|

|

|

|

|||||

|

|

|

As the Q2 earnings season wraps, let’s dig into this quarter’s best and worst performers in the video conferencing industry, including RingCentral (NYSE:RNG) and its peers.

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

The 4 video conferencing stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 1.8% while next quarter’s revenue guidance was in line.

Luckily, video conferencing stocks have performed well with share prices up 12.8% on average since the latest earnings results.

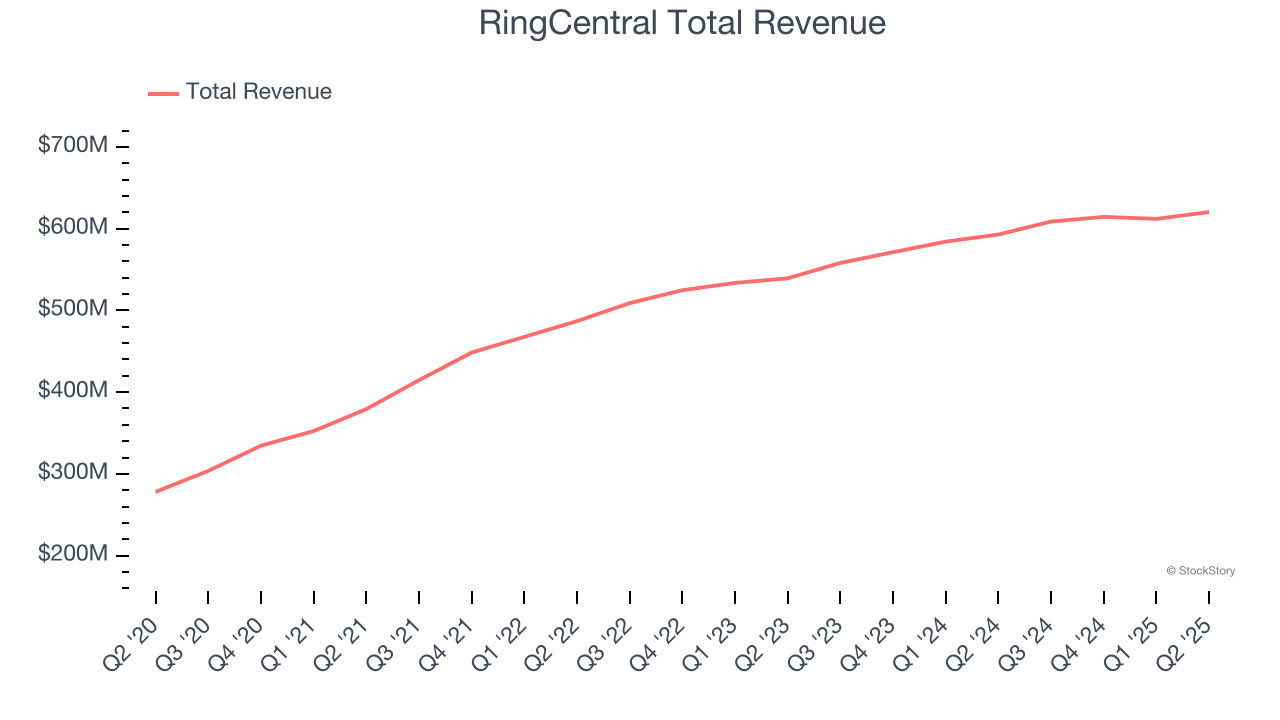

Built on its proprietary Message Video Phone (MVP) platform that unifies multiple communication methods, RingCentral (NYSE:RNG) provides AI-driven cloud communications and collaboration solutions that enable businesses to connect through voice, video, messaging, and contact center services.

RingCentral reported revenues of $620.4 million, up 4.6% year on year. This print was in line with analysts’ expectations, and overall, it was a satisfactory quarter for the company with a solid beat of analysts’ EBITDA estimates but revenue guidance for next quarter meeting analysts’ expectations.

“I want to congratulate Vaibhav Agarwal on his promotion to Chief Financial Officer of RingCentral. With his nine year tenure in prior roles as Deputy Chief Financial Officer, Chief Transformation Officer, and Chief Accounting Officer, Vaibhav has been a key contributor and has a deep understanding of our strategy, finances, and operations,” said Vlad Shmunis, Founder, Chairman and CEO of RingCentral.

RingCentral delivered the weakest performance against analyst estimates of the whole group. Interestingly, the stock is up 30.7% since reporting and currently trades at $30.87.

Is now the time to buy RingCentral? Access our full analysis of the earnings results here, it’s free.

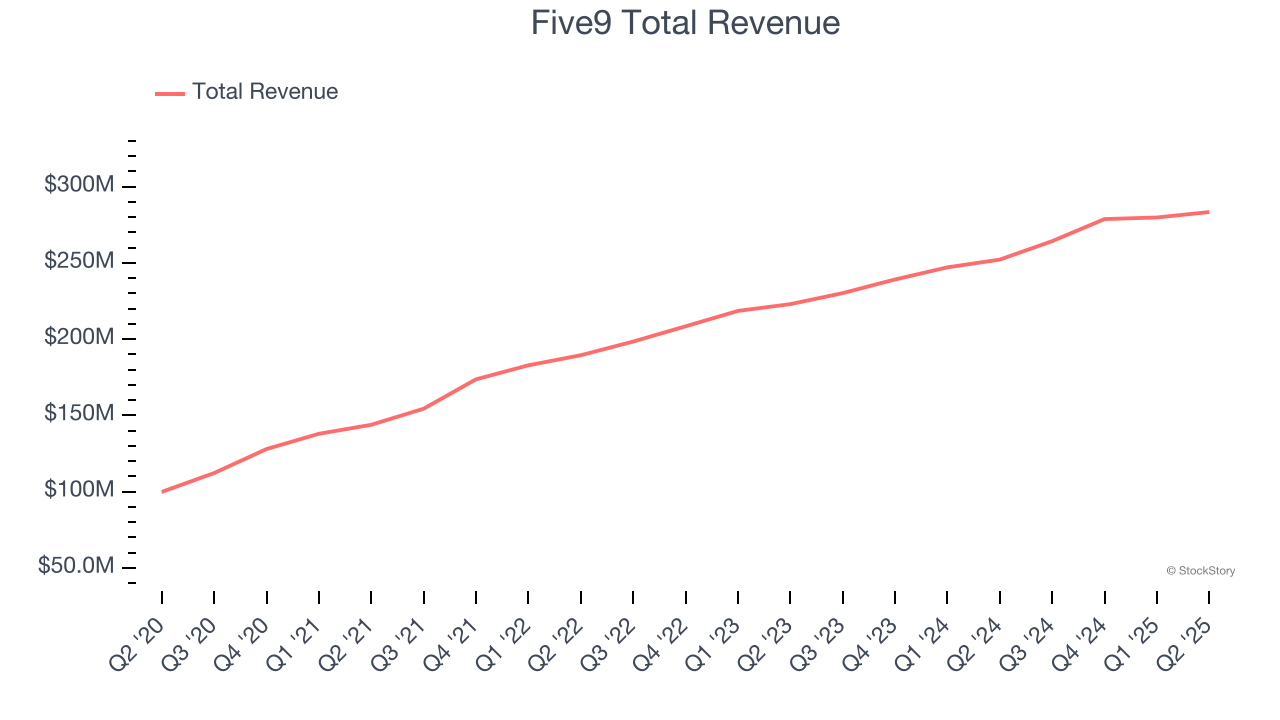

Taking its name from the "five nines" (99.999%) standard for optimal service reliability in telecommunications, Five9 (NASDAQ:FIVN) provides cloud-based software that enables businesses to run their contact centers with tools for customer service, sales, and marketing across multiple communication channels.

Five9 reported revenues of $283.3 million, up 12.4% year on year, outperforming analysts’ expectations by 2.9%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA estimates and full-year EPS guidance exceeding analysts’ expectations.

Five9 pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 5.6% since reporting. It currently trades at $27.26.

Is now the time to buy Five9? Access our full analysis of the earnings results here, it’s free.

Named after its founding year (1987) with "8x8" representing binary code for communications, 8x8 (NASDAQ:EGHT) provides cloud-based contact center and unified communications solutions that enable businesses to manage customer interactions and internal communications through a single platform.

8x8 reported revenues of $181.4 million, up 1.8% year on year, exceeding analysts’ expectations by 2.2%. Still, it was a mixed quarter as it posted a significant miss of analysts’ EBITDA estimates.

8x8 delivered the slowest revenue growth and weakest full-year guidance update in the group. Interestingly, the stock is up 1.8% since the results and currently trades at $1.96.

Read our full analysis of 8x8’s results here.

Once the verb that defined remote work during the pandemic ("let's Zoom later"), Zoom (NASDAQ:ZM) provides a cloud-based platform for video meetings, phone calls, team chat, and collaboration tools that helps businesses and individuals connect virtually.

Zoom reported revenues of $1.22 billion, up 4.7% year on year. This result beat analysts’ expectations by 1.8%. It was a strong quarter as it also produced a solid beat of analysts’ EBITDA estimates and full-year EPS guidance exceeding analysts’ expectations.

Zoom achieved the highest full-year guidance raise among its peers. The company added 82 enterprise customers paying more than $100,000 annually to reach a total of 4,274. The stock is up 13.1% since reporting and currently trades at $82.82.

Read our full, actionable report on Zoom here, it’s free.

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-31 | |

| Mar-24 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-05 | |

| Mar-01 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite