|

|

|

|

|||||

|

|

|

CrowdStrike Holdings Inc. (NASDAQ: CRWD) is down 9.76% in the last 30 trading days. However, CRWD stock is still up 79% in 2025, making it one of the best-performing technology stocks in the S&P 500.

The stock’s year-long rally started after the much-publicized outage caused by a faulty software update. The company took aggressive steps in damage control that restored customer confidence in the company.

Good public relations wouldn’t have meant much if the company didn’t back it up with results. CrowdStrike has done well with revenue and earnings, increasing year-over-year (YOY).

However, two weeks before the company reports earnings, CrowdStrike is facing concerns about valuation. That’s part of the reason the stock is down ahead of earnings.

To be fair, CrowdStrike isn’t the only company facing valuation concerns, but investors need to consider how much they want to pay for CRWD stock with earnings fast approaching.

One point for investors to consider is the company’s expansion of its AI-native Falcon platform. Approximately 92% of Fortune 500 companies use generative and/or agentic artificial intelligence (AI) in one or more business areas.

Using large language models (LLMs), copilots, and AI agents creates productivity opportunities that may exceed those of the internet. However, that’s also creating new risks and vulnerabilities that cybersecurity companies are racing to address.

A key selling point of CrowdStrike’s Falcon platform is that it is AI-native. Recently, the company announced the launch of AI Systems Security Assessment and AI for SecOps Readiness. These two services allow customers to secure AI systems while safely integrating AI into their security operations.

In its earnings presentation for the first quarter of its 2026 fiscal year, CrowdStrike reported $194 million in new net annual recurring revenue (ARR). ARR is a key metric for cybersecurity companies because it shows how much of the topline the company can retain YOY.

For the current calendar year, CrowdStrike predicts that the total addressable market (TAM) for AI-native cybersecurity platforms will be $116 billion. The company forecasts that number to rise to $250 billion by 2029.

Now consider that CrowdStrike just notched its first $1 billion in quarterly revenue in its most recent quarter. That means CrowdStrike has under 5% market share. However, management sees the long-term opportunity as more customers adopt its platformization strategy. Investors may need to ensure they’re viewing the opportunity clearly.

Investors commonly use the price-to-earnings (P/E) ratio when considering a company's valuation. CrowdStrike currently has a forward P/E of 771x. That’s a little deceiving because the company reported negative GAAP earnings of 44 cents in the last quarter. That was attributable to high stock-based compensation (SBC).

Paying employees with stock is not unusual, particularly for a growing technology company like CrowdStrike. However, the company does have an unusually high amount of SBC, similar to that of Palantir, which also faces concerns about a high valuation.

CrowdStrike’s FY2026 outlook suggests the company can generate over $1.3 billion in adjusted operating profit, making its lofty forward multiple look reasonable on a non-GAAP basis. However, on a GAAP basis, stock-based compensation running at nearly 20% of revenue will weigh on earnings.

So what’s next? CrowdStrike’s guidance implies it will still have less than 5% share of its $103 billion core cybersecurity market. To triple its non-GAAP operating profits, the company would have to increase its forecasted revenue by about 2.2x, meaning a 10% market share.

That would put its annual revenue on par with Palo Alto Networks Inc. (NASDAQ: PANW), a company also using a platformization strategy.

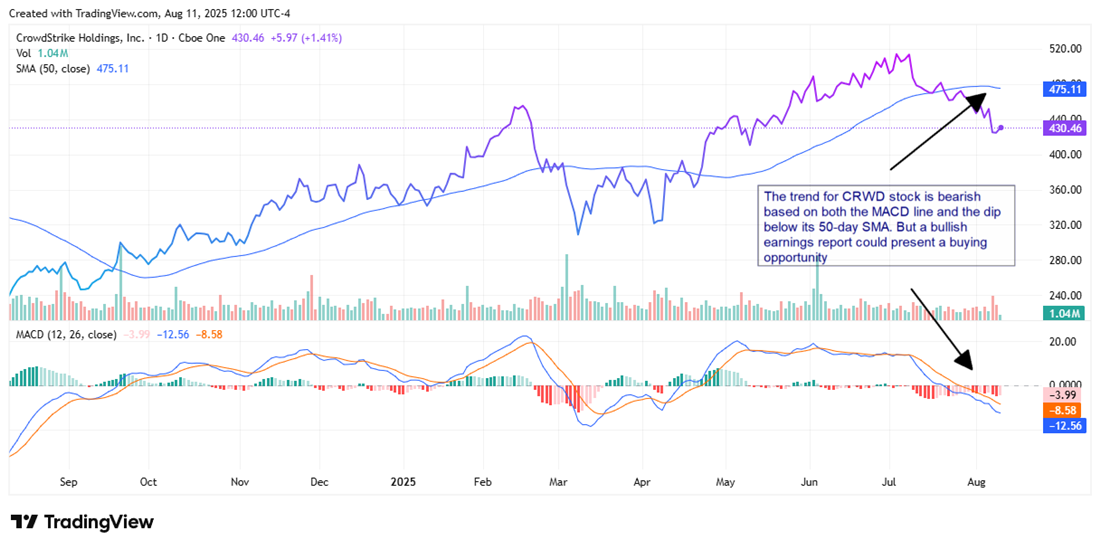

CrowdStrike stock has lost its bullish momentum. The stock has crossed below its 50-day simple moving average (SMA), and its MACD is well below the signal line, but may be showing signs of flattening. That’s consistent with an RSI around 36, which suggests a strong earnings report could cause a trend reversal.

If that’s the case, investors should look at $475 as an area of resistance. If the stock can push past that, it could signal a broader rally back above $500 and towards all-time highs.

If the results disappoint, areas of support could be at $400 (a round number and near February 2025 lows). If it slices below that, investors would have a significant buying opportunity around $375 to $380.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "CrowdStrike Faces Valuation Test Before Key Earnings Report" first appeared on MarketBeat.

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-08 | |

| Feb-07 | |

| Feb-07 | |

| Feb-07 | |

| Feb-07 | |

| Feb-06 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite