|

|

|

|

|||||

|

|

|

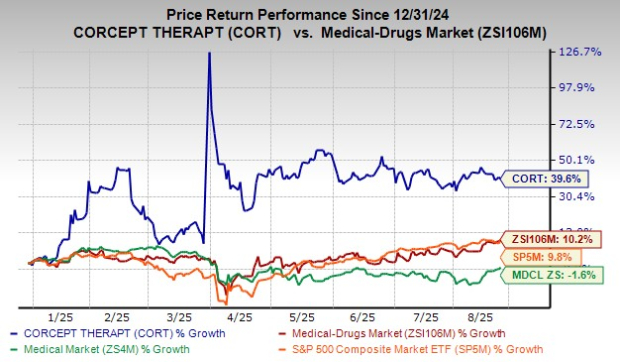

Corcept Therapeutics CORT has delivered a strong performance in the year-to-date period. Shares of the company have rallied 39.6% compared with the industry’s rise of 10.2%. The stock has also outperformed the sector and the S&P 500 index in the same timeframe, as shown in the chart below.

The company has made rapid progress with its lead pipeline candidate, relacorilant, which is being developed for the treatment of Cushing’s syndrome. The candidate is also being evaluated in combination studies for treating different cancer indications. The outperformance can be mainly attributed to ongoing development efforts for relacorilant, which is nearing potential FDA approval for Cushing’s syndrome by December 2025.

In December 2024, the company submitted a new drug application (NDA) for relacorilant to the FDA for treating patients with hypercortisolism (Cushing's syndrome).

In March 2025, the FDA accepted the NDA for relacorilant to treat hypercortisolism. The regulatory body has assigned a Prescription Drug User Fee Act target action date of Dec. 30, 2025.

The NDA was based on positive data from the GRACE study and confirmatory evidence from the phase III GRADIENT, as well as long-term extension studies and a phase II study in hypercortisolism.

A potential FDA nod for relacorilant is likely to boost Corcept’s growth prospects, given that it already markets Korlym (mifepristone), which is also approved for treating Cushing's syndrome.

Last month, Corcept submitted another NDA to the FDA seeking approval for relacorilant in combination with nab-paclitaxel for treating patients with platinum-resistant ovarian cancer. This marked a new NDA for relacorilant.

The NDA for relacorilant in platinum-resistant ovarian cancer was based on data from the pivotal phase III ROSELLA study and phase II studies.

Recently, the company announced that the ROSELLA study met its primary endpoint of improved progression-free survival, as assessed by blinded independent central review (PFS-BICR). Per management, data from the ROSELLA study suggested that the combo of relacorilant plus nab-paclitaxel has the potential to become a new standard of care for patients with platinum-resistant ovarian cancer.

Corcept is also evaluating relacorilant plus nab-paclitaxel and Roche’s RHHBY Avastin (bevacizumab) in the phase II BELLA study for treating patients with platinum-resistant ovarian cancer.

Per management, the BELLA study will help in understanding whether combining relacorilant with two medicines — nab-paclitaxel and RHHBY’s Avastin — offers patients an additional treatment option or not.

The company is also evaluating relacorilant plus Xtandi (enzalutamide) in patients with early-stage prostate cancer. This phase II study is being conducted in collaboration with the University of Chicago.

Corcept is evaluating its other pipeline candidates, dazucorilant and miricorilant, in separate mid-stage studies for treating amyotrophic lateral sclerosis and biopsy-confirmed or presumed metabolic dysfunction-associated steatohepatitis, respectively.

At present, Corcept’s top line solely comprises product sales from Korlym. The company is entirely dependent on Korlym for revenues. Sales of the drug were relatively slow in the first half of 2025.

In the first half of 2025, Korlym recorded sales of $351.6 million, up around 13.2% year over year. Our model estimates full-year 2025 Korlym sales at $857.1 million, suggesting an increase of almost 27% year over year.

During the second-quarter earnings call, management lowered its total revenue guidance for 2025. For full-year 2025, the company now expects total revenues in the range of $850-$900 million compared with the earlier projection of $900-$950 million.

Though the potential FDA nod for relacorilant is likely to give Corcept its marketed product for Cushing's syndrome, the softer sales for Korlym remain a concern.

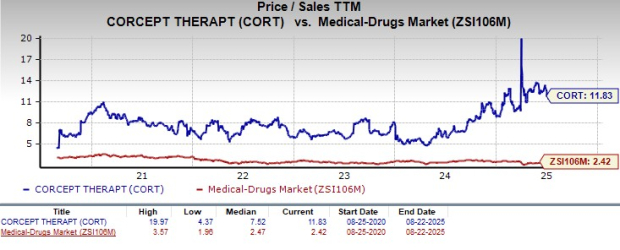

From a valuation standpoint, Corcept is trading at a premium to the industry. Going by the price-to-sales (P/S) ratio, the company’s shares currently trade at 11.83, lower than 2.42 for the industry. The stock is also trading above its five-year mean of 7.52.

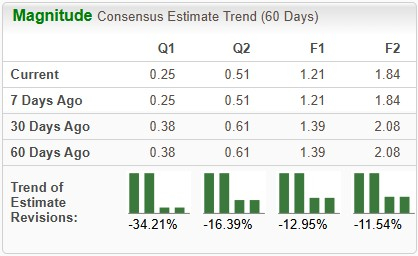

The Zacks Consensus Estimate for its 2025 earnings per share (EPS) has decreased from $1.39 to $1.21 over the past 30 days. During the same time frame, EPS estimates for 2026 have decreased from $2.08 to $1.84.

We note that the successful development and potential approval of relacorilant should help Corcept address a broader patient population and likely push the stock upward in future quarters.

However, softer sales for Korlym are a concern. Any regulatory setback for Korlym and a developmental issue with relacorilant will be a huge blow for the company. Also, failure in ongoing studies and pipeline setbacks will hurt the growth prospects.

We would advise investors to wait for the FDA decision on relacorilant in Cushing's syndrome, additional data readouts, and the successful completion of other pipeline studies. For those already owning the stock, staying invested for now would be a prudent move. It also remains to be seen whether relacorilant can reduce the heavy dependence on Korlym for revenues in the future quarters.

Corcept Therapeutics Incorporated price | Corcept Therapeutics Incorporated Quote

Corcept currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the drug sector are Avadel Pharmaceuticals AVDL and Rigel Pharmaceuticals RIGL, each sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

In the past 60 days, estimates for Avadel Pharmaceuticals’ EPS have increased from 17 cents to 26 cents for 2025. During the same time, EPS estimates for 2026 have increased from 72 cents to 88 cents. Year to date, AVDL stock has rallied 45%.

Avadel Pharmaceuticals’ earnings beat estimates in three of the trailing four quarters, while meeting the same on the remaining occasion, delivering an average surprise of 119.64%.

In the past 60 days, estimates for Rigel Pharmaceuticals’ EPS have increased from $2.25 to $4.26 for 2025. During the same time, EPS estimates for 2026 have increased from $1.60 to $2.68. Year to date, shares of RIGL have surged 146.7%.

Rigel Pharmaceuticals’ earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 1,840.49%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-07 | |

| Jul-01 | |

| Jun-17 | |

| Jun-16 | |

| Jun-06 | |

| May-29 | |

| May-27 | |

| May-27 | |

| May-27 | |

| May-21 | |

| May-14 | |

| May-12 | |

| May-12 | |

| May-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite