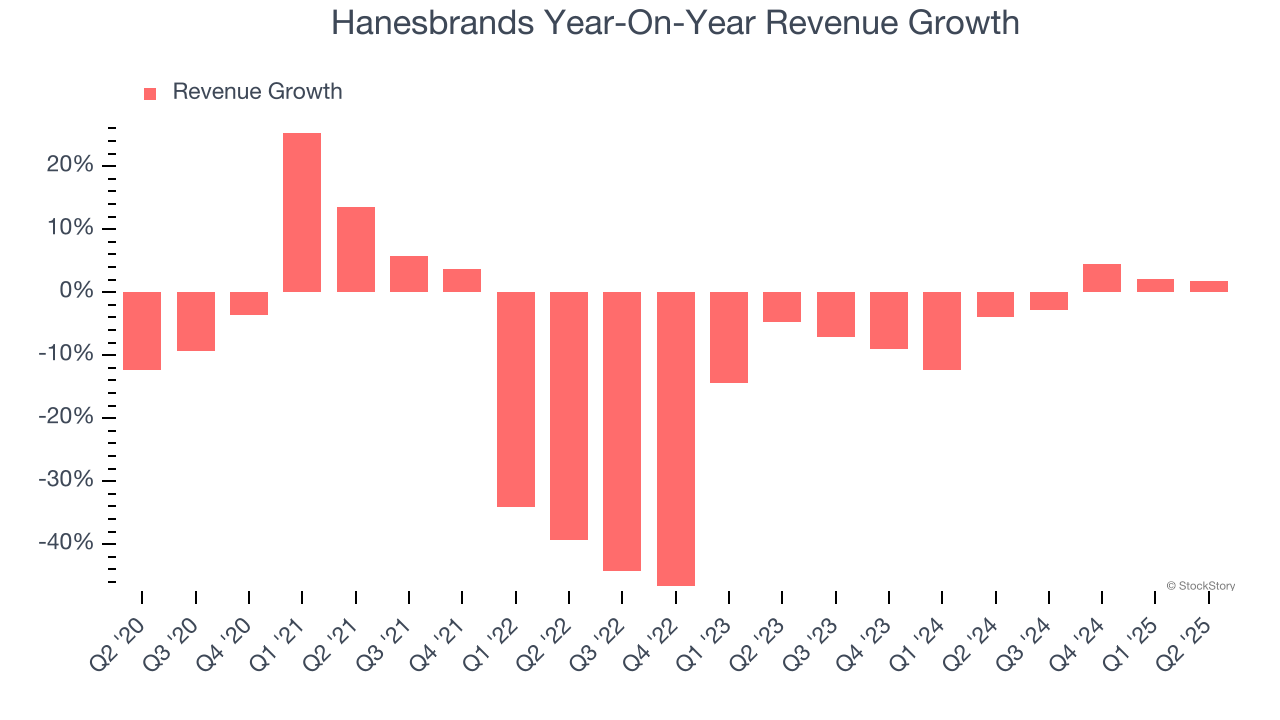

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Hanesbrands’s demand was weak over the last five years as its sales fell at a 11.1% annual rate. This wasn’t a great result and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Hanesbrands’s annualized revenue declines of 3.4% over the last two years suggest its demand continued shrinking.

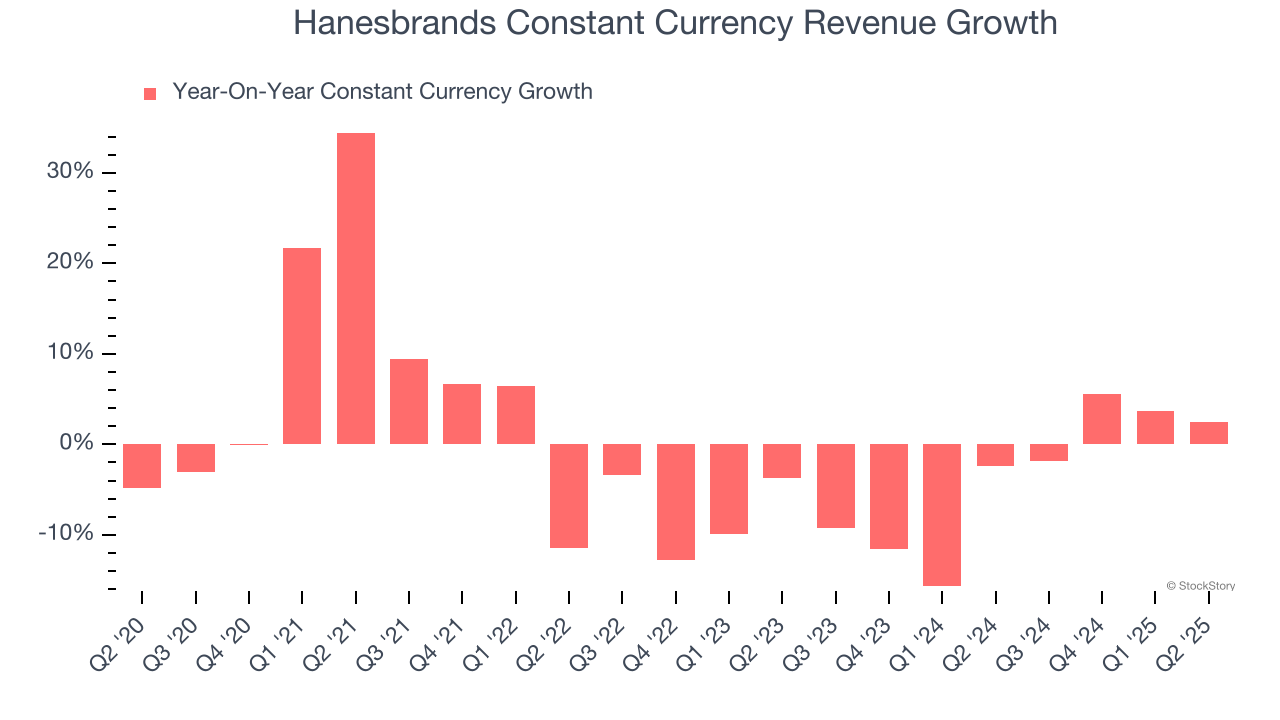

Hanesbrands also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 3.6% year-on-year declines. Because this number aligns with its normal revenue growth, we can see that Hanesbrands has properly hedged its foreign currency exposure.

This quarter, Hanesbrands reported modest year-on-year revenue growth of 1.8% but beat Wall Street’s estimates by 1.9%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 2.1% over the next 12 months, similar to its two-year rate. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

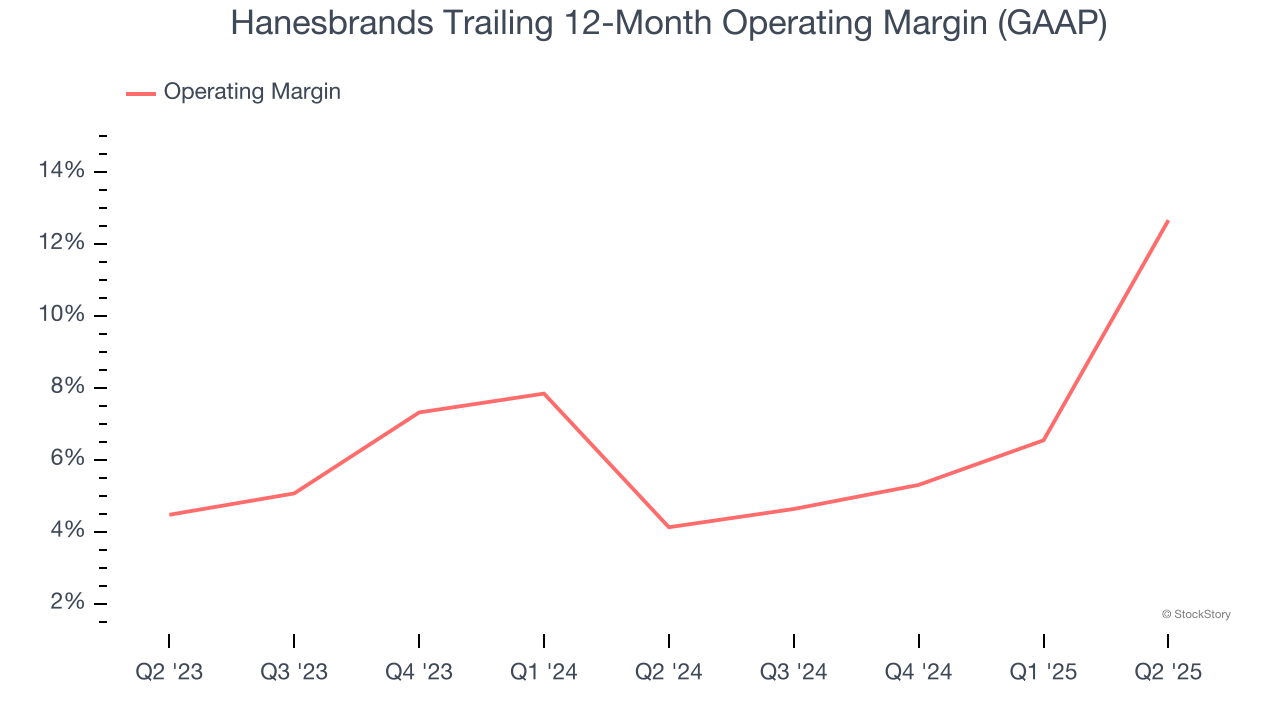

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Hanesbrands’s operating margin has risen over the last 12 months and averaged 8.4% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports mediocre profitability for a consumer discretionary business.

This quarter, Hanesbrands generated an operating margin profit margin of 15.6%, up 22.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

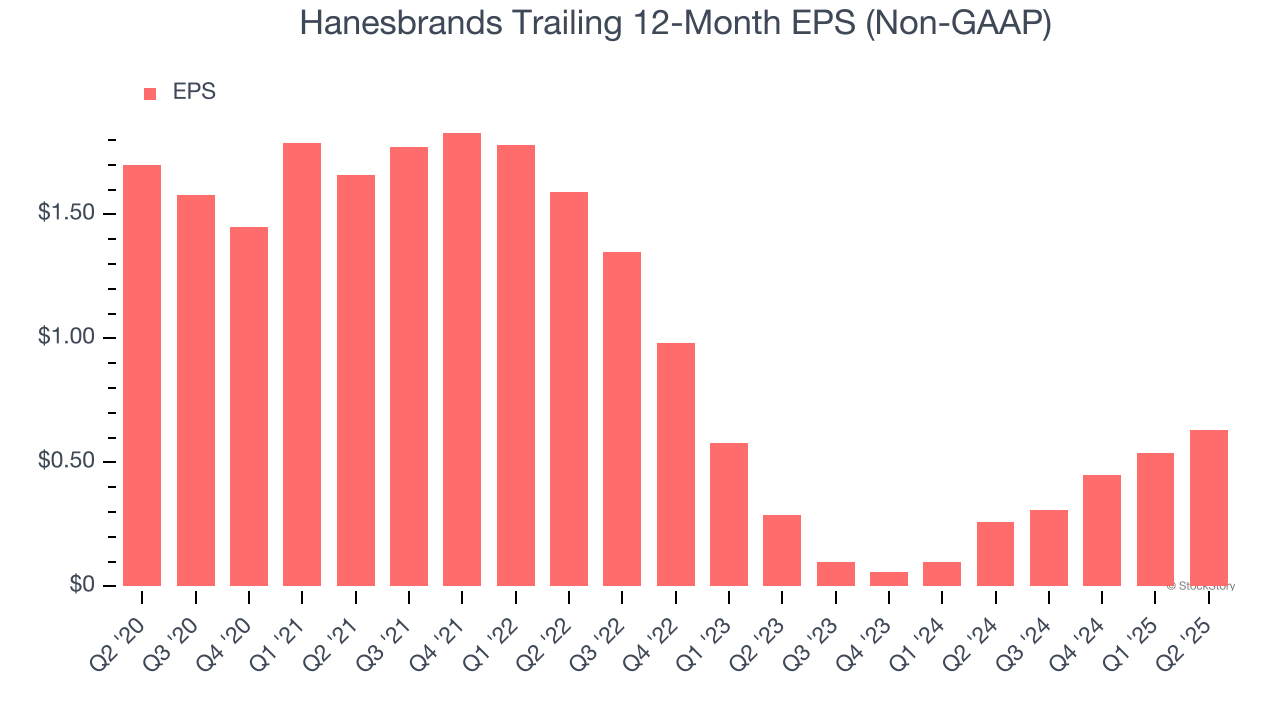

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Hanesbrands, its EPS declined by 18% annually over the last five years, more than its revenue. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

In Q2, Hanesbrands reported adjusted EPS at $0.24, up from $0.15 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Hanesbrands’s full-year EPS of $0.63 to shrink by 14.9%.

We were impressed by how significantly Hanesbrands blew past analysts’ constant currency revenue expectations this quarter. We were also glad its EPS guidance for next quarter trumped Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 12.8% to $4.71 immediately after reporting.

Hanesbrands had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Nov-28 | |

| Nov-24 | |

| Nov-13 |

Stifel Nicolaus Maintains a Hold on Hanesbrands Inc. (HBI)

Insider Monkey

|

| Nov-13 | |

| Nov-11 |

Analyst Report: Hanesbrands Inc.

Morningstar Research

|

| Nov-07 | |

| Nov-06 |

Analyst Report: Hanesbrands Inc.

Morningstar Research

|

| Nov-06 | |

| Nov-05 | |

| Nov-04 | |

| Nov-03 | |

| Oct-31 | |

| Oct-30 | |

| Oct-30 | |

| Oct-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite