|

|

|

|

|||||

|

|

|

A focus on quickly expanding its AI data centers is translating into outstanding growth for Nebius.

It is making its data centers more efficient and is aiming to corner a bigger share of the infrastructure-as-a-service market that's growing rapidly.

The stock may seem expensive at first, but its phenomenal growth justifies the premium valuation.

Nebius Group (NASDAQ: NBIS) has been one of the hottest stocks on the market in 2025, rising a stunning 154% as of this writing on account of the outstanding growth that it has been delivering. Importantly, it looks like this cloud infrastructure provider has room for more upside even after its phenomenal rally.

Nebius is a Dutch company that provides artificial intelligence (AI) cloud computing infrastructure. It operates AI data centers with large-scale graphics processing unit (GPU) clusters and provides tools and software solutions that customers can use to train AI models and run inference applications.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

The AI cloud infrastructure market that Nebius serves is growing at a breathtaking pace. Let's take a closer look at Nebius and see why this red-hot growth stock has room for more upside.

Image source: Getty Images.

Nebius has built its business by accumulating powerful AI GPUs from Nvidia and renting them out to customers. Developers can access a range of Nvidia GPUs such as the H100, the H200, and B200 at hourly rates from Nebius and run various AI models from Microsoft, Meta Platforms, DeepSeek, and others.

Nebius' full-stack AI infrastructure allows customers to train and fine-tune AI models, develop custom AI applications, and run inference tasks. Importantly, customers can increase or decrease the usage of Nebius' platform according to their needs. The company's latest quarterly results make it clear that its business model is a hit with customers.

Its revenue in the second quarter of 2025 jumped by more than 7x year over year to $105 million. Nebius also reduced its net loss by 49% owing to its focus on lowering the operating costs of data centers. Management points out that Nebius lowered its total cost of ownership by 20% by improving the hardware design of its data centers and investing in energy-saving solutions.

Looking ahead, Nebius is focused on aggressively expanding its data center capacity so that it can corner a bigger share of the fast-growing cloud AI infrastructure market. The company aims to boost its data center capacity to 220 megawatts by the end of 2025 before ramping it up to 1 gigawatt by the end of next year.

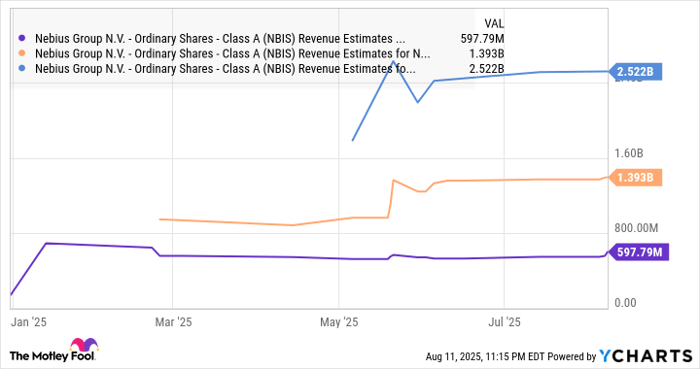

Nebius was sitting on $1.68 billion worth of cash at the end of the previous quarter, which it will use for capacity expansion. The company says that the demand for its solutions is outpacing supply, which is why it is important for it to keep investing in more capacity. Also, higher data center capacity will translate into more business for Nebius, which explains why the company has increased its annualized run-rate revenue (ARR) for 2025.

It now expects ARR to land between $900 million and $1.1 billion this year as compared to the earlier estimate of $750 million to $1 billion. Analysts, meanwhile, are expecting Nebius' top line to jump by over 5x in 2025, followed by robust growth over the next couple of years as well.

NBIS Revenue Estimates for Current Fiscal Year data by YCharts

However, don't be surprised to see Nebius blowing past analysts' expectations in the current year and beyond. The company was originally guiding for $500 million to $700 million in revenue for 2025, and the increased ARR guidance indicates that it could exceed the midpoint of its original guidance range. So, a stronger-than-expected performance going forward should set Nebius up for more gains.

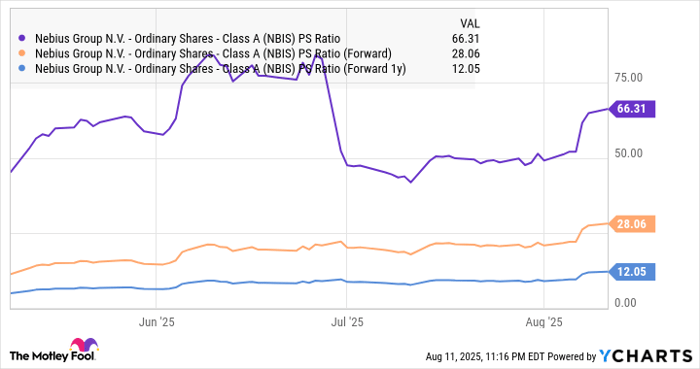

Nebius' remarkable rally this year has brought the stock's price-to-sales ratio to 66. That's well above the U.S. technology sector's average sales multiple of 8.7. However, Nebius' outstanding growth explains why it is richly valued. The company is growing at an eye-popping pace and is relatively cheaper than some other AI stocks.

What's more, the outstanding sales growth that the company is expected to deliver in the future is the reason why its forward sales multiples are much lower.

NBIS PS Ratio data by YCharts

Finally, investors shouldn't forget that Nebius is operating in a market that's expected to grow rapidly in the long run. Fortune Business Insights estimates that the cloud infrastructure-as-a-service market could clock an annual growth rate of almost 21% through 2032, generating more than $712 billion in annual revenue at the end of the forecast period.

Nebius is currently growing at a much faster pace than the end market, and its capacity expansion efforts should allow it to become a key player in this space. All this makes Nebius a top AI stock to buy right now as its phenomenal growth is likely to result in more upside.

Before you buy stock in Nebius Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nebius Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $649,544!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,113,059!*

Now, it’s worth noting Stock Advisor’s total average return is 1,062% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Nebius Group and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 2 hours | |

| 2 hours |

AI Stealth Play Receives Bullish Initiation; Data Center Revenue Expected To Grow 64%

NBIS +5.43%

Investor's Business Daily

|

| 2 hours | |

| 4 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-14 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite