|

|

|

|

|||||

|

|

|

As digital content dominates the modern landscape, traditional media organizations must adapt to stay relevant. The New York Times Company NYT has successfully embraced this transformation, making digital subscriptions a key revenue source. By prioritizing high-quality journalism, tailored content and strategic pricing, NYT has bolstered its subscriber base. The company has also broadened its digital offerings beyond news, incorporating lifestyle, cooking, crosswords and more, each playing a role in its subscription expansion.

The New York Times has prioritized digital subscriptions as a core revenue stream, offsetting declines in print circulation and advertising. By leveraging a well-structured paywall, strategic pricing and engaging content, the company has steadily increased its subscriber base.

At the end of the fourth quarter of 2024, The New York Times Company had approximately 11.43 million subscribers across its print and digital products, including 10.82 million digital-only subscribers. Of the 10.82 million subscribers, 5.44 million were bundle and multi-product subscribers. Compared to the third quarter, the company added 350,000 net digital-only subscribers, underscoring its steady growth trajectory.

Subscription revenues of $466.6 million grew 8.4% year over year during the fourth quarter. Subscription revenues from digital-only products jumped 16% to $334.9 million. This reflects an increase in bundle and multi-product revenues and a rise in other single-product subscription revenues.

The New York Times Company consistently grew its digital-only average revenue per user (ARPU). ARPU increased to an impressive $9.65 in the fourth quarter from $9.24 in the year-ago period. This rise in ARPU can be attributed to subscribers transitioning from promotional pricing to higher rate plans and price hikes for tenured non-bundle subscribers.

The New York Times Company expects further gains in subscription revenues in the first quarter of 2025. Management envisions first-quarter total subscription revenue growth of 7-10%, with digital-only subscription revenues anticipated to rise 14-17%, signaling continued momentum in its digital business.

By focusing on building a loyal, paying subscriber base, The New York Times has reduced its reliance on advertising revenues, which can be volatile.

The New York Times Company’s strategic focus on subscription growth and digital innovation has proven to be a key driver of its success in a competitive media landscape. Its ability to consistently expand its digital offerings, attract new subscribers and optimize ARPU showcases its resilience and strong market positioning. However, the decline in print advertising revenues remains a concern, with a 16.4% drop in the fourth quarter of 2024 highlighting the challenges in the traditional print sector. The New York Times Company currently carries a Zacks Rank #3 (Hold).

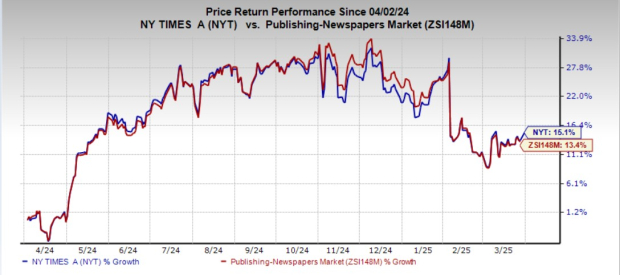

Shares of The New York Times Company have risen 15.1% in the past year compared with the industry’s growth of 13.4%.

Affirm Holdings, Inc. AFRM, which operates a payment network in the United States, Canada and internationally, currently sports a Zacks Rank #1 (Strong Buy). AFRM has a trailing four-quarter average earnings surprise of 84.1%. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Affirm Holdings’ current financial-year sales and earnings suggests growth of 36.9% and 94%, respectively, from the year-ago reported numbers.

Reddit, Inc. RDDT, a social media platform and online forum, currently sports a Zacks Rank #1. RDDT has a trailing four-quarter average earnings surprise of 194.1%.

The Zacks Consensus Estimate for Reddit’s current financial-year sales and earnings implies growth of 40.4% and 134.8%, respectively, from the year-ago reported numbers.

Arista Networks Inc. ANET, an industry leader in data-driven, client-to-cloud networking for large AI, data center, campus and routing environments, currently carries a Zacks Rank #2 (Buy). ANET has a trailing four-quarter average earnings surprise of 12.9%.

The Zacks Consensus Estimate for Arista Networks’ current financial-year sales and earnings calls for growth of 18.1% and 12.8%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-10 | |

| Apr-10 | |

| Apr-10 | |

| Apr-10 | |

| Apr-10 | |

| Apr-10 | |

| Apr-09 | |

| Apr-09 | |

| Apr-08 | |

| Apr-08 | |

| Apr-08 | |

| Apr-07 | |

| Apr-07 | |

| Apr-07 | |

| Apr-07 |

Arista Upgraded To Buy On Google, Anthropic Data Center Orders

ANET +5.85%

Investor's Business Daily

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite