|

|

|

|

|||||

|

|

|

Palantir's valuation multiples are at levels far beyond any of its peers in the software arena.

At the same time, the company's revenue growth and profit margins exceed comparable businesses -- potentially suggesting the stock deserves to trade at a premium.

While Palantir's growth is impressive, institutional investors may not rely as heavily on software industry metrics as much as Cramer implies.

Shares of data analytics powerhouse Palantir Technologies (NASDAQ: PLTR) soared by 141% this year. For two years running, Palantir is the top-performing stock in the S&P 500, and its momentum doesn't appear to be diminishing in the slightest.

Following the company's blowout second quarter earnings report, CNBC investment personality Jim Cramer shared his thoughts on Palantir -- even going so far as to call the stock "ridiculously cheap".

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

That's a bold statement, and one I'm not totally sold on myself. Let's explore some different valuation methodologies for Palantir and assess why Cramer still sees Palantir as a compelling buy.

Is now a good time to buy Palantir stock? Read on to find out.

Many years ago, I worked as an investment banking analyst at SunTrust Robinson Humphrey -- which is now part of Truist Financial following its merger with BB&T Capital Markets. My focus was on mergers and acquisitions, and a key part of my role involved prepping comparable company valuation analyses.

Broadly speaking, companies trade at a multiple of some profitability metric -- be it earnings, EBITDA, or free cash flow. Software-as-a-service (SaaS) businesses are a slight exception to these traditional valuation norms, however. While SaaS businesses often have healthy gross margins, they tend to reinvest excess profits to bolster sales, marketing, and product development efforts rather than capture near-term profitability.

These dynamics make valuing Palantir a little tricky. For example, Palantir currently trades for a price-to-earnings (P/E) ratio of 621 and a forward P/E of 287 -- levels so stretched that they offer little insight as very few (if any) other SaaS businesses trade at comparable multiples.

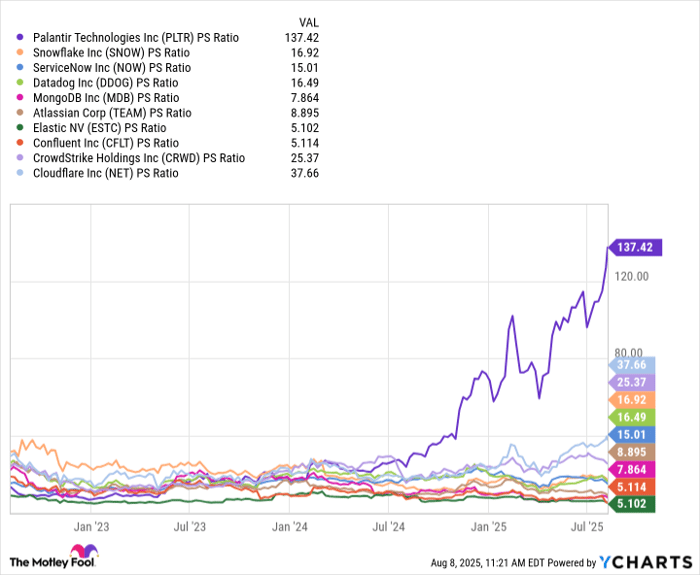

PLTR PS Ratio data by YCharts

I've benchmarked Palantir against a sizable cohort of SaaS companies specializing in data analytics, cybersecurity, cloud infrastructure, customer relationship management, and enterprise productivity.

Not only does Palantir boast a meaningfully higher price-to-sales (P/S) multiple than any of its peers, but the ratio is expanding. By this very nature, Palantir stock is becoming more expensive relative to other SaaS stocks -- suggesting the stock is well past the point of being considered overvalued.

Given these dynamics, how can Cramer justify saying Palantir stock is cheap?

Well, in order to understand his logic, investors are going to have to close the lid on traditional valuation protocols and look at some industry-specific metrics; in particular, the Rule of 40.

Image source: Getty Images.

The Rule of 40 is a SaaS metric that is calculated by taking a company's revenue growth and adding it to some sort of profit margin (i.e. free cash flow margin, operating income margin, or EBITDA margin).

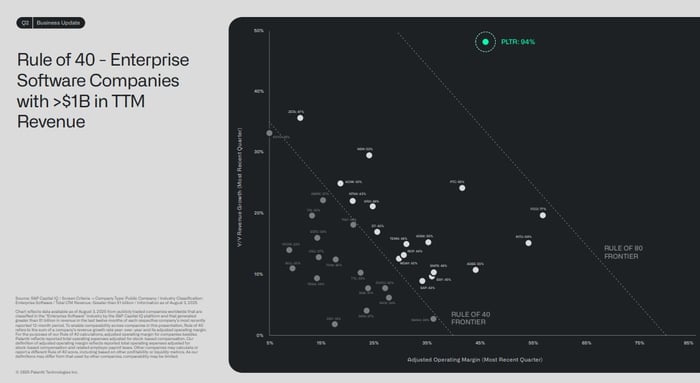

Image source: Palantir Investor Relations.

The chart above was included in Palantir's second quarter earnings report presentation. As investors can see, Palantir's Rule of 40 score of 94% is higher than any enterprise software company that generates at least $1 billion in revenue.

Palantir's combination of accelerating revenue and improving profitability is unmatched in the software sector. When viewed through the lens of the Rule of 40, it's easy to see why some investors think the company's valuation is justified.

Relying purely on the Rule of 40 to value Palantir is a controversial -- and potentially flawed -- approach.

The metric can be misleading for many reasons: short-term revenue spikes can create the illusion of sustained high growth, while profitability can appear more durable than it really is if a company chooses to use adjusted non-GAAP figures that remove certain expenses. As seen in the footnote in the slide above, Palantir uses adjusted operating margin in its Rule of 40 score. This is calculated by adding back non-cash expenses such as stock-based compensation.

Moreover, the Rule of 40 does not directly account for competitive dynamics in the broader market or the sustainability of growth -- meaning a high score does not necessarily imply that a stock is undervalued.

While I applaud Palantir's growth throughout the AI revolution, I do think the stock is overbought and view Cramer's declaration that the stock is cheap as an outlier perspective.

In practice, institutional investors at hedge funds and wealth management firms generally place greater weight on traditional valuation methodologies such as P/S, P/E, or cash flow yields over industry-specific metrics such as the Rule of 40.

If these measures suggest that a stock is overvalued -- as they do with Palantir -- institutions will likely face pressure from their limited partners to trim exposure and lock in profits rather than add to their position at a premium valuation.

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $653,427!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,119,863!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 11, 2025

Annie Dean, a Vice President at Atlassian, is a member of The Motley Fool's board of directors. Adam Spatacco has positions in Palantir Technologies. The Motley Fool has positions in and recommends Atlassian, Cloudflare, CrowdStrike, Datadog, MongoDB, Palantir Technologies, ServiceNow, Snowflake, and Truist Financial. The Motley Fool recommends Confluent and Elastic. The Motley Fool has a disclosure policy.

| 7 hours | |

| 10 hours | |

| 14 hours | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite