|

|

|

|

|||||

|

|

|

Affirm Holdings, Inc. AFRM is trading like a market favorite, yet its valuation is raising eyebrows. The stock commands a forward 12-month price-to-sales (P/S) multiple of 6.26X, well above its three-year median of 3.63X and the broader industry average of 5.83X. Even more striking, it dwarfs the P/S ratios of rival buy now, pay later (BNPL) providers like PayPal Holdings, Inc. PYPL and Block, Inc. XYZ, which are trading at 1.94X and 1.81X P/S, respectively.

The question is clear: is the market’s confidence in Affirm warranted, or is it stretching too far ahead of reality?

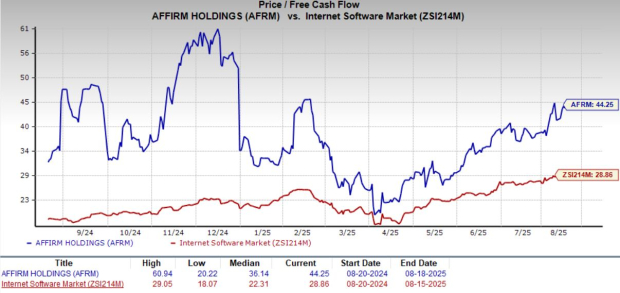

Moreover, Affirm’s free cash flow surged 109.3% over the past year to $609 million, which is a healthy sign. Yet at a P/FCF of 44.25X, the stock is trading at a premium versus the industry’s 28.86X. Such lofty multiples demand careful scrutiny: Are fundamentals strong enough to sustain this optimism, or are investors overpaying for growth?

The company exited the fiscal third quarter with $1.4 billion in cash and cash equivalents, up 33.4% from fiscal 2024-end. Funding debt also climbed to $1.9 billion, pushing its long-term debt-to-capital ratio to 71.81%, far above the industry’s 13.62%. While leverage is high, Affirm’s robust cash generation provides some cushion for future investments and expansion.

Affirm is not just chasing new customers, it is cultivating repeat usage. Short-term offerings like Pay in 2 and Pay in 30 encourage quick re-engagement, boosting lifetime value and stickiness. The payoff is clear — 94% of the third quarter of fiscal 2025 transactions came from repeat customers.

To further embed itself in everyday spending, Affirm is expanding into essentials like groceries, fuel, travel, subscriptions and partnering with the likes of Costco and World Market. The strategy is paying off, with transactions soaring 45.6% year over year to 31.3 million in the last reported quarter.

Beyond core BNPL, the company is investing in debit solutions and B2B tools, broadening its product ecosystem. These innovations aim to increase transaction frequency, deepen customer relationships, and enhance stickiness across its platform.

Its Shopify tie-up is set to launch operations in France, Germany, and the Netherlands, extending its reach across Europe. With a merchant network of nearly 360,000 partners, the growth runway looks promising.

The company is also venturing into gaming through a deal with Xsolla, aiming to tap younger, digital-native consumers. Further expansion into Canada and the U.K. is also on the board for this partnership. Added to that, a deeper partnership with Google Pay and Affirm’s ecosystem is becoming increasingly embedded in high-frequency spending categories.

The Zacks Consensus Estimate for Affirm’s fiscal 2025 earnings suggests a 103% year-over-year improvement to 5 cents per share, while fiscal 2026 earnings are expected to increase to 76 cents. Revenue projections are also strong, with fiscal 2025 and 2026 expected to grow 37.2% and 22.8%, respectively.

The company anticipates fiscal 2025 Gross Merchandise Value between $35.7 and $36 billion. Affirm has also crushed estimates in each of the past four quarters, with an average surprise of 102.2%.

Affirm Holdings, Inc. price-eps-surprise | Affirm Holdings, Inc. Quote

Affirm shares have risen 28.4% so far this year, outperforming the industry average of 22.6%. Its growth has surpassed peers such as PayPal and Block, as well as the broader S&P 500 Index.

Competition is fierce in the innovative payments landscape. Deep-pocketed rivals like PayPal and Block, along with traditional financial institutions, are aggressively expanding in the BNPL space. Walmart’s decision to switch from Affirm to Klarna underscores the challenge of retaining large merchants in a competitive space.

Operating expenses have been rising steadily, up 76.6% in fiscal 2022, 25.9% in fiscal 2023 and 5.4% in fiscal 2024. Even in the fiscal third quarter, expenses increased 7.4%. While ongoing investments are essential for growth, tighter cost discipline will be required to protect its margins.

The stock is currently trading above Wall Street’s average price target of $71.18, implying a 9.58% downside from current levels.

Affirm is rapidly carving out a strong position in the BNPL space, with impressive repeat usage, expanding partnerships and ambitious international moves that enhance its growth story. Its robust cash flow generation and upbeat earnings outlook further strengthen the bull case. However, the stock’s stretched valuation, elevated leverage and intensifying competitive pressures temper the upside. AFRM currently carries a Value Score of F.

With shares already trading above consensus price targets, the risk/reward profile looks balanced. Given these dynamics, Affirm currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite