|

|

|

|

|||||

|

|

|

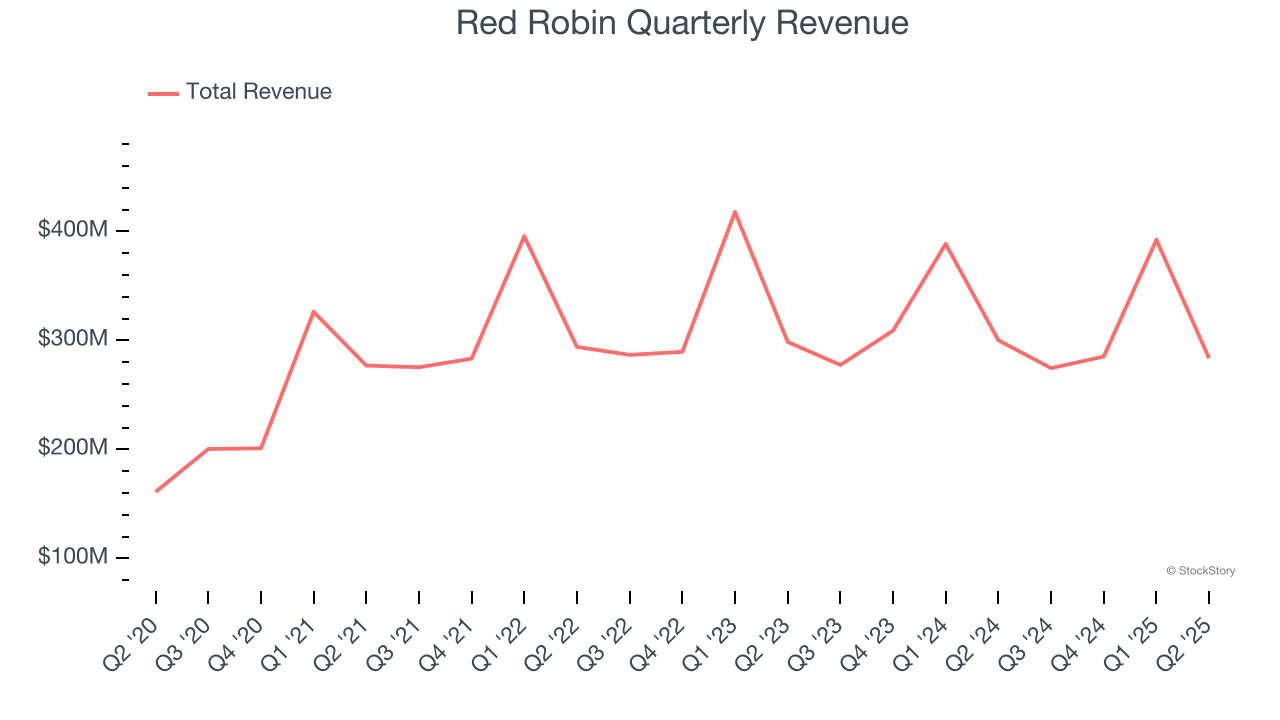

Burger restaurant chain Red Robin (NASDAQ:RRGB) reported Q2 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 5.5% year on year to $283.7 million. On the other hand, the company’s full-year revenue guidance of $1.2 billion at the midpoint came in 1% below analysts’ estimates. Its non-GAAP profit of $0.26 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Red Robin? Find out by accessing our full research report, it’s free.

Dave Pace, Red Robin's President and Chief Executive Officer said, "We have begun executing on the strategic elements of our First Choice plan and are already seeing encouraging results. Since launching our Big YUMMM Burger Deal in July, we have seen meaningful improvement in traffic compared to our second quarter exit rate. This value-driven offering, combined with our upcoming First Choice marketing launch represents the foundation of our multi-layered approach to sustainable traffic growth."

Known for its bottomless steak fries, Red Robin (NASDAQ:RRGB) is a chain of casual restaurants specializing in burgers and general American fare.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.24 billion in revenue over the past 12 months, Red Robin is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Red Robin’s revenue declined by 1.1% per year over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it closed restaurants and observed lower sales at existing, established dining locations.

This quarter, Red Robin’s revenue fell by 5.5% year on year to $283.7 million but beat Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to decline by 3.6% over the next 12 months, a slight deceleration versus the last six years. This projection is underwhelming and implies its menu offerings will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

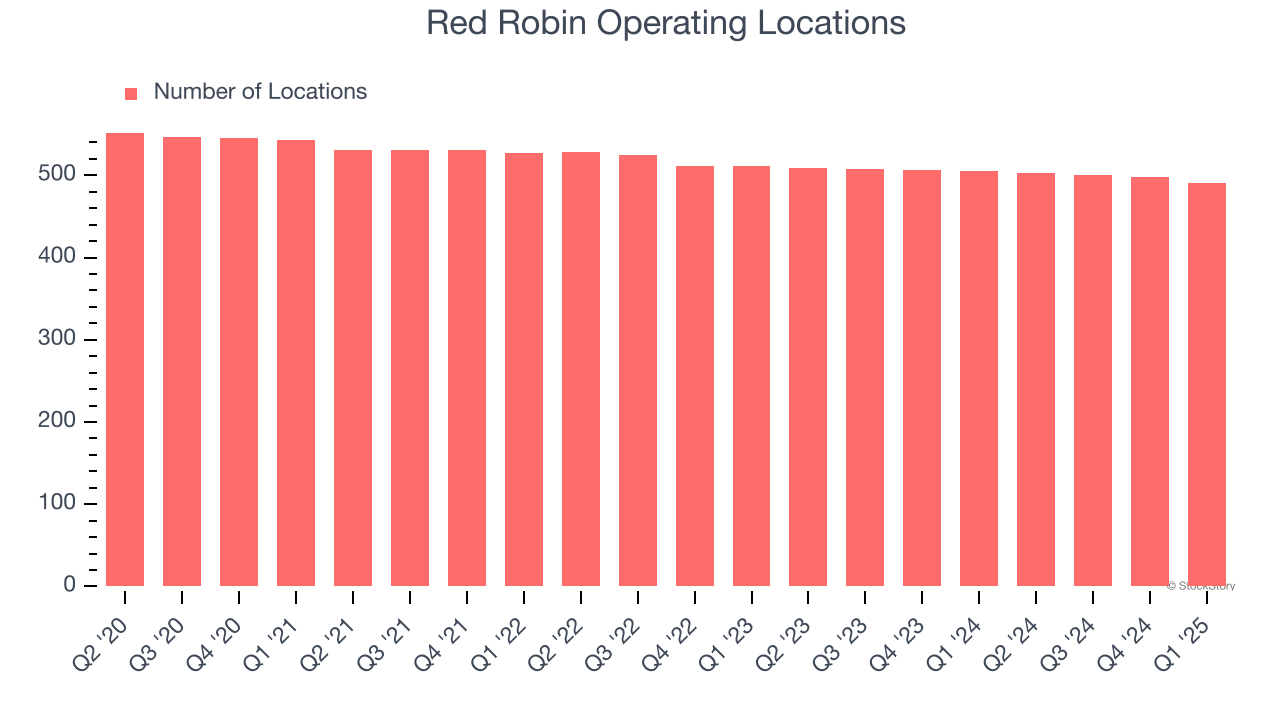

Over the last two years, Red Robin has generally closed its restaurants, averaging 1.8% annual declines.

When a chain shutters restaurants, it usually means demand for its meals is waning, and it is responding by closing underperforming locations to improve profitability.

Note that Red Robin reports its restaurant count intermittently, so some data points are missing in the chart below.

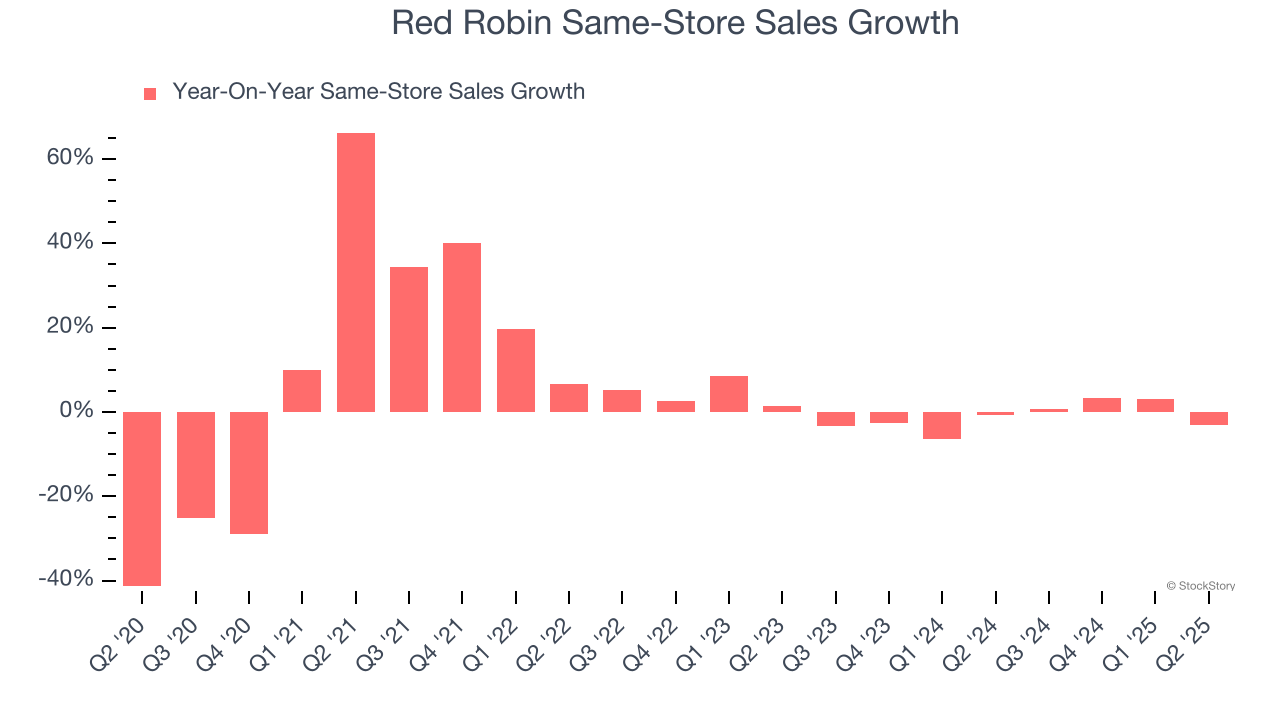

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Red Robin’s demand has been shrinking over the last two years as its same-store sales have averaged 1.2% annual declines. This performance isn’t ideal, and Red Robin is attempting to boost same-store sales by closing restaurants (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Red Robin’s same-store sales fell by 3.2% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

It was good to see Red Robin beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EBITDA guidance missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 5.5% to $6.31 immediately after reporting.

Indeed, Red Robin had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| Jun-15 | |

| May-29 | |

| May-28 | |

| May-20 | |

| May-20 | |

| May-19 | |

| May-19 | |

| May-19 | |

| May-13 | |

| May-05 | |

| Apr-29 | |

| Apr-13 | |

| Apr-06 | |

| Mar-10 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite