|

|

|

|

|||||

|

|

|

Enterprise Products Partners L.P. EPD significantly benefits from its extensive, diversified asset base and stable fee-based revenue streams, which bolster its financial stability and growth potential. The partnership owns more than 50,000 miles of pipelines, 300 million barrels of storage capacity for NGLs, crude oil, petrochemicals and refined products. It also has 14 billion cubic feet of natural gas storage capacity.

This efficient structure supports high utilization rates and operational efficiency across multiple commodity value chains, from production and processing to transportation, storage and export.

A major advantage for EPD is the considerable share of fee-based contracts in its portfolio, which accounted for approximately 78-82% of its gross operating margin in recent years. These contracts, covering pipeline tariffs, fractionation, storage and terminal services, provide predictable cash flows mainly insulated from commodity price volatility.

For example, strong performance from fee-based natural gas processing and marketing offset weaker crude oil marketing results in the second quarter of 2025, helping the partnership deliver $1.9 billion in distributable cash flow with 1.6X distribution coverage.

This combination of robust infrastructure and stable revenue generation enables EPD to maintain investment-grade credit metrics, support consistent distribution growth for 27 consecutive years, and reinvest in high-return organic growth projects. By anchoring earnings in fee-based activities while leveraging its expansive asset footprint, EPD enhances its competitive positioning and long-term value creation potential.

Kinder Morgan KMI benefits from its substantial base of stable, fee-based revenues, which account for roughly 26% of its cash flow mix. These fixed fees are collected regardless of commodity prices, ensuring predictable income streams even during market volatility. More than 40% of these revenues come from highly stable refined product operations, underpinning the company’s ability to fund growth projects and shareholder returns.

MPLX LP MPLX similarly enjoys the stability of long-term, fee-based contracts, particularly from its gathering, processing and NGL infrastructure. Its newly acquired Northwind Midstream assets, supported by minimum volume commitments averaging 13 years, are expected to deliver above-average rates due to higher CO2 and H2S treating requirements. This structure enhances cash flow resilience, enabling MPLX to sustain mid-single-digit EBITDA growth while supporting consistent distribution increases.

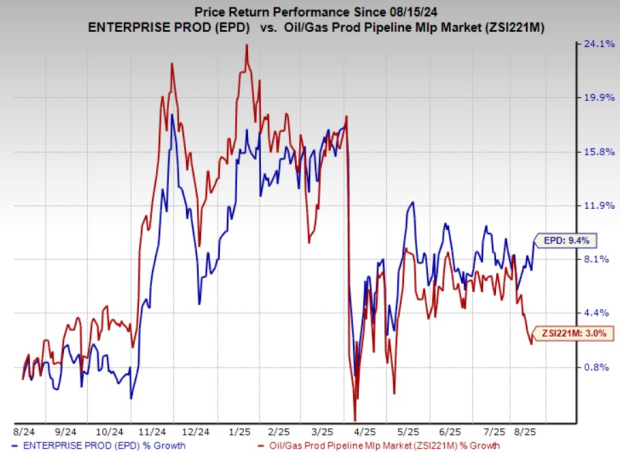

EPD units have gained 9.4% over the past year, outpacing 3% growth of the composite stocks belonging to the industry.

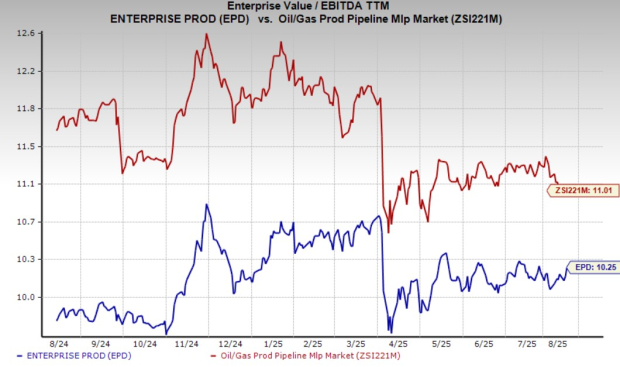

From a valuation standpoint, EPD trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 10.25X. This is below the broader industry average of 11.01X.

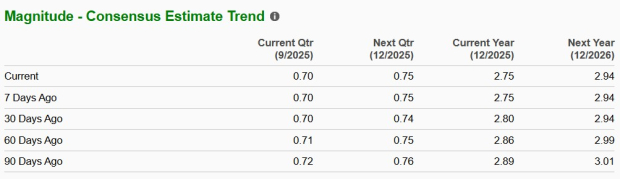

The Zacks Consensus Estimate for EPD’s 2025 earnings has been revised downward over the past 30 days.

EPD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-15 | |

| Jul-13 | |

| Jul-07 | |

| Jul-01 | |

| Jul-01 | |

| Jun-30 | |

| Jun-16 | |

| Jun-05 | |

| Jun-05 | |

| May-18 | |

| May-14 | |

| May-11 | |

| May-05 | |

| May-05 | |

| Apr-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite