|

|

|

|

|||||

|

|

|

Primoris Services PRIM provides contracting and infrastructure services across construction, fabrication, engineering, and beyond.

The company benefits from secular spending throughout the energy and utilities sectors after years of underinvestment, boosted by the power-hungry artificial intelligence boom.

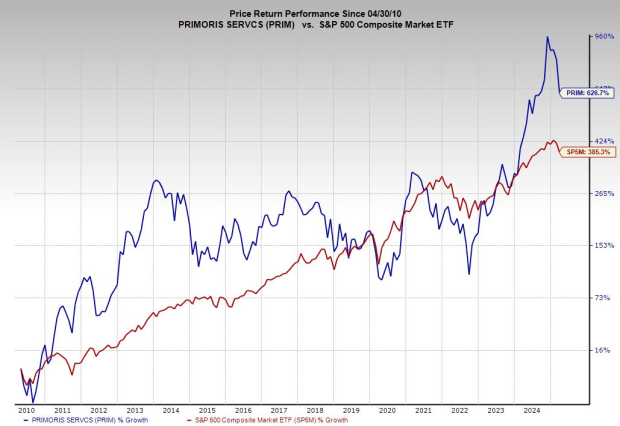

This critical infrastructure services giant has crushed the S&P 500 and the Zacks Construction sector over the past 15 years, including a 120% surge during the past 24 months. PRIM’s recent pullback has it trading 55% below its average Zacks price target, and its earnings estimates keep climbing.

Primoris Services is a specialty construction and infrastructure company that builds and maintains critical systems across the U.S. and Canada, focusing mostly on utilities and energy. The firm’s footprint spans power generation, utilities and distribution, renewables, oil and gas, chemicals, pipelines, and civil infrastructure.

The company handles projects such as installing and maintaining natural gas and electric utility systems, constructing pipelines for gas, water, and wastewater, and working on renewable energy projects like utility-scale solar and energy storage facilities. Primoris also takes on heavy civil projects, including highway and bridge construction.

The Dallas-based company is a behind-the-scenes player ensuring the infrastructure for energy, utilities, and transportation keeps running and growing. Its power delivery segment will thrive as the country races to build out the grid to support the massive overnight expansion of AI data centers.

PRIM doubled its revenue between 2019 and 2024, averaging 22% growth over the trailing three years, and it closed 2024 with a record backlog of $11.9 billion.

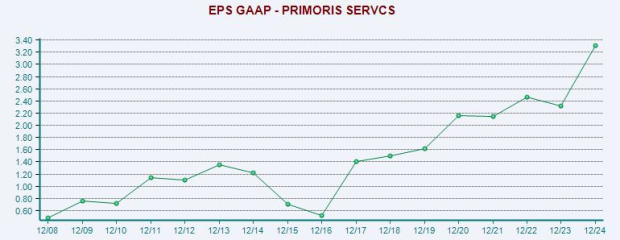

PRIM grew its adjusted earnings by 36% in FY24 and provided upbeat guidance, earning it a Zacks Rank #2 (Buy). PRIM has crushed our EPS estimates by an average of 156% over the trailing four quarters.

Primoris is projected to average 15% EPS growth in 2025 and 2026, alongside 5.5% average sales expansion.

PRIM stock has soared 120% in the past two years, blowing away its sector’s 35% and the S&P 500’s 37%. This run is part of a 620% surge over the last 15 years, outpacing the S&P 500’s 380% and the Construction sector’s 260%.

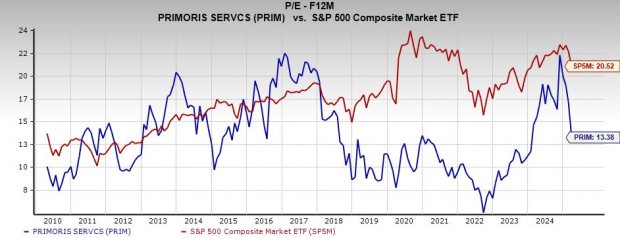

Despite its outperformance, Primoris trades at a 34% discount to the S&P 500, 17% below its sector, and near its 15-year median at 13.4X forward earnings.

Primoris trades 55% below its average Zacks price target, and it’s trying to find support near its pre-Q4 breakout levels. On top of that, six of the seven brokerage recommendations Zacks has for PRIM are “Strong Buys,” and it pays a dividend.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-10 | |

| Jan-23 | |

| Jan-22 | |

| Jan-20 | |

| Jan-13 | |

| Jan-12 | |

| Jan-12 |

IBD Stock Of The Day Primoris: Early Buy Point For The Data Center Builder

PRIM

Investor's Business Daily

|

| Jan-06 | |

| Dec-30 | |

| Dec-29 | |

| Dec-29 | |

| Dec-24 | |

| Dec-19 |

Psst! This Stealth AI Stock Eyes Entry Amid Powerful Run As Earnings Surge 75%

PRIM

Investor's Business Daily

|

| Dec-15 | |

| Dec-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite