|

|

|

|

|||||

|

|

|

Kulicke and Soffa has been treading water for the past six months, recording a small loss of 3.6% while holding steady at $38.33. The stock also fell short of the S&P 500’s 8.6% gain during that period.

Is now the time to buy Kulicke and Soffa, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're sitting this one out for now. Here are three reasons why KLIC doesn't excite us and a stock we'd rather own.

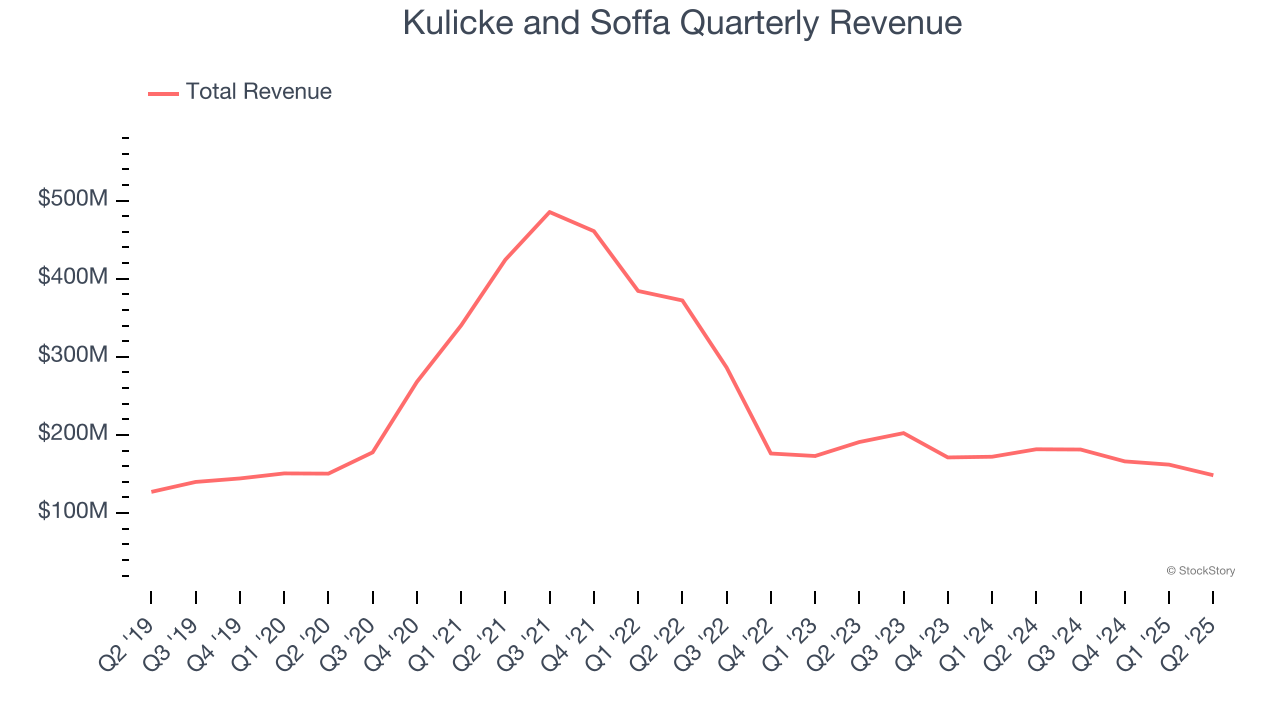

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Kulicke and Soffa’s sales grew at a sluggish 2.4% compounded annual growth rate over the last five years. This was below our standards. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

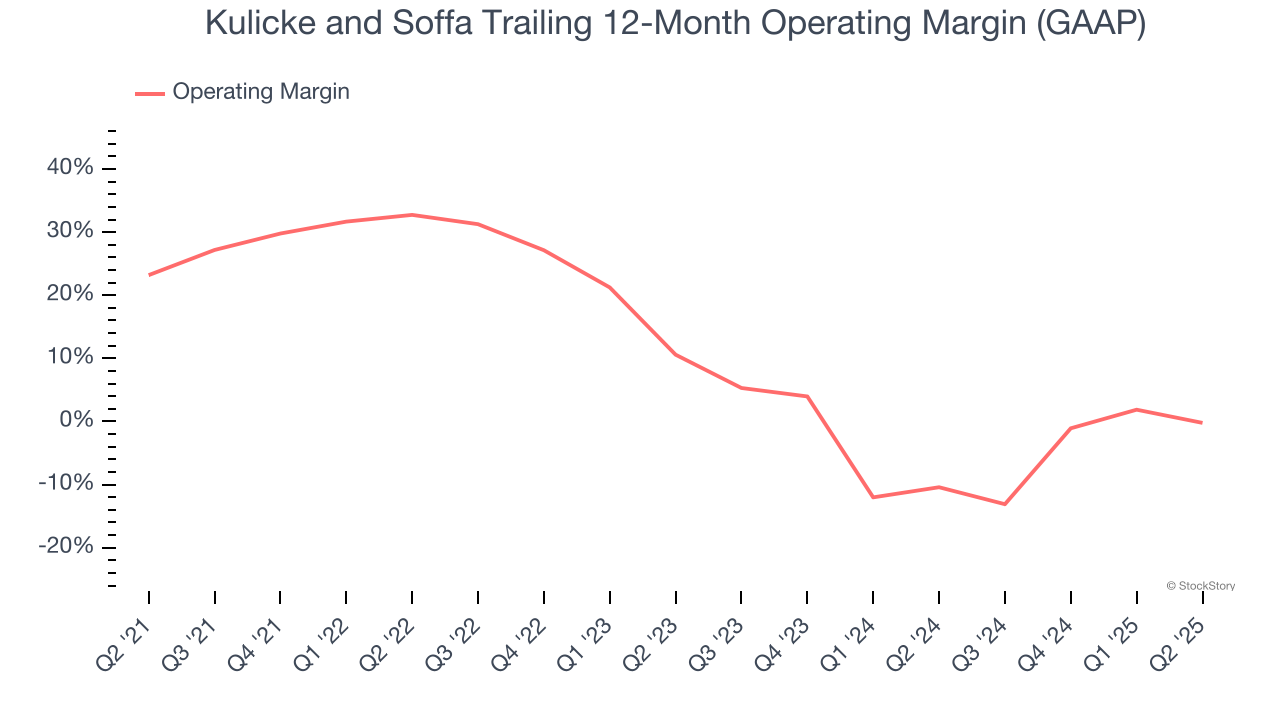

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, Kulicke and Soffa’s operating margin decreased by 23.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Kulicke and Soffa’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was breakeven.

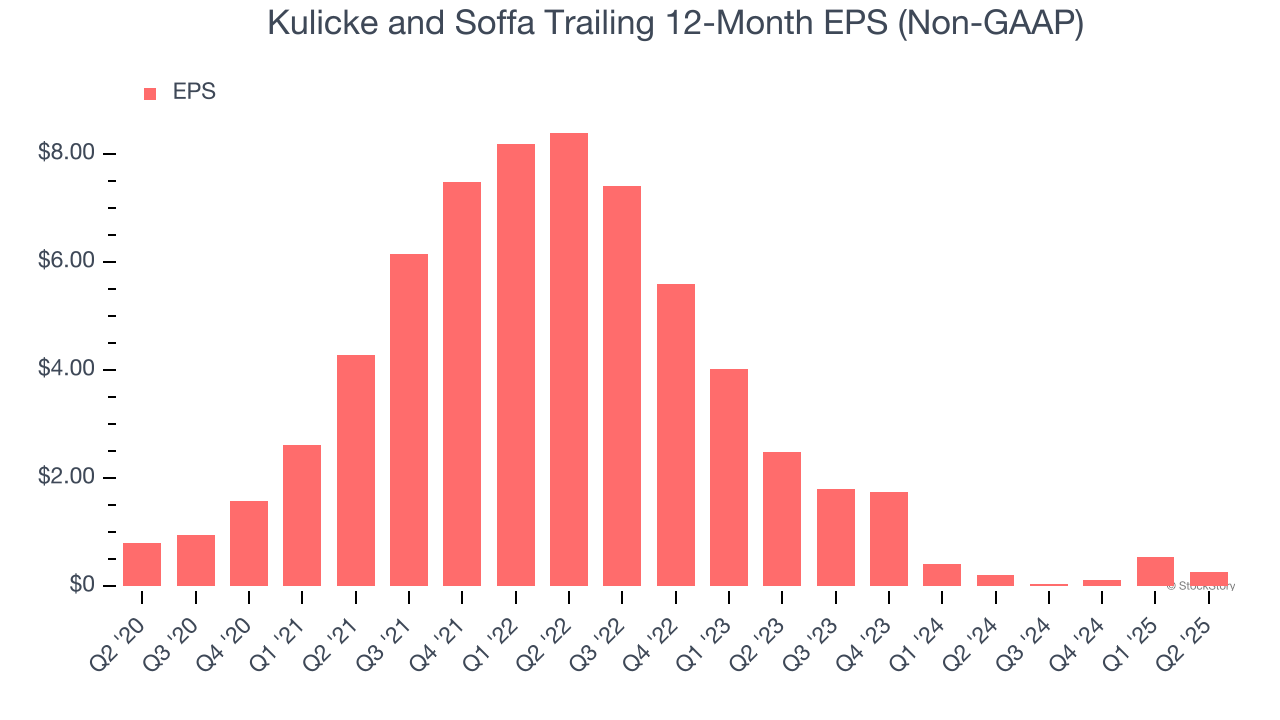

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Kulicke and Soffa, its EPS declined by 20.3% annually over the last five years while its revenue grew by 2.4%. This tells us the company became less profitable on a per-share basis as it expanded.

Kulicke and Soffa doesn’t pass our quality test. With its shares trailing the market in recent months, the stock trades at 35.6× forward P/E (or $38.33 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d recommend looking at the most entrenched endpoint security platform on the market.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-22 | |

| Jun-15 | |

| May-27 | |

| May-07 | |

| May-06 | |

| May-06 | |

| Apr-24 | |

| Apr-22 | |

| Apr-09 |

Kulicke And Soffa, IBD Stock Of The Day, Surges Toward Buy Point In Chip Gear Rally

KLIC +6.14%

Investor's Business Daily

|

| Apr-09 | |

| Mar-24 | |

| Mar-24 | |

| Mar-04 | |

| Mar-03 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite