|

|

|

|

|||||

|

|

|

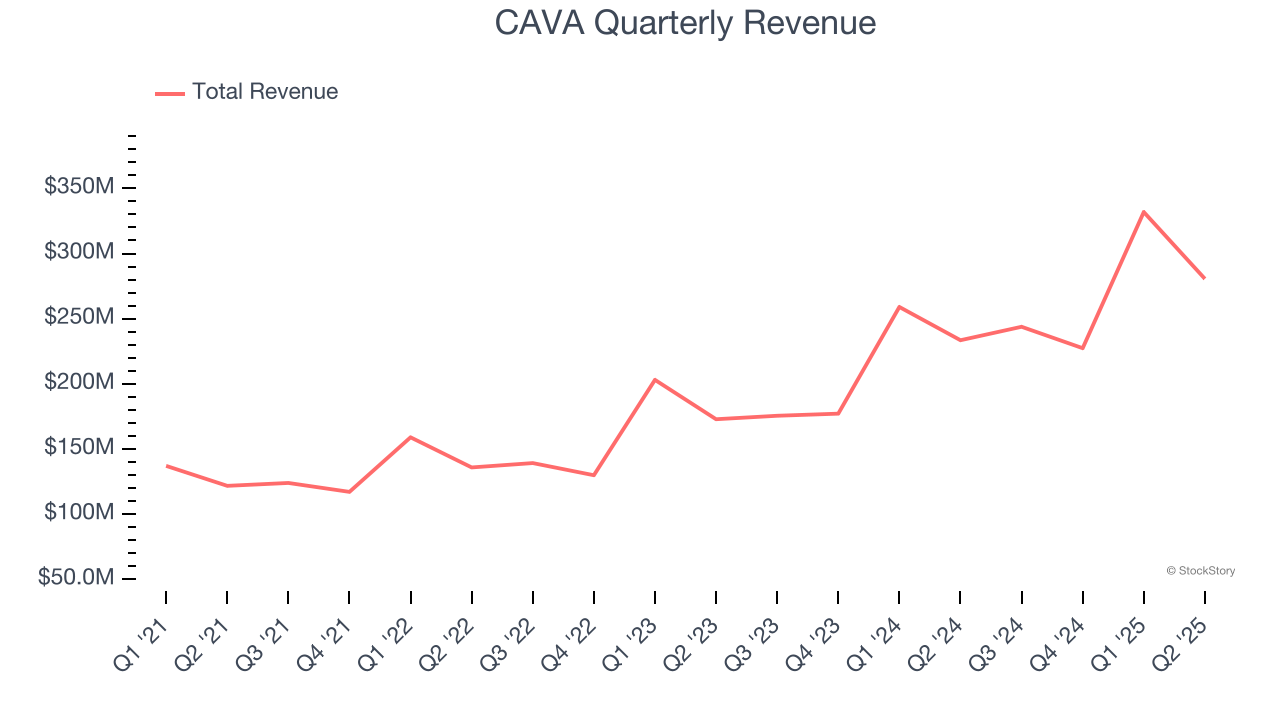

Mediterranean fast-casual restaurant chain CAVA (NYSE:CAVA) missed Wall Street’s revenue expectations in Q2 CY2025, but sales rose 20.2% year on year to $280.6 million. Its non-GAAP profit of $0.16 per share was 18.7% above analysts’ consensus estimates.

Is now the time to buy CAVA? Find out by accessing our full research report, it’s free.

“During the second quarter of 2025, we continued to grow market share and firmly establish our category-defining leadership position,” said Brett Schulman, Co-Founder and CEO.

Starting from a single Washington, D.C. location, CAVA (NYSE:CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.08 billion in revenue over the past 12 months, CAVA is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, CAVA’s sales grew at an incredible 24% compounded annual growth rate over the last four years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, CAVA generated an excellent 20.2% year-on-year revenue growth rate, but its $280.6 million of revenue fell short of Wall Street’s high expectations.

Looking ahead, sell-side analysts expect revenue to grow 22% over the next 12 months, a slight deceleration versus the last four years. Despite the slowdown, this projection is commendable and suggests the market is baking in success for its menu offerings.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

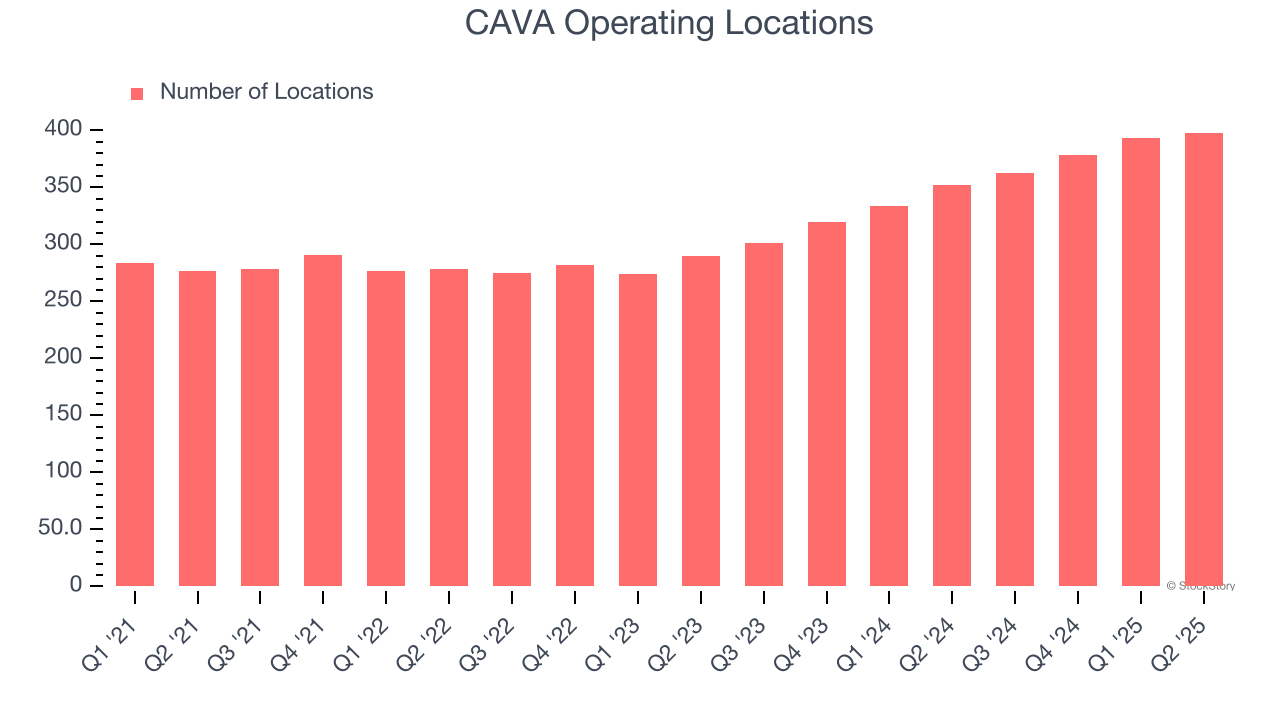

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

CAVA operated 398 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 17% annual growth, much faster than the broader restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

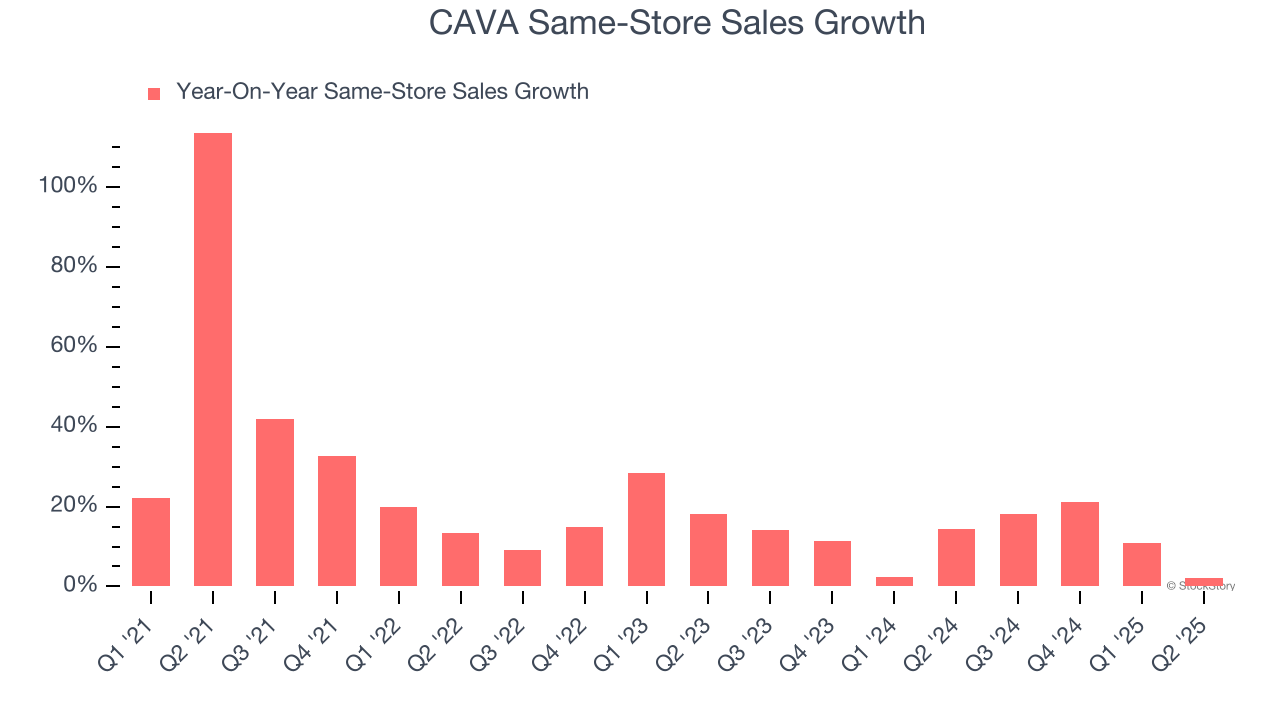

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

CAVA has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 11.8%. This performance along with its meaningful buildout of new restaurants suggest it’s playing some aggressive offense.

In the latest quarter, CAVA’s same-store sales rose 2.1% year on year. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if CAVA can reaccelerate growth.

We enjoyed seeing CAVA beat analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its same-store sales missed and its full-year EBITDA guide fell short. Overall, this was a weaker quarter. The stock traded down 22% to $65.98 immediately following the results.

CAVA underperformed this quarter, but does that create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| 2 hours | |

| 2 hours | |

| 5 hours |

Cava Fourth-Quarter Sales Rise on Higher Prices, New Restaurant Openings

CAVA

The Wall Street Journal

|

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 13 hours | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-21 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite