|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Confluent recently hit a 52-week low, as investors were not impressed by management's latest guidance.

However, the company is growing at a brisk pace and building a solid revenue pipeline.

An increase in AI-focused workloads should pave the way for stronger growth at Confluent, and its valuation makes it worth buying right now.

Data streaming platform provider Confluent (NASDAQ: CFLT) saw a sharp drop in its share price this year, which was blamed on slowing growth. Things went from bad to worse following the release of the company's latest quarterly results.

Confluent reported its second-quarter results on July 30. The stock shed almost a third of its value the following day and also touched a 52-week low on Aug. 1. Investors were quick to press the panic button despite Confluent's better-than-expected results, as management's guidance didn't inspire much confidence.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Savvy investors looking to buy a potential artificial intelligence (AI) winner should consider using Confluent's dip as a buying opportunity. Here's why.

Image source: Getty Images.

Confluent reported a 20% year-over-year increase in its revenue in the previous quarter to just over $282 million. Its earnings growth was even more impressive at 50%, to $0.09 per share. Confluent management remarked on the latest earnings conference call that it is navigating a tight spending environment.

The company, which operates a cloud-based data streaming platform to store, access, connect, and manage customers' data and applications in real time, says that its growth was hindered by customers' "optimization" initiatives. According to CEO Jay Kreps:

In Q2, our larger customers continued their optimization efforts and adopted new use cases in a more measured pace. While we are confident that this elevated level of optimization will eventually subside, our outlook for the second half assumes consumption growth notably below what we've seen in the same period of prior years.

Unsurprisingly, investors were spooked by this forecast of slowing sales growth in the second half of the year. But at the same time, one shouldn't forget that Confluent has slightly increased the lower end of its 2025 revenue guidance. What's more, the company's future revenue pipeline is improving at a brisk pace despite the controlled spending by customers.

This is evident from the 31% increase in its remaining performance obligations (RPO) in the previous quarter. RPO is the total value of a company's unfulfilled contracts at the end of a period. This metric grew at a much faster pace than the growth in Confluent's top line. That's good news, as the faster growth in Confluent's revenue backlog should allow it to eventually increase its growth rate in the future once it starts fulfilling the contracts that it's signing now.

Meanwhile, the company expects a big boost from the adoption of AI services in the cloud. Confluent says that it saw an increase in the number of customers using its data streaming platform to support real-time AI workloads such as agentic AI applications, code generation, content creation, chatbots, and others.

In fact, Confluent says that it expects "production AI use cases to grow 10x across a few hundred customers" in 2025. The company cited several examples where customers around the globe are using its data streaming solutions to build AI agents capable of handling real-time queries. Looking ahead, there's a good chance that more customers could flock to Confluent's cloud-based platform, thanks to the sharp increase that it's predicting in real-time AI use cases.

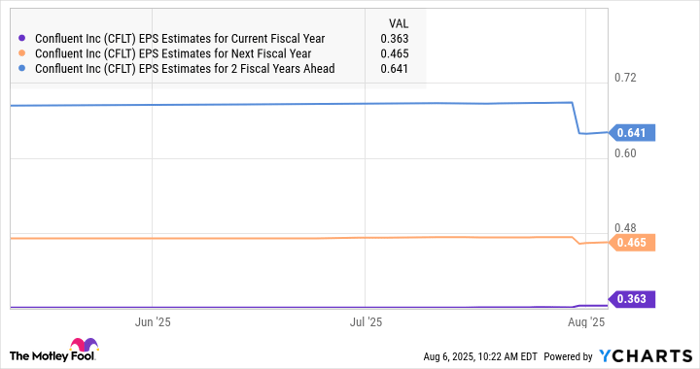

This explains why analysts expect an improvement in Confluent's earnings growth rate in the future.

Data by YCharts.

The sharp drop in Confluent's stock price this year explains why it is trading at an attractive 5 times sales right now, less than half its average five-year sales multiple. Moreover, Confluent stock trades at a discount to the U.S. technology sector's average sales multiple of 8.4. Investors can consider buying Confluent at this discounted multiple, since it is clocking a healthy revenue growth rate despite controlled customer spending.

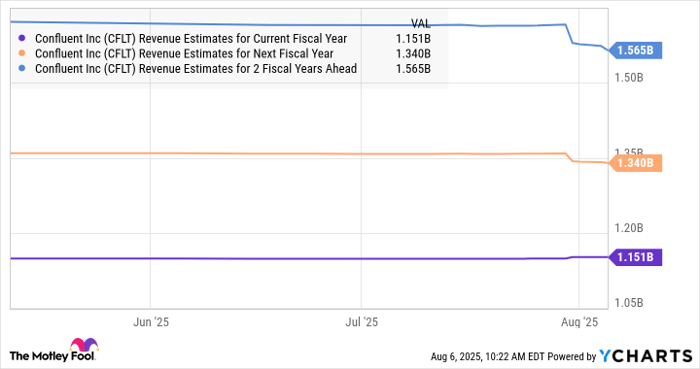

Analysts also expect its top line to grow in the mid-teens for the next couple of years, though don't be surprised to see Confluent doing better than that, given the pace at which its revenue backlog is improving.

Data by YCharts.

If the company indeed manages to outpace Wall Street's revenue expectations over the next couple of years, the market could reward it with a higher sales multiple. That could pave the way for healthy stock price upside.

Even if Confluent's revenue increases to $1.57 billion in 2027 (as per the previous chart) and it trades at even 7 times sales at that time (a discount to the U.S. technology sector's average), its market cap could hit $11 billion. That would be an increase of 86% from current levels.

So, investors looking for an AI stock that's cheap and is trading at an attractive valuation should take a closer look at Confluent, as it seems capable of stepping on the gas in the long run.

Before you buy stock in Confluent, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Confluent wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $653,427!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,119,863!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 4, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool recommends Confluent. The Motley Fool has a disclosure policy.

| Feb-13 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-04 | |

| Feb-03 | |

| Feb-01 | |

| Jan-28 | |

| Jan-28 | |

| Jan-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite