|

|

|

|

|||||

|

|

|

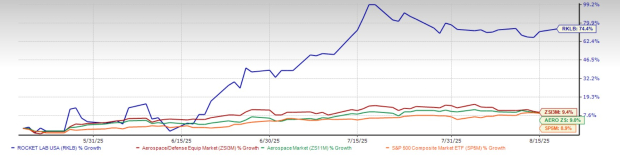

Shares of Rocket Lab USA, Inc. (RKLB) have gained 74.4% in the past three months, surpassing the 9.4% growth of the Zacks Aerospace-Defense Equipment industry. It also outperformed the Zacks Aerospace sector’s growth of 9% and the S&P 500’s rise of 8.9%.

Other defense equipment stocks, such as AAR Corporation (AIR) and Curtiss-Wright Corporation (CW), have also outperformed the industry in the past three months. Shares of AIR have gained 19.7%, while shares of CW have gained 16.6%.

With RKLB’s robust performance on the bourses, some investors may consider buying the stock right away. However, before taking any decision, it is important to understand the reasons behind this robust performance. Does the company have what it takes to continue this momentum, or are there risks that may affect its growth? The idea is to help investors make a more insightful decision.

Rocket Lab’s share gains over the past three months seem to be supported by its strong revenue performance in the recent quarterly results, notable acquisitions and contract wins. Notably, in August 2025, the company announced its second-quarter 2025 results, wherein its revenues of $144 million beat estimates by 7% and surged 36% year over year.

In August, RKLB also completed the acquisition of GEOST, which will now allow it to provide electro-optical and infrared (EO/IR) sensor systems and thus strengthen its position in next-generation defense technology space. In the same month, Rocket Lab reached an integration milestone for the U.S. Space Force’s Victus Haze mission. This achievement showed its ability to deliver responsive space operations from payload preparation to launch.

In July 2025, RKLB selected Bollinger Shipyards to support modifications for its Neutron landing platform. This step is important for preparing the rocket’s future reusable operations and expanding into the medium-lift launch market.

Moreover, in June, Rocket Lab got selected to launch a dedicated Electron mission for the European Space Agency (ESA) for the first time, to deploy the first pair of satellites for a future navigation constellation for Europe.

These catalysts must have boosted investor confidence in RKLB’s market potential and thereby driven its share price higher over the past three months.

Rocket Lab continues to build growth momentum through successful missions, acquisitions and new product development. In August 2025, it launched its 69th Electron rocket for Institute for Q-shu Pioneers of Space, Inc., marking the 11th successful mission this year with a 100 percent success rate. Frequent launches are expected to support its goal of completing more than 20 Electron missions in 2025, which shows strong demand and growing trust from both commercial and government clients. These launches also fetch solid revenue and earnings growth for the company in the coming quarters.

Looking ahead, the first launch of the Neutron rocket, expected in the second half of 2025, remains a major growth catalyst for RKLB. Supported by the recently awarded contract to build its ocean landing platform, Neutron is designed to expand Rocket Lab’s reach beyond small satellite launches. This could allow the company to compete for larger missions and higher-value contracts against major players in the space industry.

Rocket Lab shows strong growth potential in the near term, but investors should also keep in mind some important risks. One key concern is the company’s high operating costs. Rocket Lab continues to spend heavily on the development of advanced technologies such as the Neutron rocket, satellite platforms and other space systems. These expenses often exceed revenue growth and have resulted in ongoing losses in recent quarters and might also continue to do so in the near term.

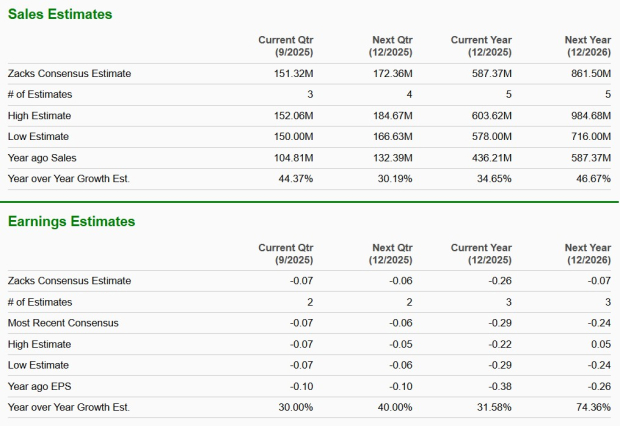

The Zacks Consensus Estimate for RKLB’s 2025 revenues indicates a solid improvement of 34.7% from the prior-year level. The estimate for its earnings also indicates a solid improvement from the prior-year quarter.

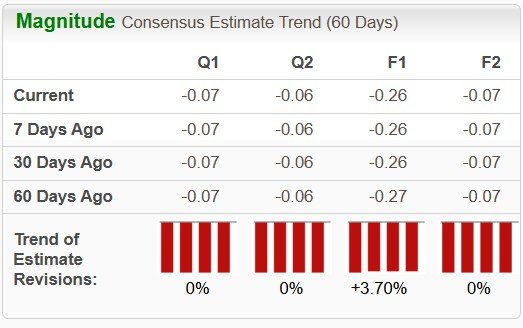

The upward revision in its 2025 earnings estimate over the past 60 days reflects increasing analysts' confidence in its earnings growth prospects. The other near-term estimates remained stable over the past 60 days.

RKLB shares are trading at a premium, with its forward 12-month Price/Sales (P/S F12M) being 27.92X compared with its industry’s average of 2.26X.

Its industry peers, AIR and CW, are trading at a discount in comparison with RKLB. AIR is trading at a P/S F12M of 0.93X, while CW is trading at a P/S F12M of 5.17X.

Investors interested in RKLB should wait for a better entry point, considering its premium valuation and the persistent high operating costs. However, those who already own this Zacks Rank #3 (Hold) stock may choose to maintain their positions, taking into account its solid long-term prospects, outperformance at the bourses and strong sales growth expectations.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 min | |

| 21 min | |

| 24 min | |

| 30 min | |

| 32 min | |

| 34 min | |

| 1 hour |

Rocket Lab Reports Earnings Tonight: What Do Prediction Markets Say About Neutron Launches in 2026?

RKLB

Benzinga Prediction Markets

|

| 2 hours | |

| 2 hours | |

| 5 hours | |

| 5 hours |

SpaceX Rivals Rocket Lab, AST SpaceMobile About To Report Earnings. What To Expect.

RKLB

Investor's Business Daily

|

| 12 hours | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite