|

|

|

|

|||||

|

|

|

Over the past six months, Saia’s shares (currently trading at $349.43) have posted a disappointing 19.4% loss while the S&P 500 was down 1.7%. This might have investors contemplating their next move.

Is now the time to buy Saia, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're cautious about Saia. Here are three reasons why we avoid SAIA and a stock we'd rather own.

Pivoting its business model after realizing there was more success in delivering produce than selling it, Saia (NASDAQ:SAIA) is a provider of freight transportation solutions.

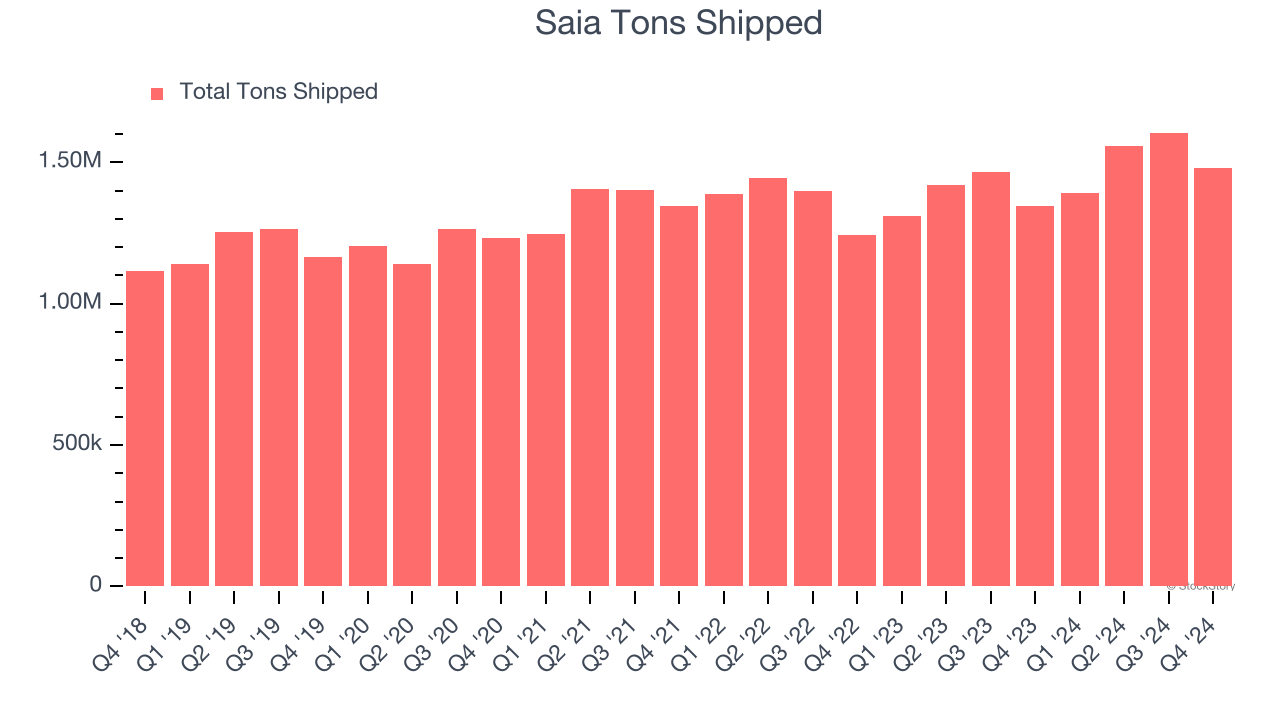

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Ground Transportation company because there’s a ceiling to what customers will pay.

Saia’s tons shipped came in at 1.48 million in the latest quarter, and over the last two years, averaged 5.2% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

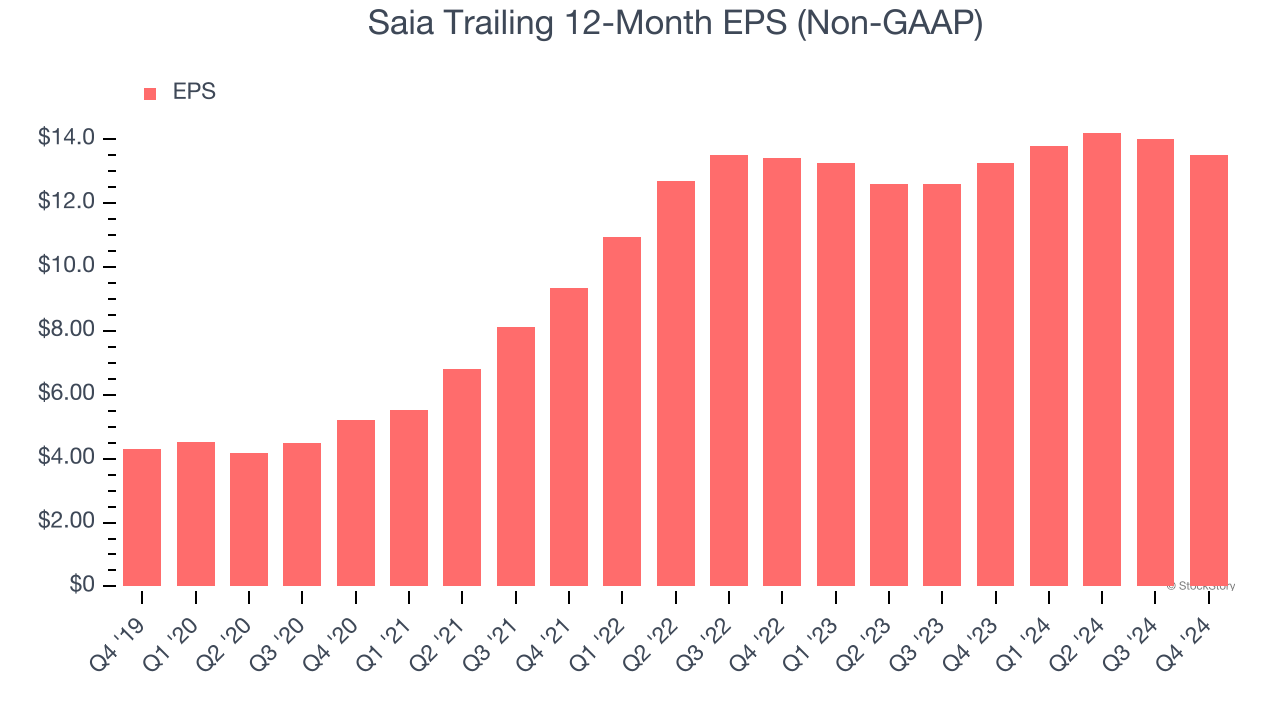

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Saia’s flat EPS over the last two years was worse than its 7.2% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

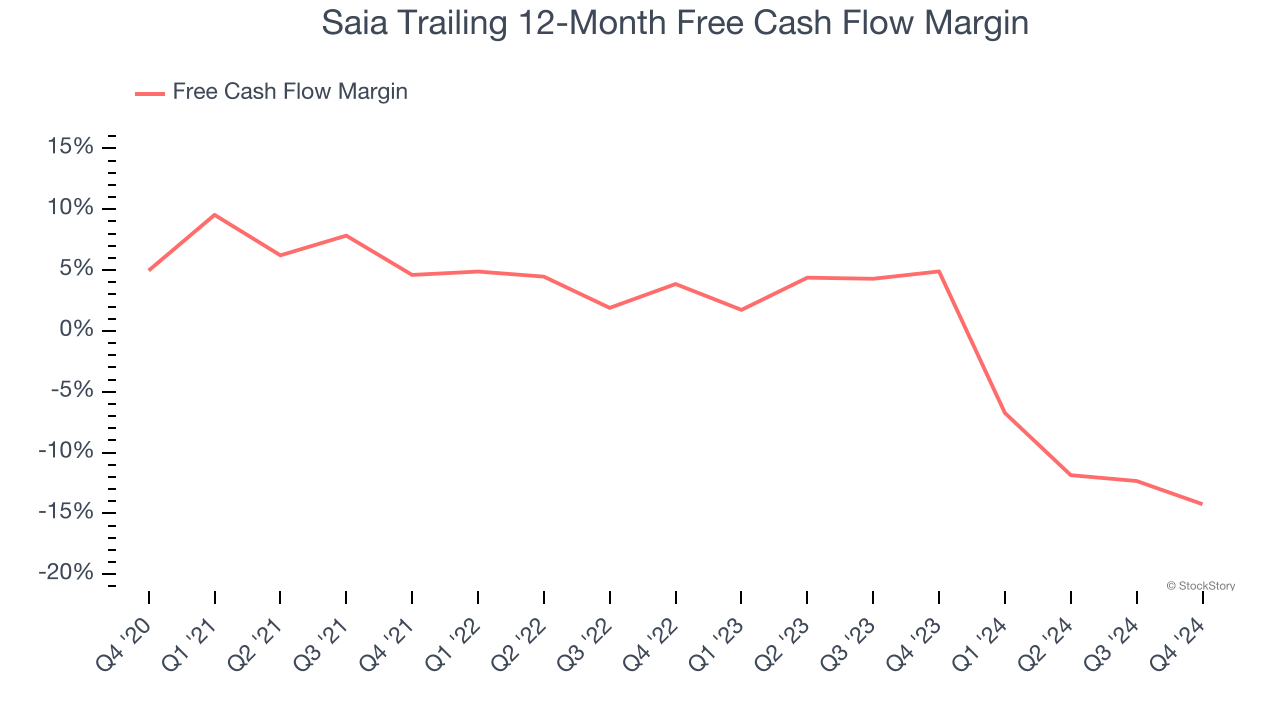

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Saia’s margin dropped by 19.2 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business. Saia’s free cash flow margin for the trailing 12 months was negative 14.2%.

Saia isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 22.3× forward price-to-earnings (or $349.43 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.

| Feb-25 | |

| Feb-18 | |

| Feb-15 | |

| Feb-11 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite