|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Tobacco giant Altria Group has outperformed the broad market in 2025.

Price hikes continue to stabilize the company's cash flows.

An ongoing share buyback program will support dividend growth in the years to come.

The stock market is soaring. On a total return basis, the S&P 500 is up 10% year to date, 57% in the past three years, and over 100% in the last five years.

It may surprise you to learn, however, that leading tobacco company Altria Group (NYSE: MO) has been outperforming the broad market, despite the long-term decline of smoking in the U.S. That's due in large part to the stock's juicy dividend, which yields 6.2% as of this writing.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Altria reported its second-quarter earnings on July 30. Results showed continued progress in its strategy to optimize cash flows over the long term. The stock has steadily climbed following the report and is now up over 25% so far this year.

The recent gains mean Altria is trading at levels not seen since 2018. Should you buy this dividend stock as it approaches its previous all-time high? Let's look at the numbers and find out.

Altria holds the rights to the famed Marlboro cigarette brand in the U.S. It has employed a consistent strategy for decades to optimize cash flows from the shrinking cigarette category. In the face of consistent volume declines and waning demand from consumers in the country, Altria regularly raises prices on cigarettes, counteracting the volume declines.

Q2 numbers illustrate this dynamic. Altria's cigarette volume declined 10.2% year over year, while revenue net of excise taxes was flat year over year. Operating income still grew 4.4% for the smokeables category, which was helped by the cigars segment where the Black & Mild brand posted volume increases.

These price hikes are how Altria consistently increases its free cash flow. In the last 12 months, the company generated $8.7 billion in free cash flow, which is close to a record high (excluding a 2020 period of irregular inventory and working capital dynamics). As price hikes continue, Altria Group should see stable cash flows from the cigarette and smokeables division as a whole.

Image source: Getty Images.

Like the other nicotine giants, Altria Group has made investments into alternative nicotine categories such as vaping and nicotine pouches. Some of these have been successful, while others were wild failures, such as its investment in Juul vaping before the brand's collapse. Today, the company is showing growth with its On! nicotine pouch brand and NJOY vaping division.

On! volume grew 26.5% year over year last quarter to 52.1 million cans sold. However, this didn't even fully counteract the volume declines from chewing tobacco brands such as Copenhagen as overall oral nicotine volumes were down 1.0%. Oral nicotine revenue net of excise taxes was $728 million last quarter, or just 16% of the size of Altria's smokeables division.

Something that could affect Altria's growth going forward is a government crackdown on illicit vaping devices, which have flooded the U.S. market. These devices are technically illegal, but they're wildly popular and eat into sales for Altria's nicotine pouches, vaping products, and even cigarettes. A stricter regulatory environment could be a boon for volume growth across the business.

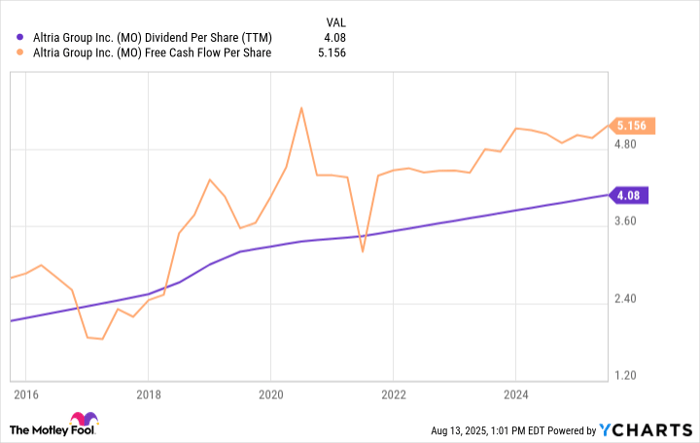

Data by YCharts.

At the end of the day, cash flows from legacy smokeable products will continue to drive the business for years to come. With these cash flows, management returns capital to shareholders through share repurchases and dividends.

Altria's free cash flow per share was $5.16 over the last 12 months. This gives the company plenty of coverage for its $4.08 dividend per share payout to shareholders. With the excess cash accumulating on the balance sheet, management is retiring shares outstanding through stock buybacks, which will further boost free cash flow per share and help with future dividend growth. Over the last 10 years, Altria's shares outstanding have fallen 14%.

Price increases, margin expansion, and a little help from newer categories like nicotine pouches can help Altria maintain its overall free cash flow levels, allowing Altria to sustain its streak of annual dividend increases. With a 6.2% yield, Altria Group still looks like a good dividend stock to buy today, even after its strong gains year to date.

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $668,155!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,106,071!*

Now, it’s worth noting Stock Advisor’s total average return is 1,070% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 | |

| Feb-13 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-06 | |

| Feb-06 | |

| Feb-05 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite