|

|

|

|

|||||

|

|

|

I'm a long-time shareholder in Eaton, an electricity-focused industrial giant.

The stock has performed very well for me, overall, and has been rallying strongly of late.

I'm a very happy Eaton shareholder, but there are some very good reasons to be cautious about buying it today.

I've owned Eaton (NYSE: ETN) since late 2015. It was one of the first stocks I bought after I had a bit of an existential crisis around the way I invested in dividend stocks (I got significantly more conservative, in case you were wondering). It is one of my best-performing investments and the business is top-notch. But would I buy it again today?

Essentially, the products industrial giant Eaton makes help to move and control power in some form. That includes within cars and trucks, airplanes, and electrical systems of all sorts, from data centers to electrical grids. When I bought Eaton, however, it was still working on integrating a major transformational purchase that materially shifted the business toward managing electricity.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

Today vehicle end markets account for 14% of revenue (including a small but growing e-mobility business). Aviation makes up another 15% of the top line. The rest is tied to electricity in some form and spread across end markets including data centers (17% of revenue), utilities (11%), commercial and institutional (20%), residential (6%), industrial (12%), and machinery (5%). The business repositioning I bought into has materially benefited Eaton in recent years, noting that revenue has risen nearly 15% over the past five years (through year end 2024) while earnings per share are up 80%.

At first blush the revenue advance and the earnings advance doesn't seem to add up. But along the way, Eaton has been focusing heavily on its profitability. So while the top line was rising, its operating margin also improved around 40%, which supercharged the bottom line. Simply put, a lot has been going right for Eaton.

While that's the past, it seems like Eaton is ready to take on the future, too. The markets it serves are all doing reasonably well and its margins have widened. The industrial giant is positioned to take advantage of major power tends, as controlling power in a world that is seeing huge power demand growth has become incredibly important. Notably, the U.S. market is expected to see electricity go from 21% of final energy use to 32% between 2020 and 2030.

As a shareholder who has owned the stock for roughly a decade, this is all good news. Indeed, I can't help but believe that the business will prosper in the years ahead. But the company's success hasn't gone unnoticed on Wall Street, with the stock up materially since I bought it. Today the value proposition just isn't as good as when I first jumped aboard. Some numbers will help.

The current price-to-sales ratio is nearly 6 compared to a five-year average of roughly 3.5. The price-to-earnings ratio is 38 versus a long-term average of a bit under 32. And the price-to-book value ratio is 8 today, compared to a five-year average of 4.3. The stock is expensive.

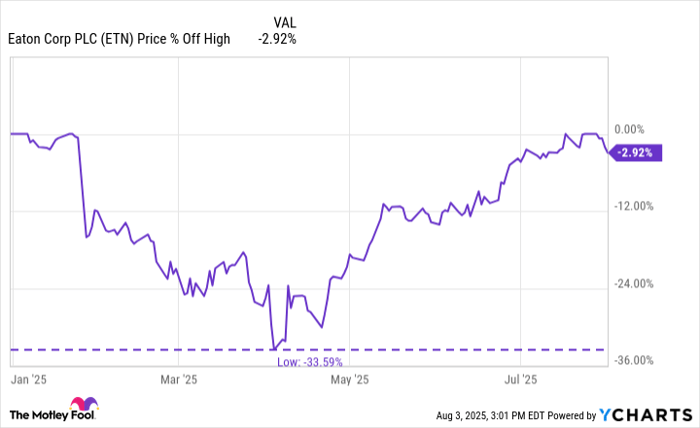

And the risk that the lofty valuation poses to new investors was highlighted earlier in 2025, when the stock lost a third of its value before rebounding back toward all-time highs. I'm not going to sell a well-run company while its business is still growing, so I'm happy to continue owning Eaton's stock. That includes sticking it out through a drawdown in the stock. But if I were looking for a stock to buy today I probably wouldn't consider buying Eaton.

Benjamin Graham, the man who trained Warren Buffett, often explained that even a great company can be a bad investment if you pay too much for it. Given the lofty valuation Eaton is fetching today, most investors will probably want to keep this great company on their wish list instead of their buy list. As the 33% drawdown earlier in 2025 highlights, the price could very quickly become more attractive if you are patient enough. But prepare now for that possibility or you may not have the resolve to jump in when Eaton is selling off on Wall Street.

Before you buy stock in Eaton Plc, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Eaton Plc wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $653,427!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,119,863!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 4, 2025

Reuben Gregg Brewer has positions in Eaton Plc. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

| 2 hours | |

| Feb-15 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite