|

|

|

|

|||||

|

|

|

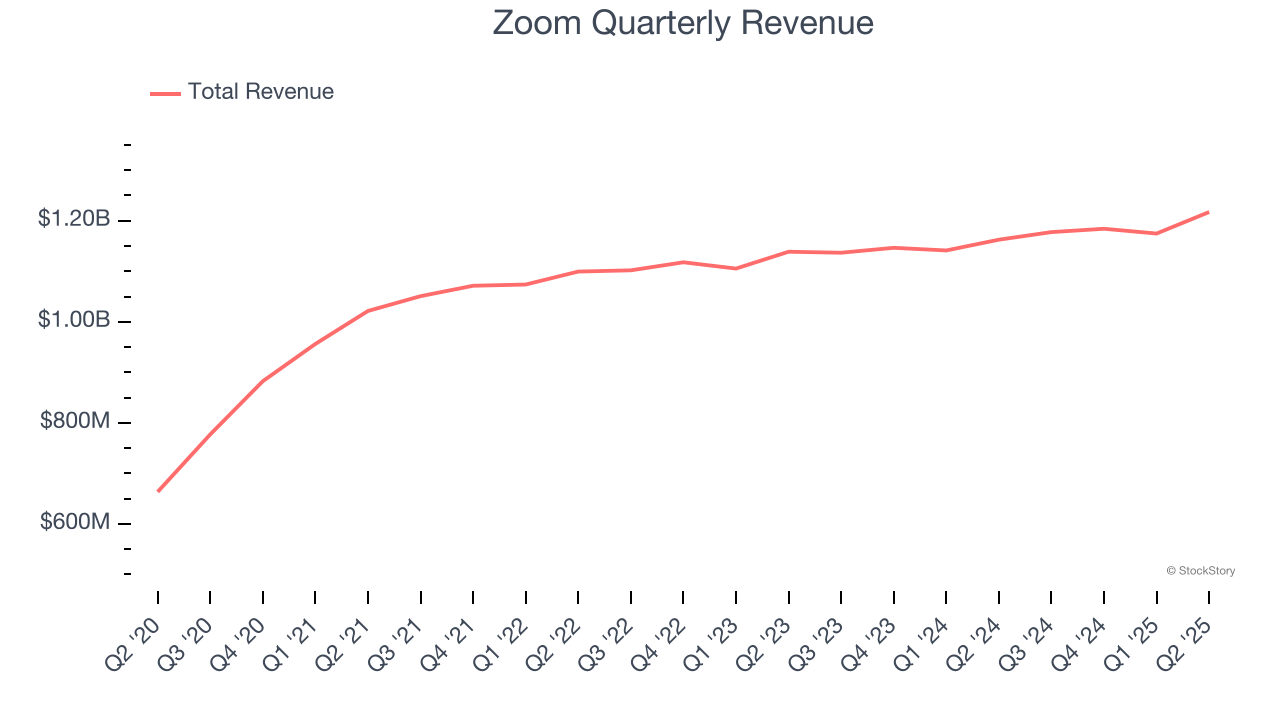

Video communications platform Zoom (NASDAQ:ZM) reported Q2 CY2025 results topping the market’s revenue expectations, with sales up 4.7% year on year to $1.22 billion. The company expects next quarter’s revenue to be around $1.21 billion, close to analysts’ estimates. Its non-GAAP profit of $1.53 per share was 11% above analysts’ consensus estimates.

Is now the time to buy Zoom? Find out by accessing our full research report, it’s free.

“AI is transforming the way we work together, and Zoom is at the forefront, driving innovation that helps people get more done, reduce costs, and deliver better experiences for customers and employees alike,” said Eric S. Yuan, Zoom’s founder and CEO.

Once the verb that defined remote work during the pandemic ("let's Zoom later"), Zoom (NASDAQ:ZM) provides a cloud-based platform for video meetings, phone calls, team chat, and collaboration tools that helps businesses and individuals connect virtually.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Zoom grew its sales at a weak 3.4% compounded annual growth rate. This was below our standard for the software sector and is a tough starting point for our analysis.

This quarter, Zoom reported modest year-on-year revenue growth of 4.7% but beat Wall Street’s estimates by 1.8%. Company management is currently guiding for a 3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.6% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and implies its newer products and services will not catalyze better top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

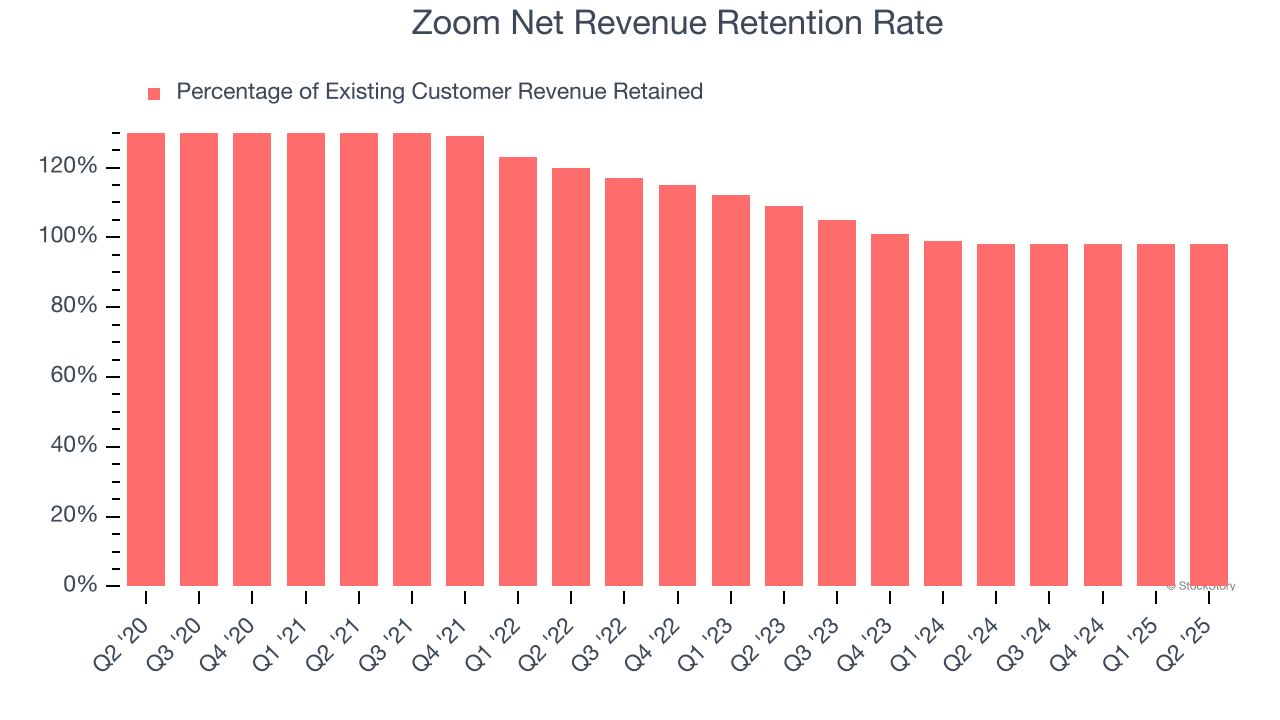

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Zoom’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 98% in Q2. This means Zoom’s revenue would’ve decreased by 2% over the last 12 months if it didn’t win any new customers.

Zoom has a weak net retention rate, signaling that some customers aren’t satisfied with its products, leading to lost contracts and revenue streams.

We were impressed by Zoom’s optimistic full-year EPS guidance, which blew past analysts’ expectations. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its new large contract wins slowed. Overall, this print had some key positives. The stock traded up 5.7% to $77.44 immediately following the results.

Sure, Zoom had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-13 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-08 | |

| Feb-05 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 | |

| Feb-04 | |

| Feb-03 | |

| Feb-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite