|

|

|

|

|||||

|

|

|

Note: The following is an excerpt from this week’s Earnings Trends report. You can access the full report that contains detailed historical actual and estimates for the current and following periods, please click here>>>

Here are the key points:

The revisions trend continues to remain favorable, as we have consistently been flagging in recent weeks. We see this in estimates for the current period (2025 Q3) as well as for the last quarter of the year.

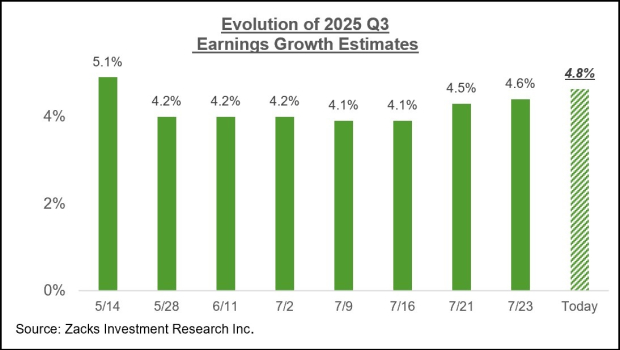

For 2025 Q3, the expectation is for earnings growth of +4.8% on +5.4% revenue gains. The chart below shows how Q3 earnings growth expectations have evolved in recent weeks.

Since the start of Q3 this month, estimates have modestly increased for five of the 16 Zacks sectors, including Finance, Tech, Energy, Retail, and others.

On the negative side, Q3 estimates remain under pressure for the remaining 11 Zacks sectors, with significant declines to estimates for the Medical, Basic Materials, Construction, Transportation, and other sectors.

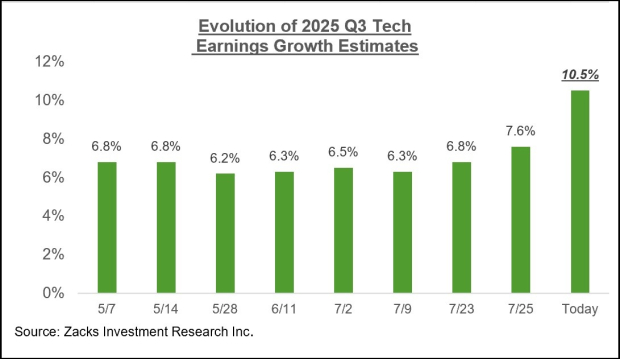

For the Tech sector, Q3 earnings are expected to be up +10.5% from the same period last year on +11.6% higher revenues. The chart below shows how the sector’s Q3 earnings growth expectations have evolved over the last couple of months.

You can look at Q3 estimates for Tech players like Meta Platforms META, Alphabet GOOGL, and others.

Meta, which reported Q2 results on July 30th, is currently expected to bring in $6.69 per share in earnings in Q3. Estimates for Meta have been on a steady upward trend, with the current $6.69 EPS estimate increasing by 14.4% over the past month and 17.4% over the past two months. Alphabet, which reported Q2 results on July 23rd, is expected to earn $2.32 per share in Q3, with the estimate up +5.9% over the past month and +7.4% over the past two months.

This positive revisions trend is even more notable for the big banks and brokers like JPMorgan, Citigroup, Goldman Sachs, and others in the Finance sector.

The positive results from more than 90% of S&P 500 members have helped push the Q2 earnings growth expectation higher, with earnings for the S&P 500 index now expected to increase by +12.0% from the same period last year on +6.0% higher revenues.

The chart below shows expectations for 2025 Q2 in terms of what was achieved in the preceding four periods and what is currently expected for the next three quarters.

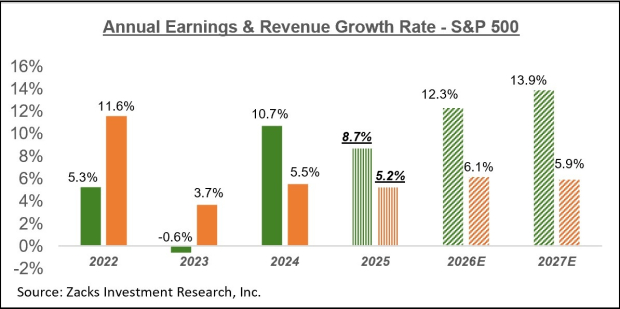

The chart below shows the overall earnings picture for the S&P 500 index on an annual basis.

We have been pleasantly surprised by the aforementioned favorable revisions trend, which validates the market’s rebound from the April lows. Given the positive run of Q2 results, it will make sense for this trend to remain in place over the coming weeks as we go through this reporting cycle.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 | |

| Jul-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite